Introduction

Uber’s CEO: “Our strategy remains to build best-in-class verticals across Mobility and Delivery and our Q2 results demonstrate that strategy is working. We reached two important milestones: our first-ever GAAP operating profit, $326 million, and our first quarter of free cash flow of more than a billion dollars, $1.14 billion to be precise.”

Going through corporate results, Uber’s FCF generation during the last quarter of over $1 billion caught my eye. Simply annualizing that number and putting it on the current EV (i.e. Enterprise Value = Market Cap + Net Debt), gives investors a FCF yield of 5%. For a company where its core businesses are still growing at top line rates of 15 to 40%. While its incremental margins, i.e. the additional EBITDA the company is generating on those grown revenues, are around 30%. This is a clear set-up for a potentially nice compounder..

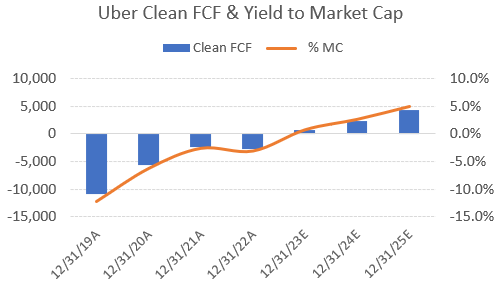

Now, Uber is still awarding employees with share based compensation of around 5% of revenues, a dilutive cost to shareholders which isn’t reflected into FCF. So let’s try to clean this FCF number up. We can define the clean FCF as FCF minus interest expenses and minus share based compensation. It is thus the real FCF which is available to equity holders after the debt holders have been paid and taking into account dilutive compensation schemes. The chart below illustrates how Uber is now starting to break-even on this metric. And as the company should be able to continue to improve this trend in profitability, this would result on Wall Street’s numbers in a 5% clean FCF yield to the current market cap in two years’ time.

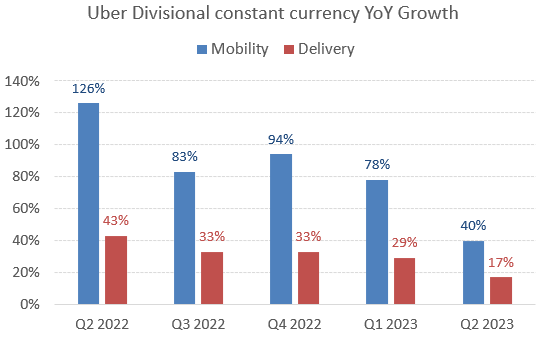

As already mentioned, Uber’s top line growth rates are expected to remain attractive for quite some time..

.. While it’s incremental EBITDA margins hover around attractive 30% levels:

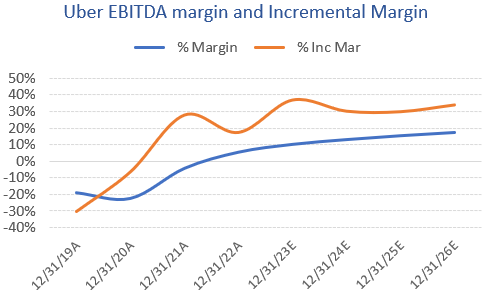

If Uber can continue to move their margins up over time towards those of other online booking platforms such as AirBnb or Booking Holdings, there is obviously a lot of upside on the EV to Sales multiple. Currently each of these businesses are valued on EV to EBITDA and PE metrics, so if Uber keeps showing nice progress on their margins and top line, obviously this should translate into strong share price performance.

Business and industry analysis

What Uber does probably needs little explanation, it is basically an app where you can order a ride or a meal. These services are provided by people in your area who drive around in their car, on their motorbike or in their tuk tuk (rickshaw). Uber subsequently takes a cut from the service fee you pay them.

The ride sharing market is extremely consolidated on a per country basis, as its marketplace benefits from huge network effects. Drivers will only be active on platforms where they get large volumes, while consumers will only order rides on platforms where there is a large availability. Therefore, it is extremely hard for a new player to come in, if you have no riders, you won’t be able to convince any drivers to provide services on your marketplace. Similarly, when there are no drivers on your platform, no one will install your app. Therefore the ride sharing market is typically a two-player market in most countries.

According to Bloomberg Second Measure, Uber currently has a 74% market share in the US, with Lyft occupying the remaining 26%.

Both players are commenting to not want to compete on pricing, but rather on quality and app features. Lyft was historically somewhat more expensive compared to Uber, but over the last year they’ve been closing this price gap. However, the goal is not all to move to a discount, but rather to match Uber’s pricing. Reading through interviews, both CEOs are well aware that a pricing war would hurt both of them, which is obviously in no one’s interest. Uber for their part is taking pricing up in some markets, whereas in others they’ve been able to reduce it. Uber’s CEO explained this at the Morgan Stanley conference:

“Lyft was not competitive in terms of pricing, 9 to 12 months ago, they've taken some tough actions, and they are competitive in pricing now. Generally, our pricing is quite comparable to Lyft. And that has resulted in a, I'd say, constructive competitive marketplace. And we've taken booking fees up in certain markets, for example, Los Angeles, where due to the tort environment and certain abuses, we think insurance costs are significantly higher than they are. Pretty much anywhere else in the country, we increased booking fees. And then in certain other markets, where we have seen effective tort reform, Georgia or Virginia, we're able to take prices down for consumers.”

