Wolfspeed is an interesting company to have a look at for several reasons. One, this is a pure play on silicon carbide, one of the highest growth areas in semiconductors. Two, Wolfspeed is vertically integrated across the entire silicon carbide value chain, from crystal growing, to wafer fabrication, to semiconductor manufacturing, while boasting strong market shares in each of these. Three, the shares are now trading at their lowest level in three years.

Do me a favor and hit the subscribe button. Subscriptions let me know you are interested in research like this, which is a good motivation to publish more of the analysis I’m carrying out. Special thanks to the 400 subscribers so far!

Overview of the SiC field

Silicon Carbide (SiC) is the key material to drive the electrification of the world. Energy in batteries is stored in the form of direct current, which needs to get converted into alternating current to power engines. Power semiconductors made from SiC are extremely good at this. Much better than purely silicon ones. This leads to large cost savings in terms of electricity usage and also strong performance gains. Not only is a SiC powered electric vehicle cheaper to drive, but it also has better range and you can charge it ‘ultrafast’.

Wolfspeed is at the heart of all of this, having been the key pioneer in the field. This has resulted in the company having a strong patent portfolio and attractive market shares across the entire value chain, from SiC crystal growing, to wafer fabrication, to semiconductor manufacturing and finally, the packaging into units and modules.

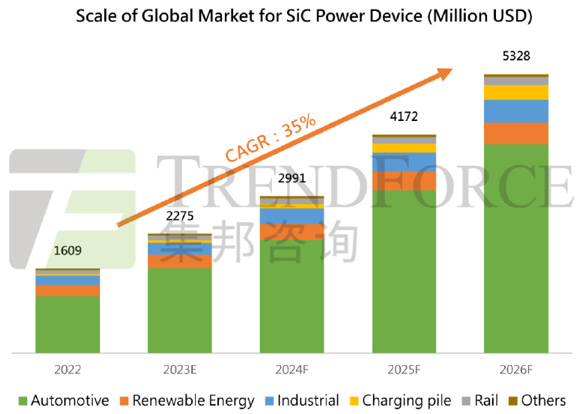

According to all estimates I’ve seen, the SiC market is expected to explode over the coming decade. Both semiconductor research houses Yole and TrendForce estimate the market to grow at a CAGR of around 35%. Most of this is being driven by the switch to electric vehicles, but also to some extent by the industrial end market. The latter using SiC power semiconductors in the electric grid, renewable power generation, and battery storage as some examples. How TrendForce sees the market evolving:

Electric vehicles remain the key end market, and the trend here is towards making use of higher voltages. The attraction for Wolfspeed is that this increases the need for more advanced SiC modules. Higher voltages have several advantages. The first is that this increases power efficiency, meaning lower electrical losses. This results in both lower driving costs as well as better vehicle range. Secondly, it allows for thinner wiring and smaller components, resulting not only in lower manufacturing costs but also a lower vehicle weight, again increasing range while lowering electricity costs. Finally, higher voltages allow for faster charging. Although most electric vehicle charging can easily be done overnight at home, similar to how you recharge your iPhone, it’s still convenient to have the optionality of a fast charge available when making a long drive.

Below is an illustration of a SiC module from the Japanese automotive supplier Denso:

SiC crystal growing and wafer fabrication

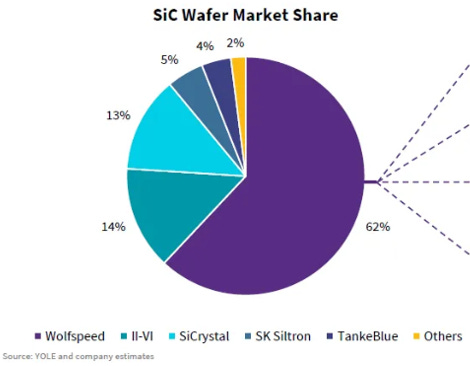

Wolfspeed’s market share in SiC wafer fabrication is impressive. At its 2021 capital markets day, the company disclosed to occupy 62% of the market.

