Summary

Valens is a smaller semi player focused on high-speed video and audio connectivity. This market is expected to see high growth rates due to the rising automation levels of cars, with increasing amounts of sensors having to be connected. The company has been an innovator in the field, with their engineering developments being incorporated in industry standards, which resulted in some high-profile design-wins. For instance, the company’s chips are being shipped in all of Mercedes’ latest models. And there is substantial scope for further design wins from other automotive manufacturers.

On top of this potentially high-growth automotive semi business, the company already has an established audio-video semi business with well-known customers such as Samsung, Panasonic, Siemens, and Medtronic. This division saw attractive double digit growth rates last year. Overall gross margins for the company are over 60%, a pretty strong number for a semi company.

Despite these several attractions, the shares are trading at an undemanding valuation of 1.3x EV / NTM Sales, or 2.9x Market Cap / NTM Sales due to the high net cash position. Semi peers with similar gross margins trade at valuations of around 3 to 12x EV / NTM Sales, some of which with much lower potential growth profiles. Valens looks to be under the radar, with the company being covered only by a few sell side analysts, as the free float is also way too small for the large institutional money to get involved.

Naturally this is a higher risk name, with the company only having a few selected number of chips revolving largely around one type of technology. Although at current valuations, I’m regarding the risk-reward profile as starting to look quite appealing, meaning the expected upside should be far greater than the potential downside. If they can successfully announce some further design wins within automotive, we get a clear path for revenue growth, likely combined with multiple re-rating. Obviously the shares will work well here. A blue-ish sky scenario of $400 million of revenues within the coming five years or so, would make revenues go times more than 4, and the market cap to sales ratio times 2 or so, resulting in an 8-bagger.

Do me a favor and hit the subscribe button. Subscriptions let me know you are interested in research like this, which is a good motivation to publish more. Special thanks to the 700 subscribers so far!

Automotive Semis

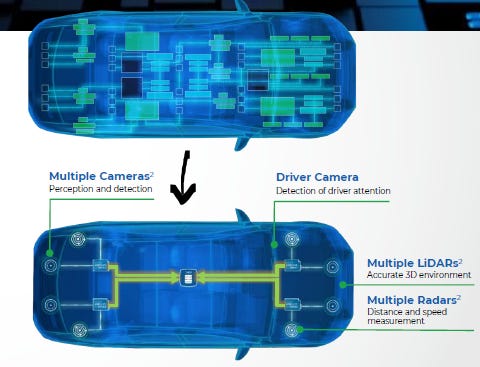

As the automation levels of vehicle movement will only keep increasing over time, the number of sensors onto a vehicle similarly should stay on a rising trend:

This is where Valens’ connectivity chips come in, handling the high-speed transfer of large amounts of data over a vehicle’s cabling. What sets the company’s designs apart are firstly the speed, which is near instantaneous. Secondly, the bandwidth, which enables the transfer of data with zero compression. Thirdly, the resilience of the data to electromagnetic distortions. Finally, the ability to transfer all needed data over one cable, as opposed to have separate ones for each type. This last characteristic allows for the vehicle’s weight to be reduced, resulting in lower costs, both in manufacturing as well as in driving. Valens’ presentation mentioned the car’s cabling to be the third heaviest component of a vehicle, behind the engine and the chassis.

Valens’ CEO gave some more details at the Deutsche Bank conference:

“Electromagnetic influence is one of the biggest challenges of the automotive industry in the future. We require more and more bandwidth and the higher the bandwidth, the noise is exponentially higher. Meaning 8 gigabits will have far more than twice the noise of 4 gigabits and our technology is actually unique by the ability to overcome those hassles. And available to do it in copper cables. Where a cable is starting to be damaged and age, you can still use the cables. In addition, when the cable is going to end its life, our chipsets will know that and will know to alarm about it.”