So what you’re reading here is a typical oligopoly at work. Uber is the dominant player and sets the pricing for the industry, allowing them to make sufficient profits. And then subsequently Lyft follows in pricing. This is a good situation for investors.

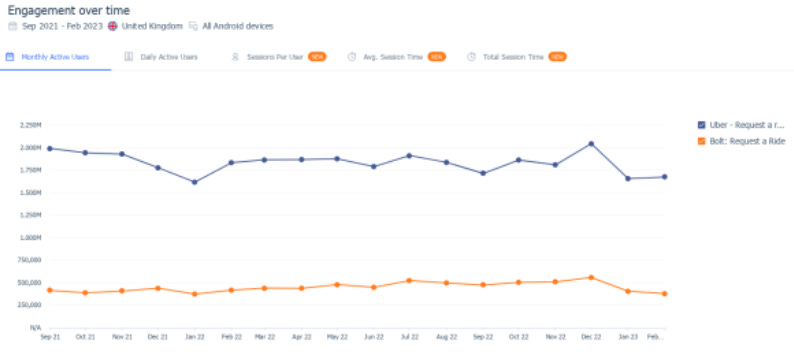

Similarly in the UK, the only sizeable player competing with Uber is Bolt. The chart below taken from SimilarWeb is somewhat vague, but it shows monthly active users for Uber in blue and those for Bolt in orange.

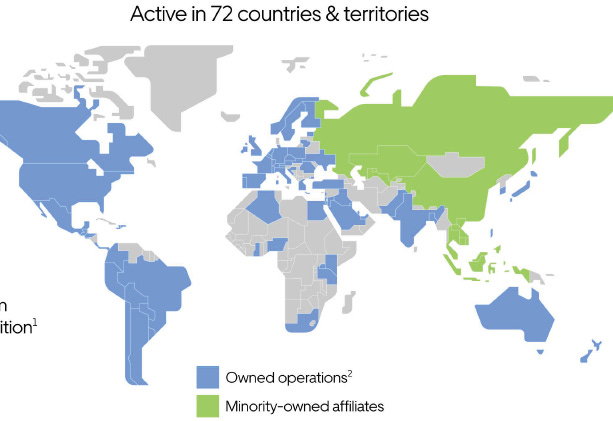

Overall, Uber is active in 72 countries, from the capital markets day:

And there are still strong growth opportunities within these, Uber’s CEO: “Even in our major markets, less than 10% of the population over the age of 18 uses Uber on a weekly basis. That number is even lower in several large economies, including Spain, Germany, Argentina, Japan, Hong Kong, and South Korea, where we see lots of opportunity to grow. In Q2, those markets together generated over $3 billion in annualized Gross Bookings (18% of total mobility bookings) and grew over 135% YoY on a constant-currency basis. Even in our top markets like the UK, France, and Canada, we see a large opportunity to grow outside our urban cores in London, Paris, and Toronto respectively. For example, our business in the UK outside of London in cities like Manchester and Birmingham grew roughly 45% YoY on a constant-currency basis.”

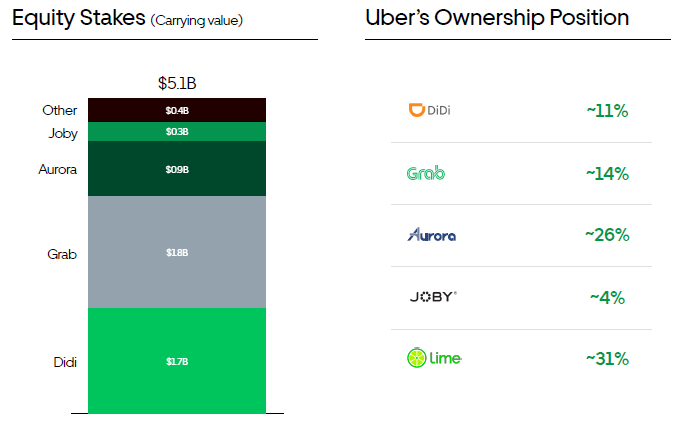

The company also has exposure to China and South-East Asia via their stakes in Didi and Grab. It recently divested its Russian ride sharing business to Yandex, the Russian Google.

The profitability profile of their other key business, Delivery (Uber Eats), has been gradually improving. Historically, I was a lot less enthused about this business compared to ride sharing, as food delivery is a much more competitive market. In London, I can probably order food from five platforms and then each restaurant chain will have its own app as well, and there are a plethora of options for grocery deliveries as well. That said, deliveries are now starting to generate decent margins, while at the same time the Freight business has gotten close to break-even, more on this one later.