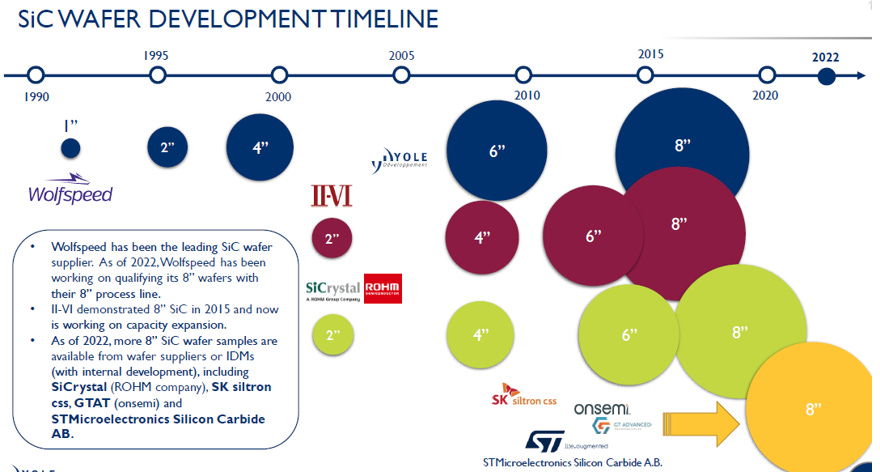

Yole illustrates how Wolfspeed has been a pioneer in this field. A number of players have been able to successfully develop 8 inch wafers (200 millimeter) in the lab. Currently there is a race ongoing to successfully implement this in a high-volume manufacturing setting.

Reading up on on SiC crystal growing, it looks to be a rather complicated process. The silicon carbide molecule is a combination of one silicon and one carbon atom. The problem is that these molecules need to be formed under a temperature of roughly half that of the sun. And to complicate matters further, these molecules can organize themselves in around 200 different crystal structures. Of which only one is suitable for application in semiconductors.

Wolfspeed reckons that the SiC semiconductor manufacturers will aim to set-up their own crystal growing and wafer fabrication capabilities as well. Although Wolfspeed estimates that they will likely still source around 50% of their needs from other manufacturers. Also the silicon wafer manufacturers are aiming to enter the field. Reading through various announcements, Taiwan based GlobalWafers and Soitec from France have developed capabilities to manufacture SiC wafers as well. So while the market has an attractive growth rate, the competitive environment will become more intense.

Longer term, my guess is that this market will probably have around ten players or so, which would make it ripe for M&A to consolidate it to around five players. Overall with the high growth in this industry and a future trend towards consolidation, this should become an attractive business over time. However, the main risk is in the near term with a certain number of competitors being able to enter the market which could result in overcapacity and lower margins.

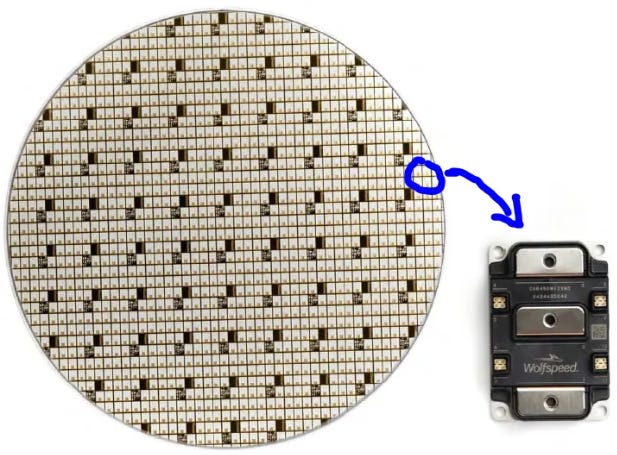

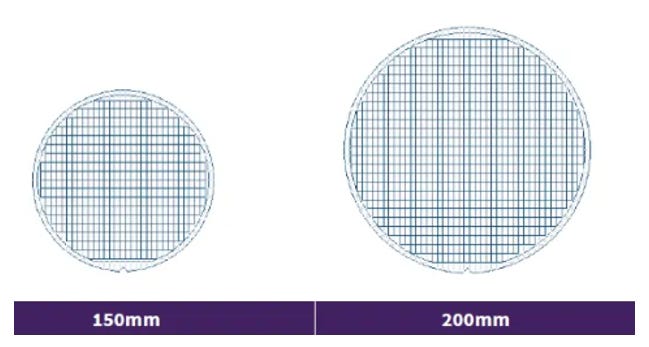

Below is an image of a Wolfspeed fully fabbed 200 mm SiC wafer with an example of how dies can be turned into a module.

Also some explanation about why wafer sizes matter might be useful. The main reason is that the larger the diameter of the wafer, the more chips you can produce from a single one. On the image below, you can see that you can produce 70% more chips from a 200 mm wafer compared to a 150 mm one. This means that you can spread the manufacturing costs of running one wafer over much more chips, strongly lowering the cost per chip. Texas Instruments estimates that their move from 200 mm to 300 mm silicon wafers resulted in a 40% cost saving per chip.