An illustration of how the car’s cabling can be reduced:

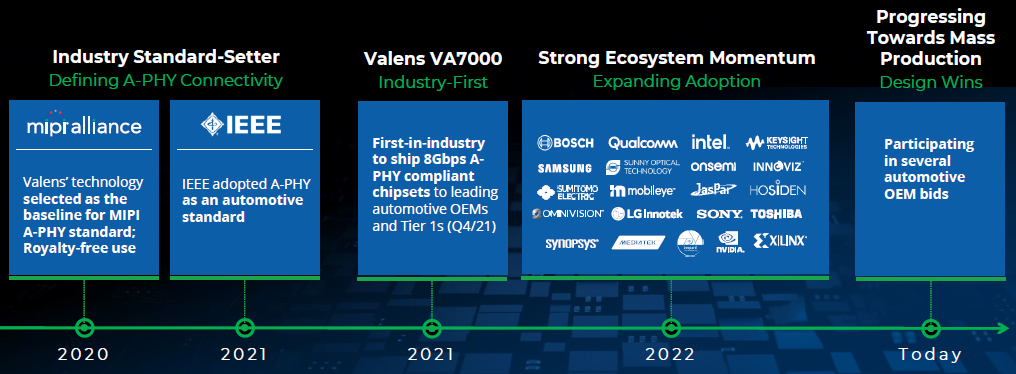

Valens’ tech has been embraced by Mercedes, with the chips now being found in their latest models, including the S, C, and E-classes, powering the infotainment and telematics systems. The tech also formed the basis for the creation of a new IEEE standard, known as MIPI A-PHY. Companies that participated in this development include Intel, MediaTek, ON Semi, Qualcomm, Robert Bosch, ST Micro, Synopsys and Toshiba.

Valens’ latest VA7000 chip is the first introduced chip worldwide which is fully compliant with this standard. This chip is currently being evaluated by more than 20 OEMs and tier 1 suppliers. JASPAR, the Japanese automotive organization which includes Toyota, Nissan, Honda, and Denso, has already validated the chip, clearing all the required tests. Good news overall.

The company made the following slide to give an overview of these developments:

Valens is also in collaboration with Intel to enable foundry customers to implement this standard. This opens the door for competition but Valens’ view here is that it is better to grow the ecosystem and the market, and subsequently take a smaller part of this large pie. Nivruti Rai, vice president at Intel, commented:

“Our priority at Intel Foundry Services is to invest in disruptive technologies that can help our customers accelerate time to market. As the most cutting-edge high-speed connectivity technology in the automotive industry, MIPI A-PHY is well positioned for large-scale integration in cars around the world.”

Like many other semi success stories, such as Nvidia, Marvell or Broadcom, Valens is a fabless semi manufacturer. Meaning the company is focused on the entire design of the chip with the manufacturing being outsourced to a foundry, usually in the far east. Currently all manufacturing is taken care of by TSMC in Taiwan, although the above mentioned partnership could indicate that Valens might shift production to Intel’s foundry in the future.

It would be nice if MIPI A-PHY was the sole novel tech which could achieve these capabilities. Alas, there is a competing standard and ecosystem. The Auto-SerDes standard has similar capabilities and similarly has a powerful set of promoters. This is an obvious competitive risk to be aware of.

Valens held a capital markets day around the time of the IPO two years ago, where a number of interesting shakers presented. Martin Bornemann, director at Aptiv gave the following outlook:

“The number of camera and radar sensors will increase significantly in the near future. We are working with Valens on their MIPI A-PHY technology in order to address these requirements from the market. This technology allows us to realize the necessary harness technologies with lower costs compared to other interface technologies. And it is also a way for us to replace other proprietary solutions with one IEEE standard. Valens is an important partner for Aptiv for the future of vehicle architecture solutions.”

Ziv Aviram, co-founder of Mobileye, commented:

“It is clear to me that the transmission of high bandwidth data is escalating fast and has become a real challenge in the noisy environment of cars. Valens and the MIPI A-PHY standard are the solution to transfer high-speed data and protect it from errors. And they can do it while reducing total system costs. Knowing the company and the management, I'm excited to watch as Valens continues to impact the automotive industry.”

Eyal Waldman, founder of Mellanox which was later acquired by Nvidia, disclosed that he was an investor in the company.

“As an entrepreneur, I've invested in Valens because I believe in the team and I believe that their technology solutions will drive the autonomous market.”