Uber Delivery’s restaurant penetration rates are still reasonably low, at around 20 to 40% depending on the market. I can imagine that local restaurants want to be present on as many delivery platforms as possible, in order to maximize revenues. Certain large chains are negotiating exclusive deals however, Domino’s Pizza for example signed an exclusive deal with Uber Eats.

Due to the rise of online food ordering, there has been the emergence of ‘dark kitchens’, also called ghost kitchens. This is basically a kitchen unit you can rent somewhere without a physical restaurant attached, to purely focus on online business. An example of Deliveroo dark kitchens in the UK:

Uber’s take rate has become a messy affair. Traditionally it was defined as revenues to gross bookings, so basically the cut that Uber is taking from the ride or delivery. However, in some markets such as the UK they had to change the accounting, effectively booking the entire price paid by the customer as revenues, and then accounting for the driver under costs of revenues. This obviously boosts the take rate, but depresses margins.

Uber’s CEO explained this on the Q2 call: “The reported take rate was 29%. But if you adjust for the UK merchant model change, which happened a year ago, the underlying take rate was actually 21%. On an underlying basis, the take rate decreased by 30 basis points because we made some supply investments in some international markets, particularly LatAm and APAC.”

Obviously it would be far more helpful if they would just start reporting this real underlying take rate rather than this messed up one. Even one sell side analyst was confused by it on the Q2 call, thinking Uber had generated a record take rate.

New growth drivers

Uber’s CEO: “Our suite of non-UberX products together grew over 80% YoY in Q2, generating nearly $8 billion in annualized bookings (or 12% of Mobility Gross Bookings). We continued to improve Uber Reserve availability, including for airport pickups, while driving significant reliability improvements. We also made progress on our low-cost offerings, expanding UberX Share to 50 markets globally and Uber Moto, our bike taxi product, to additional cities in Argentina. In Q2, riders who took at least one Moto trip in a given month had 1.8x greater engagement than average.”

Uber Moto and Auto (i.e. 3-wheelers, commonly referred to as ‘tuk-tuks’), are especially attractive in emerging markets, where roads are often congested. The company commented that tuk-tuk services are in hyper growth mode in India, and are seeing strong growth for motorbike demand especially in Latin America.

Uber’s Head of Rides at the capital markets day: “In many parts of the world, 2- and 3-wheelers are really popular both as mobility and delivery vehicles, thanks to their low cost and small size. These have also proven to be a great user acquisition lever, 10% of all first time riders last year came through a 2-wheeler or 3-wheeler trip. Both of these businesses have recovered faster coming out of the pandemic than our core business and are profitable in 9 out of 12 operational markets despite the lower price point.”

The company also introduced a membership plan, Uber One, which gives you unlimited free food deliveries in your area and a 5% discount on rides. This is a smart move to lock consumers in and boost their app usage. After Amazon introduced Prime memberships, subscribers more than doubled their spend on the platform, while Uber mentioned that subscribers have been increasing their spend with 50% after becoming members. Currently 27% of Mobility gross bookings and 35% of deliveries are coming from members.

Advertising revenues might look small at only 2% of revenues, but this is a very high-margin business, with likely operating margins of over 50%. This would mean this business could be contributing already 10% to EBITDA, and even more to EBIT..

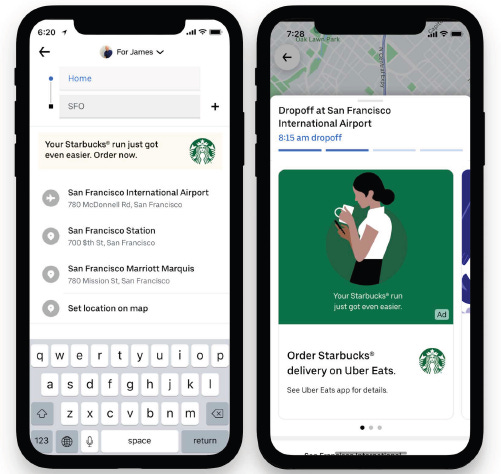

Personally looking at the ad below, it doesn’t really make sense to me. You’re in the middle of booking a ride and suddenly Starbucks logos are being shown. I wouldn’t even pay attention to these and even if I did, I’d probably find it rather confusing what Starbucks has to do with me booking a ride to the airport.

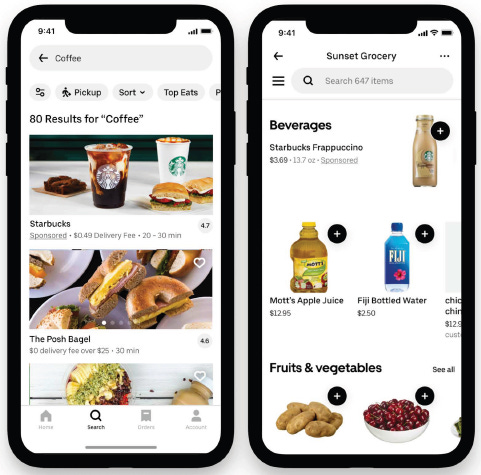

The below ad makes a lot more sense, I’m ordering a coffee from Uber Eats and now the top listing is a sponsored one from Starbucks. There’s clearly context here for why the ad is being shown and in my opinion, the consumer is quite likely to tap on it.