A large part of the silicon chip industry has already moved to 300 mm wafer sizes, although some older fabs on legacy tech can still be running 200 mm ones. Those fabs are fully depreciated, and so are still competitive for the manufacturing of basic chips. For SiC on the other hand, the crystal growing is already sufficiently complex to manage 200 mm wafers, so therefore the industry is now trying to move from 150 mm to 200.

Recently Wolfspeed had a hiccup in the scaling up of their 200mm SiC wafer fabrication. Although the company explains that they saw a similar trajectory with the scaling up of the 150mm wafers. So there is probably no reason to get overly concerned here at this stage. When technology is still in development, it is always somewhat of a nervous feeling. This was not different with ASML during the last decade, EUV was a way bigger question mark than Wolfspeed’s 200mm SiC capabilities. However, back then, I figured that the risk-reward in ASML looked attractive, maybe 25 to 50% downside in the shares if things went wrong, and 5 to 10x upside if things went great. Perhaps Wolfspeed has a similar risk-reward profile, more on this later.

SiC semiconductor manufacturing

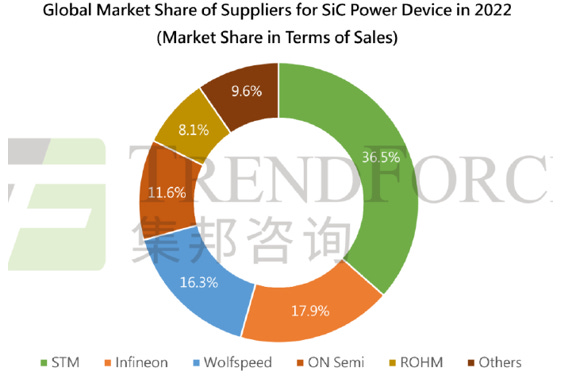

In the manufacturing of SiC semiconductors, European STM and Infineon are currently the two strongest players. With Wolfspeed being slightly behind Infineon. US based ON Semi similarly has good capabilities and is currently number four.

Both Infineon and STM have a long history of high-volume power semiconductor manufacturing (pure silicon ones) while having excellent relationships with the European automotive industry. And they were early in the SiC game as well. Infineon actually tried to acquire Wolfspeed about seven years ago, which is how I first heard about Wolfspeed’s capabilities in SiC crystal growing. As this was the skillset which Infineon wanted to add to their portfolio. However, as some of Wolfspeed’s modules are used by the US military, the deal was eventually blocked.

Also in SiC semiconductor manufacturing we have similar dynamics as in the manufacturing of SiC wafers, i.e. a variety of new entrants aiming to build up capacity. Reading news reports over recent years, I’ve seen mentions for example of Mitsubishi, Renesas, Bosch, Microchip, as well as others announcing plans to build up SiC capacity.

So while the growth in the market looks attractive, as does Wolfspeed’s positioning, there is a risk in the medium term of oversupply resulting in price wars. This will probably become a ten to fifteen player market or so, and over time I expect consolidation to bring this number down to 5 to 8 players.

Consolidation has been a big theme in the semiconductor industry, also on more lagging tech and in analog type semis. For example, over the last decade, Analog Devices acquired both Linear and Maxim, Broadcom acquired Avago, NXP acquired Freescale, Qualcomm subsequently tried to buy NXP which got blocked, and Infineon acquired Cypress. I’m expecting this trend to continue and we will see similar M&A activity in the SiC space. This is good for investors as typically there are synergies to be gained from merging two businesses while it reduces competition.

Wolfspeed’s capex plans and outlook

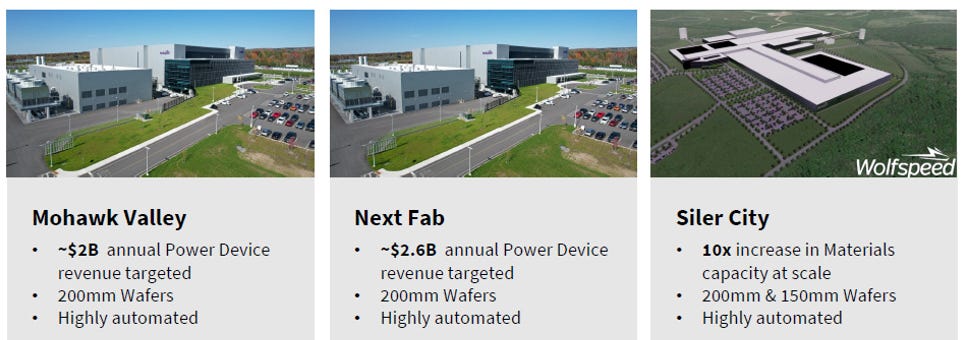

Wolfspeed is momentarily in high investment mode. Currently all its SiC wafers and semiconductors are being manufactured from its Durham facility. However, that one is already running at full capacity and with the high growth in the industry, the plan is to build out two more fabs i.e. Mohawk Valley in New York and Saarland in Germany. Then the company is also building out a site for SiC crystal growing and wafer fabrication in Siler City, North-Carolina, to supply both its own fabs as well as other manufacturers.