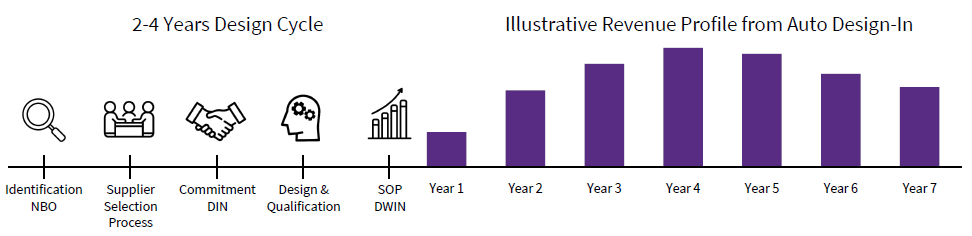

The company’s management is expecting to be able to announce a number of automotive design-wins for their latest chip this year. Now the semiconductor evaluation cycle in the automotive industry is a lengthy process. It typically takes around 2 to 4 years to get qualified by a manufacturer, who will run a battery of tests on your chips to make sure they continue functioning under a large variety of conditions, as well as for long periods of time. Once you get the design win, the semi manufacturer is looking at a long period of free cash flow generation, i.e. as long at the automotive model is in production. This is a much more attractive business than getting a win into a smartphone for example, as the model cycles are much shorter here.

An illustration from Wolfspeed explaining this process:

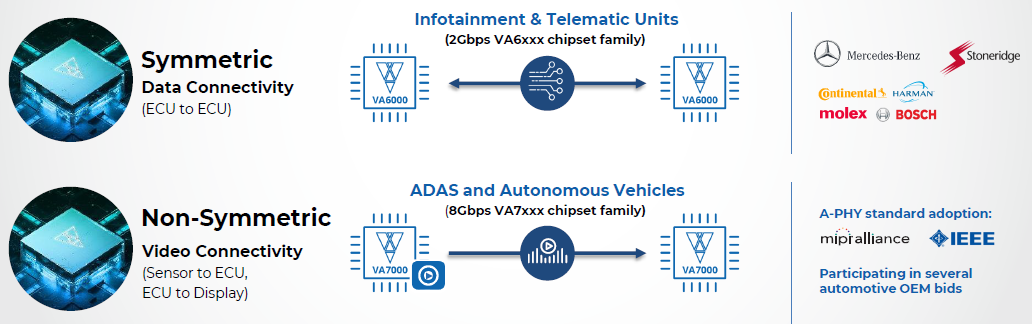

Valens supplies two main types of automotive semis currently. One symmetric chip aimed at providing the connectivity between multiple electronic control units, named the VA6000. And another asymmetric chip, the VA7000, to handle data connections from the vehicle’s various sensors to an electronic control unit.

Besides Mercedes, also Stoneridge has already decided to introduce the VA6000 in one of their systems. The chip will take care of the data traffic between a camera at the end of a truck’s trailer and the truck’s infotainment system.

Valens’ CEO gave some more details on this win at the Deutsche Bank conference:

“We have a nice design win with a leading company in the trucking industry named Stoneridge, which is actually one of the world's top tier 1 suppliers for trucks. We are doing a safety system with a back, reverse camera. Many people are not aware, but all those trucks don't have reverse camera. The technology needed to see the picture in the back was a huge technological barrier. Many tried and failed but our chips solved the problem.”

He also gave an update here on the recent Q1 call:

“Stoneridge continues to promote the tractor-trailer rear-view safety solution for fleets and drivers and has expanded the collaboration with partners to do so. In Q2, we expect to record initial sales of this solution to Stoneridge for their fleet operator customers who will be doing fleet-wide evaluations. We expect revenues to ramp up in 2024.”