Uber mentioned that businesses who buy ads on their platform see a 7 to 9-fold return on that spend. Looking at the ad above, this looks likely.

Also getting regular taxis onto the platform should be a growth driver, as obviously this is still a big market. Uber’s CEO updated investors on this topic during the Q2 call:

“We just want to wire up every single vehicle in the world that's available to move people or things around, and you saw our efforts in terms of transit, for example, buses and subways and/or taxis that we used to compete with. Now we think we should have every single taxi on Earth on the platform. So that was one trend that we have been focused on, not just in the UK but around the world.”

Similarly other forms of transport such as flights, trains, and tour operators can now be booked on the app, Uber’s CEO:

“We've now expanded into flights as well. And we're actually seeing engagement with users being higher than we thought, and we're not seeing cannibalization of the base business. So we're quite hopeful of that business. And again, that tour operator market in the UK is a very, very large market that we can go after.”

The company is also expanding Uber Eats with grocery deliveries, these can be quick or scheduled deliveries of a shopping basket from your local store.

Uber really has two sets of customers: the users of the app, and the drivers providing the services. The second type is getting considerable attention as well in terms of product development. Now, the rider will see upfront how much he can make on a certain ride or delivery, and then can select the best one on offer. Personally I’ve noticed it takes longer to get your ride accepted since they’ve rolled this feature out, but Uber is saying it reduces the rates of drivers cancelling rides, which they see as the worst experience for consumers.

The CEO detailed their logic and R&D efforts in this area at the Morgan Stanley conference:

“Upfront fare was the number one feature that drivers were asking for, and upfront destination. They want to know where they are going. It makes all the sense in the world. It might be at the end of the day. So you might not want to have a drive to the airport. You might want to stick around to drives that are closer to home.

We were able to build a product that delivered upfront fare and destination to drivers, and what we got in exchange is the ability to price our supply better algorithmically. So previously in many markets, driver pricing was based on time and distance. And time and distance on most routes gets the pricing wrong. So a very easy example is if you land in San Francisco airport and you're getting a ride into the city versus getting a ride, let's say, into the suburbs or somewhere else where there won't be another ride after the drop off. If it's equal time and distance, those two rides were priced equally to the driver. The utility to the driver for the city ride is much higher, and therefore, that should go into the price. We should price the other ride at a premium, going out to suburbs, and we should price the city ride at a discount, with the total net price being the same.”

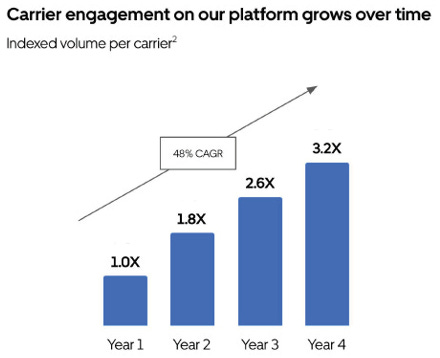

The freight marketplace

I have little background on the freight industry as this is a very fragmented, competitive market with low margins. Uber is building out a marketplace platform here so that companies (shippers) can book trucks to deliver goods to their warehouses, or from the warehouses to their retail stores or other distribution centers, such as for e-commerce. Reading through the presentation from the head of this business at Uber’s capital markets day, it did sound potentially like an interesting story for investors. I’ve inserted below the highlights:

“Nearly every participant in this vast ecosystem is struggling. 20 years ago, the average age of a truck driver in the US was 35, 10 years ago it was 45, it's now 55. It's the same baby boomers aging out of the industry. And the vast majority of those truck drivers are small mom and pop shops with less than 5 trucks. It's impossible for them to connect with the big shippers or run their operation efficiently.

So to aggregate that very long tail of supply, you have 17,000 brokers in the US, but they're all subscale and manual. It takes 25 manual steps to just coordinate and move a truck. So more than 10% of the cost of a truck is actually the cost of just coordinating it. Almost 30% of all the trucks that you see moving next to you on a highway are driving empty.

With the advent of mobile, we put an app in a pocket of more than 1 million truck drivers, creating the world's largest virtual fleet. With artificial intelligence, and data science, we're connecting the right truck for the right shipper. And with the cloud, we're making all of this accessible for tens of thousands of shippers, creating the largest logistics cloud ever built with $17 billion of freight under management.

With Uber Freight, carriers are now empowered to run their business on the go 24/7. And they are doing so while minimizing their empty miles between shipments so they can make more money. And they're paid for those shipments almost instantly, compared to an average of 45 days in this industry, while benefiting from access to discounts on fuel, maintenance, insurance and more.