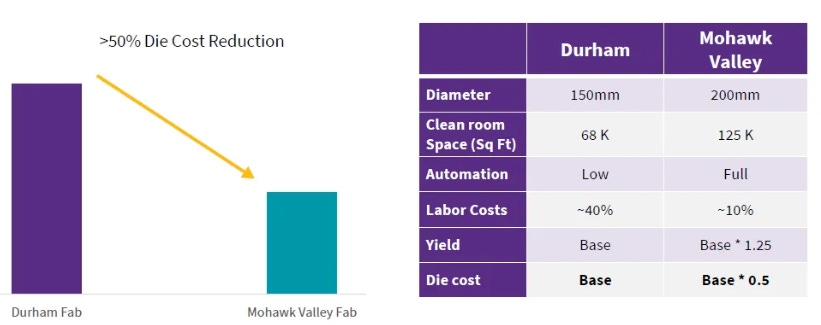

These new facilities will be heavily automated with robotics which over the long run should translate into low manufacturing costs. Wolfspeed reckons that due to this automation and the move to 200 mm wafer sizes, they can get a reduction in the cost per chip of more than 50%:

However, in the near term for investors this will mean negative free cash flows due to the size of these investments. Competitors are using a mixed strategy, some are building out new facilities as well, such as Infineon for example, whereas others are retrofitting older fabs to turn them into SiC fabs e.g. Renesas and Bosch. Retrofitting older fabs lowers the cost of investment, although building a new one could give you advantages in automation. Overall, I don’t dislike Wolfspeed’s strategy here and over the long term it might well turn out that going for state of the art, heavily automated facilities was the smart move to make, similarly as it was for Tesla.

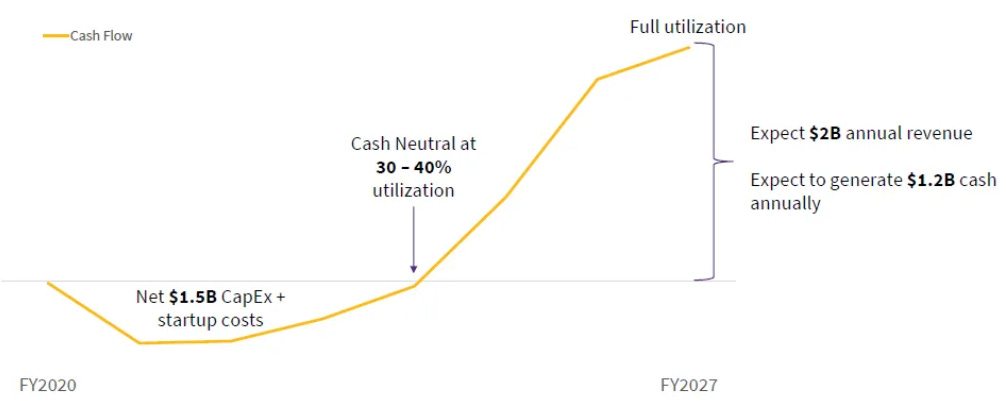

The below chart illustrates how the Mohawk Valley fab should become a free cash flow machine. After government subsidies of $500 million, the net investment made by Wolfspeed is $1.5 billion, and in around 18 months time, when the fab should be running at 30 to 40% utilization rates, it should become cash flow neutral. As the fab gears up to full utilization by 2027, Wolfspeed estimates to generate $2 billion in annual revenues from it, translating into $1.2 billion of annual free cash flow.

During the latest quarterly call, the company confirmed to have started shipping product from this fab and they estimate to be at 20% utilization rates in around twelve months’ time, which then should increase to 30 to 40% by the end of next calendar year.