The Automotive Semi Market

By 2025, the annual car market is estimated to be around 100 million vehicles. At an average of 10 sensor links per vehicle, and two connectivity chips needed per link, one for the transmitter and one for the receiver, this results in an annual market of 2 billion connectivity chips. The average selling prices for these types of chips are around $4, meaning that the total annual market could be valued at around $8 billion under the above data. Note that premium-type vehicles typically have more sensors, while lower range vehicles have less. Also, as we move from vehicle automation levels of 2-3 to 4-5, the number of needed chips is expected to increase from 10 to around 20 or 30. So overall this market should be exposed to a strong growth dynamic, with automation levels in vehicles increasing over time, resulting in an attractive CAGR in the number of needed connectivity chips. A risk to this TAM here could be ASPs coming down over time, although this could be offset with further innovation and which actually could also lead to further price increases.

If Valens would be able to capture 5 to 10% of this market in the near future, this could give a revenue opportunity of $400 to $800 million. Which looks very attractive compared to the $90 million they’re generating currently. And with still a strong possible growth trajectory thereafter due to the further increases in the number of connectivity chips.

On the competitive environment, Valens’ head of automotive made the following comments at the capital markets day in ‘21:

“If we focus on the growth area of Valens, which are the asymmetric links, where we are deploying the A-PHY technology, we see two main competitors. One of them is Texas Instruments and the second one is Maxim that was recently acquired by Analog Devices. How do we differentiate versus those two competitors? First of all, on the technology side, our core technology is digital. It's based on a DSP (digital signal processing). And the ability of us to scale up our technology is much more significant than our competitors who are based on analog technology. So I would say if you look at what the industry is requiring for the high speed links, which is connecting sensors to ECU, you need high bandwidth, you need zero latency and you need error free links. The scalability of the bandwidth is much more possible with our digital technology we are deploying, today 8-Gig moving to 16-Gig and then 32-Gig in the future. Our competitors are struggling to scale up the bandwidth from an electromagnetic interference immunity. Electromagnetic interference is one of the key challenges for the car industry moving forward if you think about advanced driving assistance systems (ADAS). So you must have resilient high speed links to make sure that the ADAS systems are immune to internal and external noise. Our technology gives an order of magnitude better electromagnetic immunity, and this is how we are delivering what we call error free links to the customers.”

There are some useful insights from these comments but going forward there should be more players able to offer chips compliant with one of the two standards, moving away from analog. There are a number of strong semi companies active in the automotive space which will likely be looking to compete in this area, such as STM, NXP, Infineon, Renesas, Bosch, Texas Instruments, Analog Devices and ON Semi. We’ll probably be looking at around 10 manufacturers or so which might be able to provide a competing solution. But this should still allow Valens to take a share of 5 to 10% or so, which would be a great result for shareholders.

Audio-Video Semis

The second business unit is Valens’ original business and still comprises today most of its revenues. The company developed a standard here as well, out of which the MIPI A-PHY automotive standard eventually evolved. The standard for the audio-video market is HDBaseT, which similarly enables high-performance connectivity over longer distances, i.e. up to 100 metres. Co-founders of this standard include Samsung, Sony, and LG.

HDBaseT basically enables the transmission of ultra-high definition video and audio over a single ethernet cable, avoiding cable clutter, and at near zero latencies, which is measured in a few microseconds. The technology is applied in video conferencing systems, industrial vision, medical imaging, and commercial advertising. Valens’ customers include some well-known names such as Samsung, Siemens, Panasonic and Medtronic.

A few of the latest products in which Valens’ chips have been embedded:

A director from Panasonic presented at Valens’ capital markets day on how they made the move from analog to digital:

“Valens’ HDBaseT chip has been essential to our projector and professional displays, changing the industry from an old-fashioned analog system to a more innovative digital-based platform. Our partnership started in 2012, as the first projector manufacturer to embed Valens’ chip.”

A Logitech director gave some further details on how Valens’ tech is useful in avoiding cable clutter:

“If you look at a typical video conferencing system, there are so many different types of signals that flow through that need to be deployed. You have one or more displays in the room. You have USB connections to cameras, microphones and speakers. There's ethernet and HDMI content sharing. There's many different types of signals and cables that have to be deployed and managed, so it's really important to use technologies like HDBaseT to streamline your implementation. Otherwise your cost and complexity just goes through the roof.”

According to Fortune Business Insights, the global video conferencing market is growing at annual double digit rates, while the market for industrial cameras is growing at higher single digits.