One million drivers have on-boarded to the platform to date, which is more than a quarter of all truck drivers in the US. We now have critical supply density on every major freight corridor. So you have tens of thousands of shippers on one end trying to connect with millions of carriers on the other end. Looking at hundreds of different parameters in real time, we offer carriers a transparent price they can trust and shippers the peace of mind they know a price in advance.

We now serve more than 100 of the Fortune 500 shippers, 5 out of the top 5 beverages companies, 9 out of the top 10 consumer packaged goods companies, and we move on our trucks more than 15% of all bottled water in the US. Collectively, just these enterprise shippers alone represent more than $100 billion of freight opportunity. We continuously increased our engagement with them. For example, Anheuser-Busch is now planning their daily factory production volume based on a real-time price of a truck in the market, something only Uber Freight can do at scale.

And as we scale with those shippers, they are asking us not just to manage a portion of their freight but their entire supply chain. And to do that, last year, we've acquired Transplace, the leading managed transportation provider in North America. They're managing all of your carrier relationships. Their software is integrated across your entire operation from enterprise resource planning, to warehouse management, and more.

I wanted to end by sharing a bit more about the future. We believe autonomous trucks will fundamentally improve safety and reduce costs by injecting much needed capacity into this market. And we believe Uber Freight is going to play a critical role in this future. Like autonomous cars, autonomous trucks will start with the most predictable routes. In this case, long stretches of highway, leaving the more complicated last and first mile to human drivers. Late last year, we've announced our first pilot with Aurora, which is moving loads on self-driving trucks as we speak in Texas, between Dallas and Houston.”

Uber’s CEO gave an update on this business during the Q2 call:

“Uber Freight continued to be pressured by category-wide headwinds with industry spot rates seasonally weak - a trend we expect to continue in the near term. Despite the challenging environment, Uber Freight continues to expand its solutions to better support shippers throughout the entire freight lifecycle, as well as offer a steady and reliable partnership to shippers, who are increasingly turning to managed services to help navigate the ongoing market complexity. Uber Freight expanded its presence in Mexico in Q2 and scaled services to support different cross-border points as we have seen nearshoring to Mexico rapidly gaining traction.

While we continue to innovate, we do so with discipline. Rigorous cost management resulted in a $9 million quarter-on-quarter (QoQ) improvement in adjusted EBITDA and we took further action in July to reduce headcount. Looking past the near-term headwinds, we are confident that Freight’s technology, shipper platform, and marketplace flywheel will drive a long-term cost advantage and profitable growth over time.”

Data on container shipping rates confirm that the freight industry has seen a strong downturn (chart from Statista):

Also headlines from the Wall Street Journal clearly show how trucking has fallen victim to a market correction:

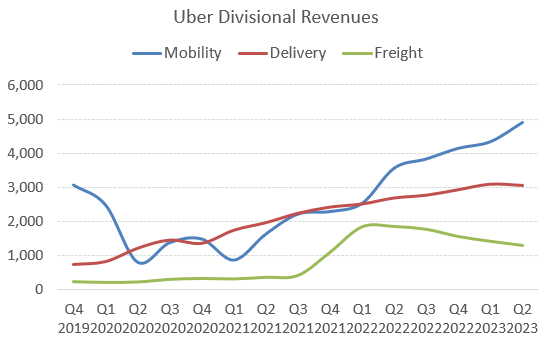

So this industry clearly has seen a cyclical downturn, which is also reflected in Uber Freight’s revenues. Although looking at the chart below, the correction seems to be much less steep here, which should be an indicator that the business is winning market share.

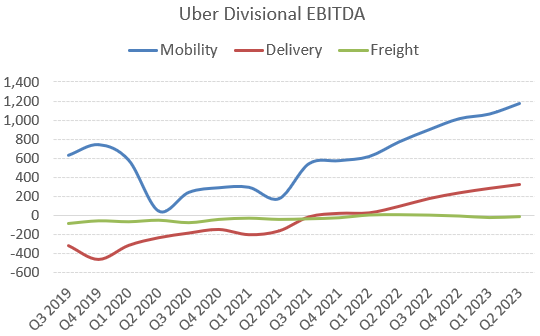

Another positive is that Freight isn’t burning much money, despite the current harsh market environment. So as the cycle normalizes over time, this should become actually an interesting earnings contributor.

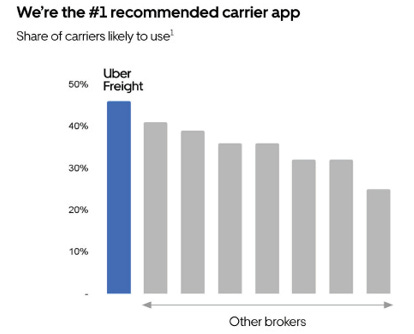

Overall, this does sound like a potentially interesting business over the long term with strong growth potential, strong network effects, and high barriers to entry. However, the current competitive environment looks to be more intense than in the duopolistic ride sharing business. Looking at the chart below, Uber lists already seven other platforms or brokers which seem to have a sizeable market share as well. Although on this data provided by the company, they are the largest already and I suspect that due to the network effects, this market will move towards a more consolidated state over time. This could easily become a 2 to 4 player market in the future. And as Uber Freight is already in the number one spot, they should be in a good position to take a large and perhaps dominant share of this market in the future.