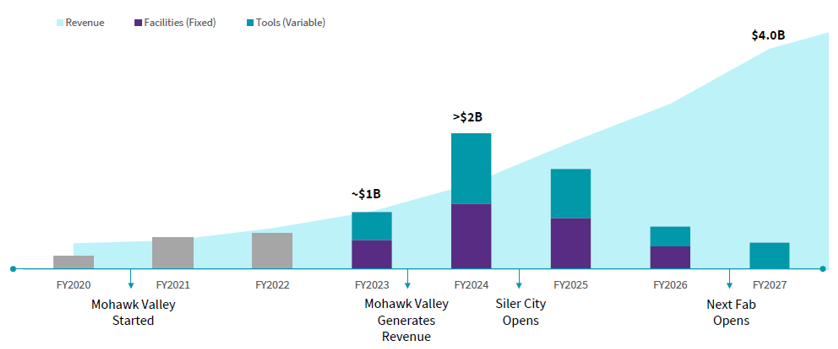

Bringing the above together, the following two slides are key to understand for investors. Due to the building out of these manufacturing sites, we’re currently looking at $2 billion of investment in fiscal year 2024 (2023 will end this month) and then another $1.6 billion in the year thereafter. The light shaded area is how Wolfspeed sees their revenues evolving. With the currently planned capacity, they’re forecasting to be able to get to $5 billion of semiconductor revenues in 2030.

On the revenue projections, the CEO commented as follows at the latest capital markets day: “When you take a look at the amount of design-ins that we need to continue to generate in order to hit those revenue numbers, we only need to hit a number that was roughly what we did last year in design-ins, which was around $6 billion. Last quarter, we did $3.5 billion. So we do not need to actually accelerate the design-ins further to hit the numbers that are on the chart.” This sound pretty reasonable, nothing overly excessive.

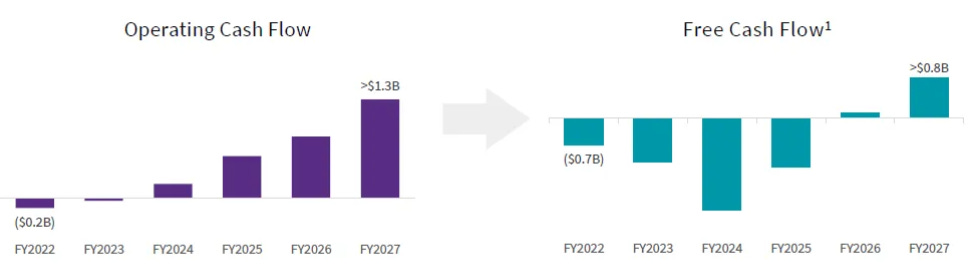

As capex rolls down over 2026 and 2027, the positive operating cash flows will start to get translated into positive free cash flows:

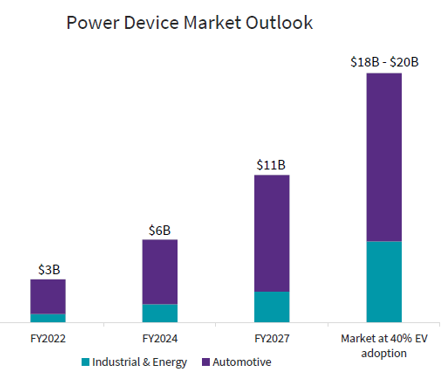

The company expects the power device market to be around $11 billion in 2027, and around $19 billion when the EV market reaches a 40% adoption rate, which the company reckons will happen by around 2030.

So building the facilities to generate around $5 billion in revenues would give the company a market share of around 25% in 2030. Clearly there could be a risk of overcapacity in the medium term. Although this can be mitigated to a large extent as the equipment installation in the fabs can happen on a variable basis, i.e. based on demand. So the way to visualize this is that each fab has a number of production lines, and you can add them one by one as you win contracts with customers.

The company’s view however here is that the shift to SiC is happening faster than expected, Wolfspeed’s CEO: “We get a lot of visibility from the tier 1 automotive suppliers. We get a really good look as to what's happening, faster than what's being published by publications, both on the material side, but particularly on the device side. I've heard back from one of one of the largest tier 1 suppliers, this company deals with every car company on earth, and his note back to me was 100% of their opportunities are silicon carbide. In the auto industry, I can't name a single car company that's planning right now an inverter that's going to go in production into a car in '27 or '28 that's silicon. So that there's a high likelihood that we're going to be capacity constrained in '26 and '27 when you start to look at those numbers. In fact, Mohawk Valley is completely full in that timeframe and the design-ins already support that.”