Overall, I think audio-video is a decent business, although there is some risk of technological disruption over time with novel standards being able to take over parts of the market.

IP portfolio

Taken from the most recent annual report:

“We consider the strength of our intellectual property portfolio to be among our most significant competitive advantages. We own approximately 116 issued patents, and 7 pending patent applications. Our patents generally cover a wide variety of areas relevant to our products, specifically covering our innovation in the areas of convergence of multiple-data types / multi-stream over the same wires, and robust operation under severe electromagnetic interference.”

R&D roadmap

Valens’ head of Automotive discussed the following R&D roadmap at the capital markets day:

“And we spoke a lot about sensor to ECU connectivity, this is the VA7000 family. We are now designing the VA8000 family. It will be supporting not just the sensor to ECU connectivity, but also the ECU to display connectivity. We also have the next level of bandwidth all the way up to 16 Gig. So definitely, we are working with R&D step by step, reusing the core IP that we developed for a certain family and then expanding and enhancing it for the next family in a similar way to what we've done with the VA6000 to the VA6003.”

During the latest Q1 call, the CEO discussed R&D efforts in Audio-Video:

“We continue to invest in expanding our offering for audio-video verticals. Most recently, in Q1 2023, we taped out the VS6320 chipset, a key milestone for market readiness of this product, which is aimed at long reach extension of USB3.2. The increasing demand for higher bandwidth for USB peripherals is driving the adoption of the USB 3.2 standard globally across verticals and Valens VS6320 is ideal for connecting the many remote USB 3.2 peripherals required in videoconferencing, industrial, and medical applications.

The VS6320 is extremely differentiated compared to other alternatives. It's a highly integrated single chip, hence, dramatically smaller, less than half the power consumption, and yet still at a better cost. Conversation with prospective customers for the VS6320 continue to progress, and we expect relatively quick adoption by them. We anticipate first engineering samples to be shipped by the fourth quarter of this year, and we believe our customers will introduce the new products embedding the VS6320 during the second half of 2024.

We also continue to gain traction in audio-video for multi-camera video conferencing applications, which we believe will be one of the fastest growth areas for audio-video equipment.”

Management

CEO Gideon Ben Zvi has a background as a serial entrepreneur as well as in venture capital. On his LinkedIn he mentions that three out of four companies he founded had a successful exit: Ligature (acquired by Wizcom), Wizcom which was subsequently IPO’d, and BriefCam, which was acquired by Canon Japan. He took over as Valens’ CEO in 2020, after having been on the board since 2011.

- YouTube")

CFO Dror Heldenberg held previously the CFO position at several companies: Compass Networks, Broadlight - which was acquired by Broadcom in 2012, and Pelican Security - which was acquired by Microsoft in 2002.

Chairman Peter Mertens was CTO at Volvo for six years, an executive at General Motors for eight years, and held various management positions at Mercedes. He joined the Valens board in 2020.

Gabi Shriki, Head of Audio-Video, joined Valens in 2015. He previously managed the Mobile Connectivity business at Texas Instruments.

Gideon Kedem, Head of Automotive, joined Valens in 2020. He has over 30 years of experience in semiconductors at companies like Intel, Cadence and Xilinx. Prior to joining Valens, he managed sales and business development at Xilinx for the EMEA and India regions.