Asking Bard about this market, he comments the following: “According to a 2021 report by FreightWaves, Uber Freight had a market share of approximately 10% in the US digital freight brokerage market. The top three players in the market were Uber Freight, Transfix, and Convoy, which together had a market share of approximately 30%. The remaining 70% of the market was shared by a variety of smaller players.”

Uber is commenting that they’re seeing strong engagement with their customers, which should be another indicator that they’re growing market share. From the 2022 capital markets day:

The business has signed up a wide variety of leading consumer brands as customers:

In summary, this is a potentially interesting business. Although it seems to be operating in a currently competitive environment, there are signs that the company is winning market share and they should be in a good position to continue this trend. Looking at Uber’s valuation, shareholders aren’t paying anything for this business at the moment so it is sort of a free call option where we could see over time both attractive top line and earnings growth coming from. On top of that, the freight industry looks to be cyclically depressed, and so as the cycle improves here over time, this should also provide another tailwind.

Autonomous driving

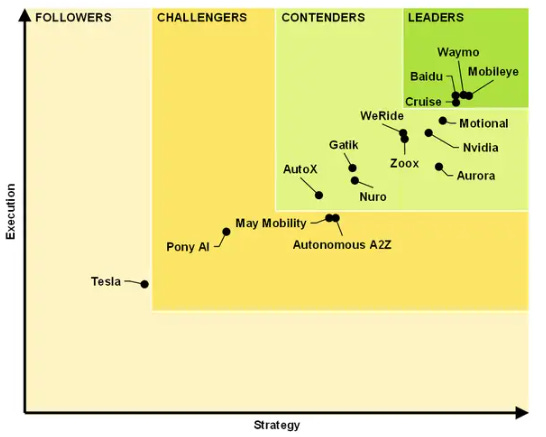

Long term the largest risk for Uber is probably autonomous driving. The biggest hurdle for any new competitor entering the ride sharing market is really signing up all the needed drivers. However, once fully robotic cars become a reality, a new competitor could more easily put cars on the road and start competing.

There are a number of players working on this technology, Guidehouse Insights rates Waymo (Google), MobilEye, Baidu, and Cruise (General Motors) to have the best capabilities. Additionally, I’m regularly seeing tweets, also from respected analysts, that they less and less have to intervene with Tesla’s Autopilot, often making long drives without any intervention.

The risk is also that one of these players successfully develops automotive AI capabilities, but won’t license the technology to Uber and instead start their own competing platform. This would put Uber on a strong competitive cost disadvantage, as the cost of the autonomous driving system should be far lower than having a driver operating a car for 8 to 10 hours a day. However, there are still a lot of mixed messages coming out of this industry and I suspect that full autonomy isn’t around the corner. I was told in 2018 that it was, and here we are five years later, with what seems to me only limited progress. Although both Waymo and Cruise did recently get approval to expand their services in San Francisco, and they’re slowly rolling out in more and more US cities.

Uber’s CEO commented on their strategy for autonomous rides: “In terms of autonomous vehicles, it's very, very early, and we are quite excited about the partnership with Waymo. We think they are best of breed in terms of their technical capabilities and their ambition to build in this business. It really is too soon to tell at this point what the economics are going to look like. We're quite focused on building out the product and really working with Waymo and our other autonomous partners to have essentially a routing layer between when demand comes into the network to be able to determine on a real-time basis whether or not we should route that demand to a person or to one of our autonomous partners, including Waymo or others, and Aurora in trucking, for example.”

Regulation

Regulation remains the other risk factor. Basically there’s the risk that Uber will be forced to employ drivers in certain geographies, as opposed to giving them the flexibility to be independent contractors as they are now. From Uber’s latest annual report:

“We believe that Drivers are independent contractors because, among other things, they can choose whether, when, and where to provide services on our platform, are free to provide services on our competitors’ platforms, and provide a vehicle to perform services on our platform.

If, as a result of legislation or judicial decisions, we are required to classify Drivers as employees, workers or quasi-employees where those statuses exist, we would incur significant additional expenses for compensating Drivers, including expenses associated with the application of wage and hour laws (including minimum wage, overtime, and meal and rest period requirements), employee benefits, social security contributions, taxes (direct and indirect), and potential penalties. Additionally, we may not have adequate Driver supply as Drivers may opt out of our platform given the loss of flexibility under an employment model, and we may not be able to hire a majority of the Drivers currently using our platform.”