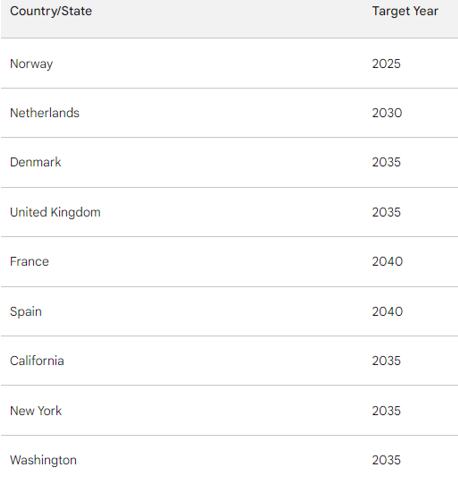

The trend is indeed towards countries and states banning the sale of gasoline powered vehicles. Bard was kind enough to make the following table highlighting all currently planned bans by region.

Clearly these regions are still amongst the economic powerhouses of the world i.e. California, New York, UK and France, while also China is making a big push into EVs. Therefore with the reduced volumes of gasoline powered vehicles, it is likely that the automotive manufacturers will go into losses for some years. My guess is that therefore these OEMs will decide to downsize their legacy businesses faster than the market expects, in order to mitigate losses, and scale up their EV manufacturing to turn this business, and the business as a whole, profitable.

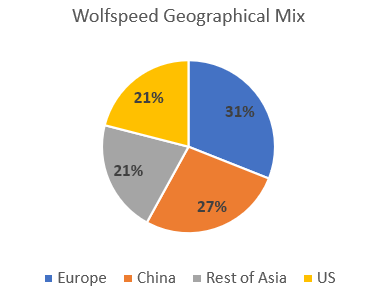

Wolfspeed’s revenues are geographically very diversified. The company seems to to have good relationships across the globe with semiconductor manufacturers, automotive suppliers and the OEMs themselves:

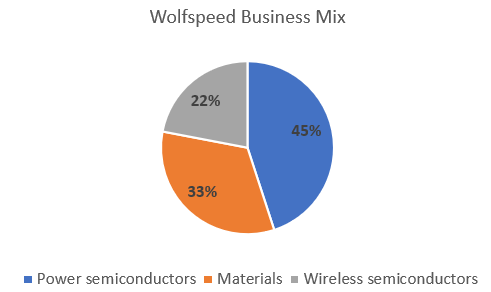

Currently the business has 45% of revenues coming from SiC power semiconductors with 33% coming from wafer fabrication (materials). As the power semiconductor business should see the highest growth rates, Wolfspeed estimates that by 2027 this business will contribute 70% to revenues, with 20% coming from wafers.

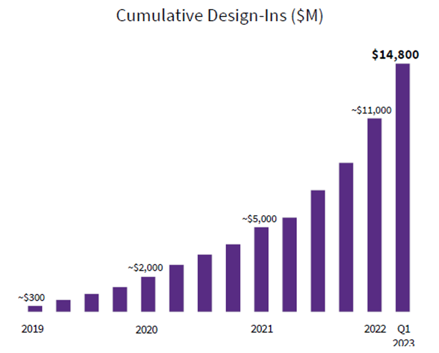

Wolfspeed has accumulated nearly $15 billion of design-ins since 2019, the chart below is from the latest capital markets day. A design-in means that a customer intents to purchase a product and has provided documentation detailing capacity needed. However, this doesn’t necessarily translate into revenues as the customer’s project can still be subject to change. When the semiconductor manufacturer gets its chip into a product that’s going to market, this is called a design-win. Wolfspeed mentions they have been getting a conversion rate of 43% turning design-ins into design-wins.

The above number of cumulative design-ins was raised to $18 billion during the latest quarter (Q3 of fiscal year 2023), so clearly the company is maintaining good traction.

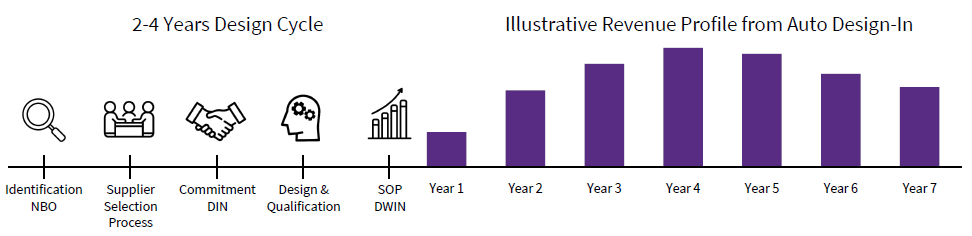

Getting design-wins for semiconductors in the automotive industry is a lengthy process. It typically takes around 2 to 4 years to get qualified by the automotive manufacturer, which will run lots of tests on your chips to make sure they continue to function well under a large variety of conditions as well as for a long period of time. The manufacturer needs confidence that your chip will last for more than 10 years and under both very hot as well as freezing temperatures. Once you get the design win, the chip manufacturer is looking at a long period of free cash flow generation on this chip, i.e. as long at the automotive model is in production. This is a much more attractive business than getting a win into a smartphone for example, as the model cycle is much shorter here.