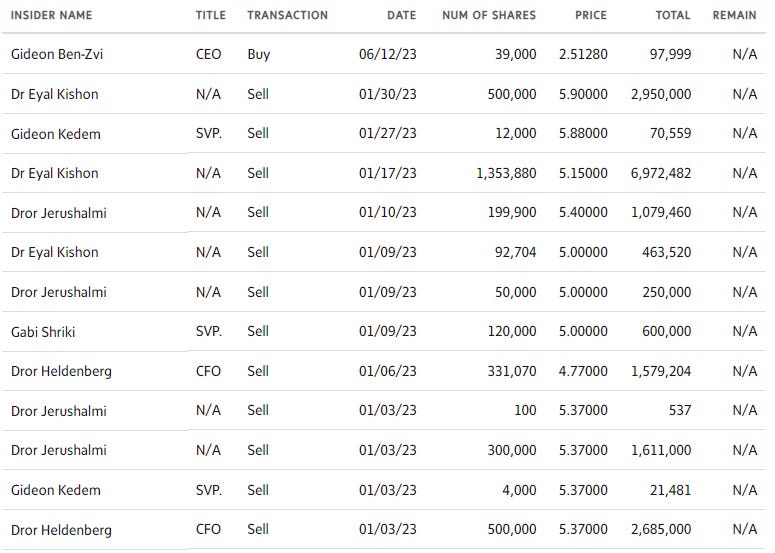

Insider trading

Insiders have mostly been selling this year, with all of sales happening in January at a share price of around $5. Although the CEO did make recently a decently sized purchase of around $98k at a share price of about $2.5.

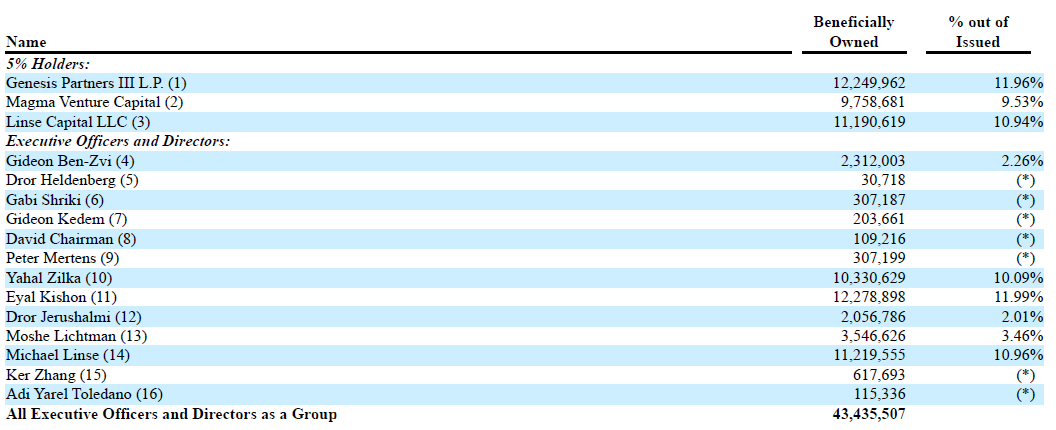

Comparing this to the latest shareholder ownership data from the annual report below, with positioning being reported as at February 10, the CEO held 2.3 million shares already. Dror Jerushalmi, who was a larger seller last January, is similarly holding on to 2 million shares. The same conclusion can be made for Eyal Kishon, who despite after selling 1.9 million shares in January, is still sitting on another 12 million of them. Both the heads of Automotive and Audio-Video own 200k and 300k shares respectively. The only executive who has a minimal position is CFO Dror Heldenberg, who has nearly sold all of his shares.

So overall, a few mixed signals here. Clearly insiders are still largely invested with the CEO increasing his position while the CFO has mostly liquidated his. Now, he might have valid reasons for doing this, maybe he’s looking for his family to move into a better home, or he might be planning to make a move to another firm, e.g. to move up to a CEO role. Overall, I wouldn’t be overly concerned here after having done this analysis.

As a side note, some investors read too much into these transactions. “Palo Alto’s CEO sold $500k of shares, this stock is ready to tank, good luck” are some of the comments you might come across on social media. What is often being missed here is that there are other factors at play as well in the decision making of the insiders. Valid reasons to take some money off the table can include a desire to diversify assets, moving into a better home, or investing in the education of your children. Take the example of AEHR, where insiders have been selling continuously and the share price has gone from $1 to $40 over that period. Yes, you read that right.