Financials - share price at time of analysis is $44, ticker UBER on the New York Stock Exchange

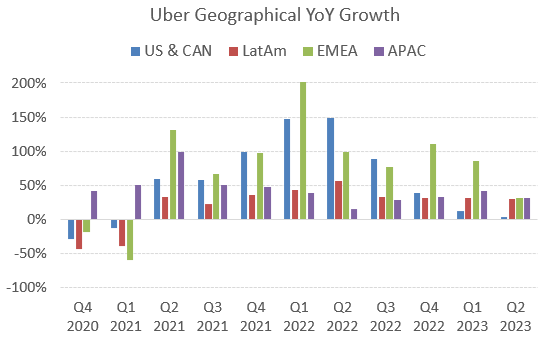

Uber’s growth is currently mostly coming from overseas (chart below). It will be wise to monitor whether that weaker growth rate currently coming from the US business is a temporary blip, or something more structural. But I suspect it’s largely related to the cyclical downturn in the Freight business which has been weighing on this geography.

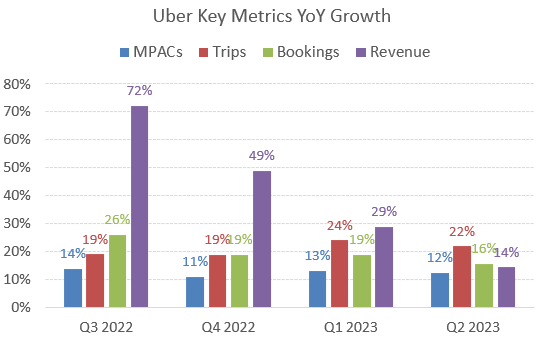

Overall, all key metrics are continuing to grow at double digit rates, as seen on the chart below. MPACs is basically an overly complicated abbreviation standing for monthly active users.

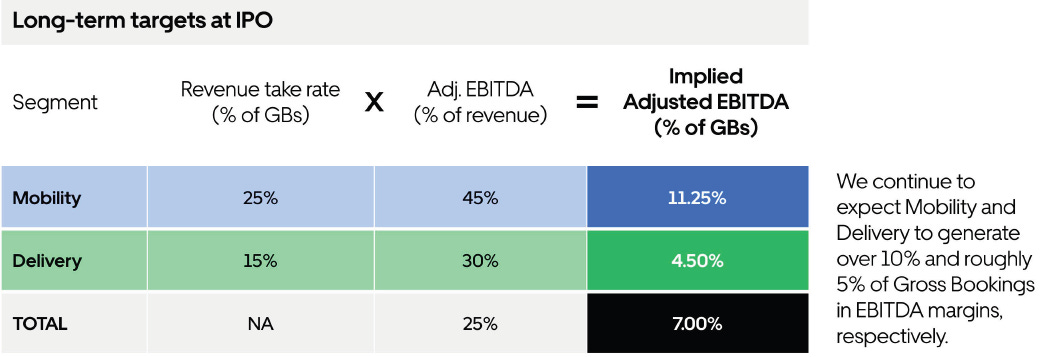

Long term, Uber is targeting around 45% EBITDA margins in Mobility and 30% in Delivery.

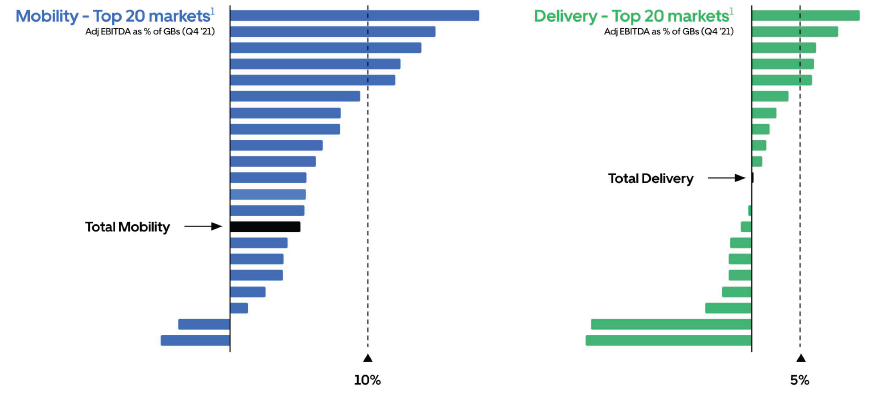

The company notes that in their key markets, they are already exceeding these profitability targets. In both Mobility and Delivery, the top five markets by EBITDA margins are well over their targeted margin. Obviously the company is burning cash in a few markets, and if these would fail to scale properly, these could easily be divested or wound down, which will lift the group margin.