Tesla comments

At Tesla’s recent capital markets day, they disclosed being able to reduce the SiC power semiconductor cost for their next-gen vehicle, which will likely be priced around $25,000, with 75%. “We designed our own custom package and we can extract twice as much heat out of that package as what we could buy off the shelf. And so what does that mean? It means that the silicon carbide wafer that's inside those packages can be much smaller. And silicon carbide, it's an amazing semiconductor, but it's also expensive and it's really hard to scale. On top of that, orchestrating all of these transistors and making them switch in the right ways is computationally extremely intensive. It used to require 4 microprocessors. We have developed our own custom microprocessor, it's purpose-built for high-power electronics.” - Tesla’s head of powertrain.

Wolfspeed’s CEO commented as follows during the recent Q3 call: “They're focusing on an entry-level car that has a pretty significantly lower power price point. When we look at the market for silicon carbide, we take an assumption that there's going to be a certain penetration of electric vehicles in the market and a certain penetration of silicon carbide in the electric vehicle market. And obviously, as we look at entry-level cars, historically, we would say there would be no silicon carbide going into that. So we view this as incrementally expanding the TAM because it takes silicon carbide down to a level where we weren't anticipating it. And we have obviously spent a ton of time talking to our customers that are building vehicles that are more mid range in terms of cost perspective. And their view is silicon carbide all the way.”

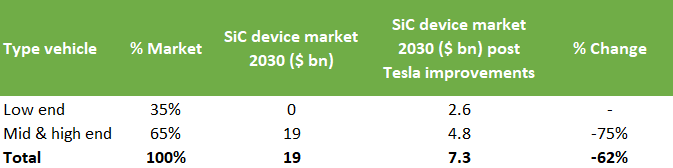

There’s a fair argument here, Tesla being able to add SiC to an entry level vehicle expands the total addressable market (TAM). However, the fact that Tesla designed a module which reduces silicon carbide content with 75% due to better heat dissipation brings a serious risk as well to the TAM. I’m assuming here a similarly designed module can go into their higher end vehicles and that other manufacturers will be able to reverse engineer this design.

At the Morgan Stanley conference, Wolfspeed’s CFO explained that they were initially assuming SiC content to go into 65% of electric vehicles. So if the 35% of lower end vehicles would add SiC as well, while the industry is able to reduce SiC usage with 75%, I end up with the below back-of-the-envelope math, i.e. ending up with a 62% reduction in the market size. Obviously this would be huge bear case scenario.

A couple of points though here. We aren’t sure yet to what extent Tesla’s claims can be extended across the range of their vehicles. Also, we aren’t sure to what extent this engineering can be replicated by the other automotive players. And, you could make the case that as SiC falls in cost, it will see much more widespread adoption, also in non-automotive applications, which will lift the TAM again. As such this potential issue is a bit wait and see at the moment.

Financials - share price is $49 at time of writing, ticker ‘WOLF’ on the New York Stock Exchange

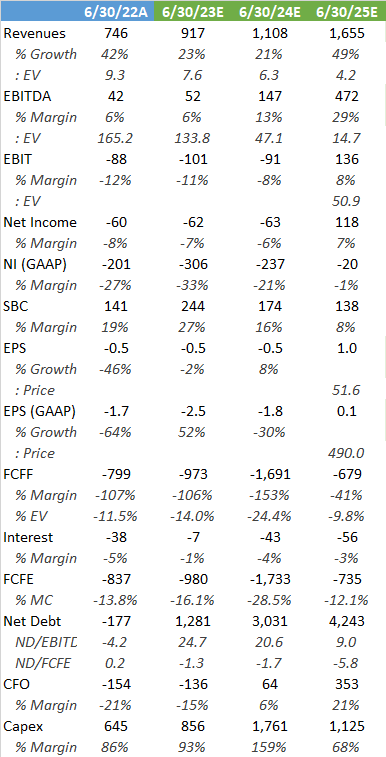

Below are Wall Street’s projections for the company. Valuation has started to look attractive at 15x June 2025 EBITDA.