Financials - share price at time of analysis is $2.5, ticker ‘VLN’ on the NYSE

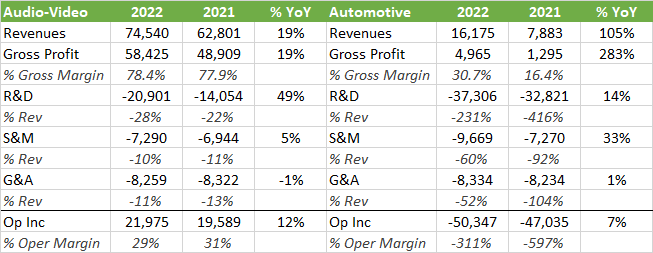

Audio-Video is still the main business line and according to the latest annual report, is generating a healthy operating margin of around 30%. Automotive is the business unit where the company is expecting most growth, although here they are still burning cash, mainly due to high investments in R&D as well as lower gross margins as this business is still scaling up.

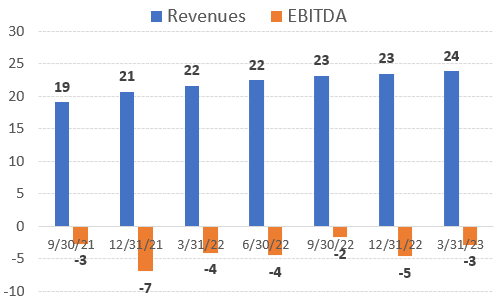

Quarterly revenues have been on a nicely upward trajectory, with a modest burn of around $3.5 million dollars per quarter over the last four. Given that the company is still sitting on $135 million of net cash while guiding the market they’ll be able to break-even at the end of this fiscal year, the overall financial position is a healthy one.

The CFO’s latest comments on this at the Q1 call:

“We remain on track to reach adjusted EBITDA break-even by the end of 2023, which means that in 2024, we expect the company will reach cash flow profitability.”

At the ‘21 capital markets day, the CFO outlined the following goals for ‘26, Valens’ five year plan sort of: revenues of $482 million, gross margins at 64% and EBITDA margins at 42%. They also mentioned that they were expecting to be able to announce two further automotive design wins within 18 months. We’re sort of passed that point now and during the last quarterly call they were guiding the market to be still able to make these later in the year. Now, getting designed in into a major automotive player’s models is a lengthy process so I’m happy to give them some slack here for the moment.

The CEO commented on this at the latest Q1 call:

“Talking about the VA7000, we are engaged in several bids by some OEMs. Today, I can tell you that these bids progressed according to plan, and we are on track to announce our initial design wins this year as we communicated in the past.”

Overall, around half of sales last year were made through distributors with the other half being made through the direct sales channel. This is a fairly typical mix for semi companies. The company was able to pass through some price increases last year, due to the inflation they were seeing in input costs. Valens also mentioned however that they did have to increase payroll expenses with $5 million, the main reason being a shortage in semi engineering talent.

The entire semi engineering team is based in Israel, occasionally a volatile region, which introduces some level of risk. This also means that the cost base is largely in Israeli Shekels, with revenues being generated in USD. So a strong appreciation of the Shekel vs the Dollar can weigh on profits in any quarter and vice versa.

The valuation is starting to look pretty attractive here. Currently Valens’ enterprise value (EV) is valued at 1.4 times next twelve months’ sales, whereas peers making gross margins of above 50% are typically valued at around 3 to 12x sales. If you assume that Valens will burn most of their cash, the market cap to sales multiple might make more sense here which is around 3x. So if Valens can successfully announce some further design wins within Automotive, we get a clear path for revenue growth combined with multiple re-rating. Obviously the shares will work well here. A blue-ish sky scenario of $400 million of revenues within the coming five years or so, would make revenues go times 4, and the market cap to sales ratio times 2 or so, which would result in an eight bagger.

The shares have strongly de-rated post IPO and in my opinion are now starting to look attractively valued from a risk-reward perspective, i.e. having much more expected upside than downside.

If you enjoy research like this, hit the like button and subscribe. Also, share a link to the research on social media with a positive comment, it will help the publication to grow.

If you like reading more, I’m regularly discussing tech and finance on my Twitter, and you can find all my past research here.

Disclaimer - This article is not advice to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it cannot be guaranteed that all information used is of such nature. The views expressed in this article may change over time without giving notice. The mentioned securities’ future performances remain uncertain, with both upside as well as downside scenarios possible.