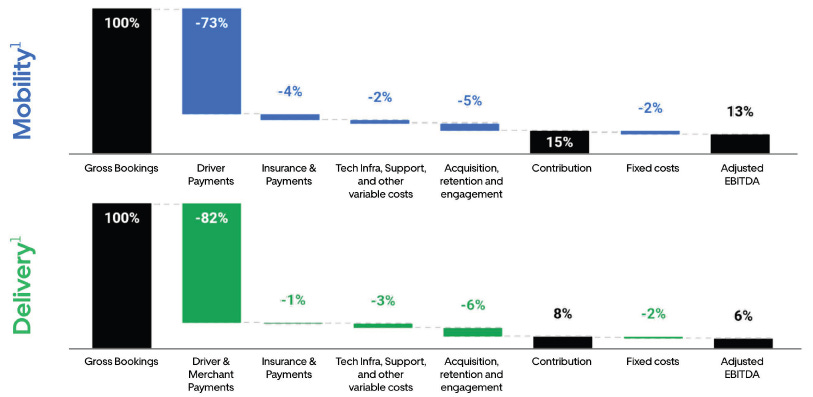

Below Uber illustrates how they get to a 13% EBITDA margin compared to Bookings in one of their most profitable markets. And they show the same exercise for Delivery:

At the currently reported take rates for Mobility and Delivery of 29% and 20% respectively, this would work out to 45% and 30% EBITDA margins on revenues for those businesses respectively:

Uber’s CEO commented on their margin expansion during the Q2 call: “It's really simple, we are levering our fixed cost base. As you know, we're really focused hard on both containing our fixed cost, getting leverage on all the variable cost items, including insurance, and then what we're doing is we are seeing some adoption of some really good new products. So what that really results in is margin expansion.”

He shared some further insights at the Morgan Stanley conference: “Our tech teams have delivered very significant algorithmic improvements that have resulted in the cost per transaction for delivery coming down substantially. We talked about cost per transaction last quarter improving 20% on a year-on-year basis.”

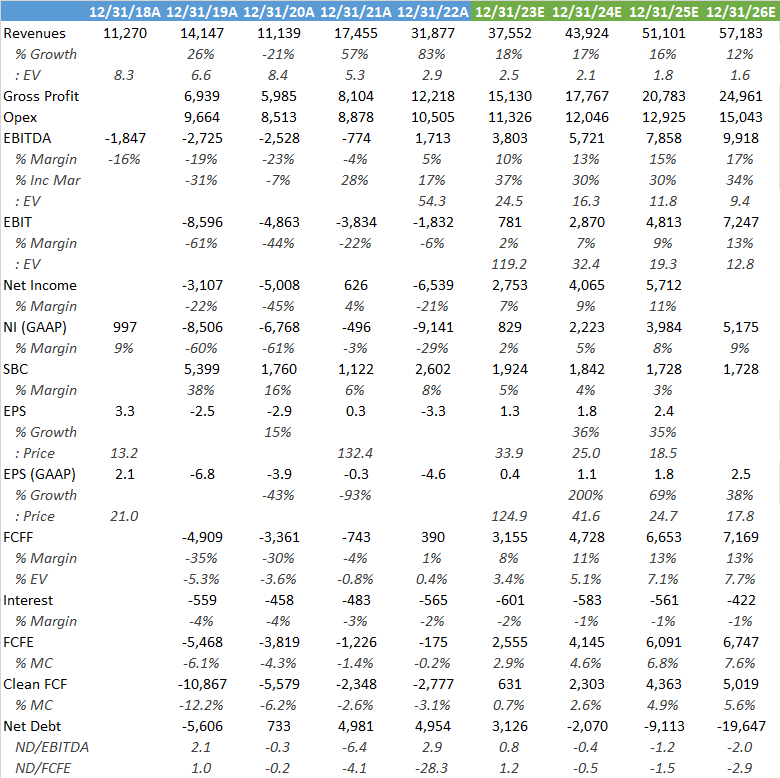

Looking at the sell side’s numbers, if I put 2026 EBITDA numbers on a reasonable 15x NTM EBITDA, I get to an IRR of 17% from now till the end of 2025, also taking into account the possibility of share buybacks from the Clean FCF metric.

A target multiple of 15x NTM EBITDA would be a similar multiple as for Booking Holdings, which operates the popular booking.com app for the supply of hotel accommodations.

Uber has become oriented towards returning cash to shareholders as well, Uber’s CEO commented recently on this: “As we have previously discussed, we are focused on achieving investment-grade credit ratings over the coming years. Our commitment should provide investors comfort that we will methodically continue to scale profitability through the coming years, while being disciplined on capital allocation. This means that we will have a high bar for any M&A opportunities, and our organic growth efforts will have a critical focus on unit economics as we continue to scale globally. Over the next few quarters, we will evaluate returning excess capital to shareholders as our cash flows ramp, and with any potential further monetization of our equity stakes over the long term.”

If you enjoy research like this, hit the like button and subscribe. Also, share a link to this post on social media or with colleagues with a positive comment, it will help the publication to grow.

I’m also regularly discussing technology investments on my Twitter.

Disclaimer - This article is not advice to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it cannot be guaranteed that all information used is of such nature. The views expressed in this article may change over time without giving notice. The mentioned securities’ future performances remain uncertain, with both upside as well as downside scenarios possible.

Great article as always! It's funny because I was listening to Ben and David (of Acquired Podcast) interviewing Dara, worth a listen.