However, the company will need more financing to build out the fabs. The CEO made the following comments at the Q3 call: “In terms of our capital needs, we continue to evaluate multiple avenues of additional funding, including upfront customer payments or investments, debt instruments and government funding in the United States and Europe. While we cannot comment on the timing or certainty of any government funding, we believe we have made great progress in this regard. In addition, we believe we need to secure approximately $1 billion of additional non-government financing between now and the end of the calendar year to support an approximate $2 billion of capex in fiscal 2024. The majority of this investment will be for 200-millimeter substrate facility construction and tool capacity both at Siler City and our Durham campus, with the intention of leveraging this investment to ramp the Mohawk Valley fab as fast as possible. While we are currently investing a modest amount of design work for the German Saarland fab, we don't expect to see significant facility construction-related capex until calendar year 2024 while we await final incentive notification from European authorities. However, we have made good progress on this front and, as of now, expect final notification later this calendar year.”

So they need another $1 billion this year, and then looking at that free cash flow chart again, probably around another $1 billion next year. So I’m assuming they need to raise $2 billion and as the company is already highly levered, they will probably need to come to shareholders for another capital raising.

The maturity profile of the current debt which is made up of convertible bonds looks fine, most of it matures in ‘28 and ‘29 when the business should be free cash flow positive. The $500 million principal to be repaid in 2026 should be able to get rolled over. However, if Wolfspeed’s share price performs well, these ‘26 convertibles will get converted into equity, which would bring an 8.5% dilution based on my calculation. The ‘28 and ‘29 convertibles are hedged to a share price of above $200, so risk of further dilution is low here.

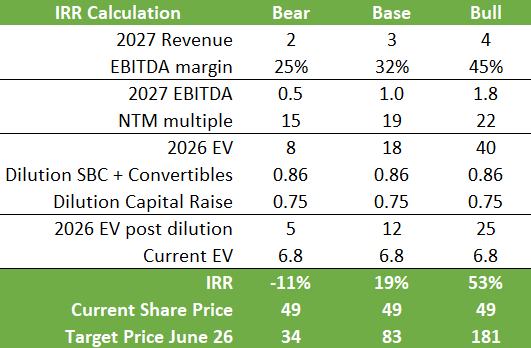

Ok, let’s have a crack to bring this all together and see whether it would make sense to buy these shares or not. Below I’ve modelled three scenarios, one base, one bull and one bear for 2027. For the base scenario, I’m assuming headwinds from a more competitive environment which would result in $3 billion of revenues at only 32% EBITDA margins. Under the bull scenario, the company reaches its $4 billion revenues target with the target EBITDA margin of 45%. Under the bear scenario, customers are also able to reduce SiC content resulting in Wolfspeed missing its target revenue by 50%, generating only 25% EBITDA margins. On these target EBITDA numbers, I’ve taken reasonable multiples as SiC should have a strong growth profile post 2027. Next, I’m modelling in a 5% dilution per annum which should cover both the share based compensation (SBC) as well as the dilutive impact from the 2026 convertibles. Then, I’m also modelling in a 25% dilution from a possible $2 billion capital raise. With these, we get to a 2026 EV of $12 billion for the base, $25 billion for the bull, and $5 billion for the bear. Overall, this makes me think the risk-reward is to the upside in these shares, as I get to an average IRR of 21% across these three scenarios.

Wolfspeed’s share price has come down a lot over the last year. One, obviously the macro headwinds had an impact. Two, the statements from Tesla raised concerns in the market. And three, the scaling up of the Mohawk Valley fab was slower than expected, which seemed to be caused by a delay in the installation of all needed electronics. Overall, one and three should be temporary issues, and the Tesla one is a bit wait and see for the moment.

Also compared to peers the valuation is starting to look attractive. Wolfspeed is currently on 7x NTM Sales while being exposed to the highest growth rates. For comparison, both Texas Instruments and Analog Devices are on 8-9x sales, while seeing much lower growth.

If you enjoy research like this, hit the like button and subscribe. Also, share a link to the research on social media with a positive comment, it will help the publication to grow.

If you like to read more, all my past research is here. I’m also regularly discussing tech and finance on my Twitter.

Disclaimer - This article doesn’t constitute investment advice. While I’ve aimed to use accurate and reliable information in writing this, it cannot be guaranteed that all information used is of such nature. The shares’ future performance remains uncertain. The views expressed in this article may change over time without giving notice. Please speak to a financial adviser who can take into account your personal risk profile before making any investment.

WOLF changed their name from Cree. They always have been BIG promoters with absolutely horrible execution. Now SIC years ago was LED etc. etc.

They never made any money

2020 2019 2018

Operating Income (160.2) (164.2) (209.3) (189.7) (61.9) 2.6

Will they be able to execute now? The start doesn't look promising. Already missing numbers and overpromising.

Chasing hot new ideas or products hasn't been smart investing EVEN in tech

ON semiconductor is my choice. Less risky