The Rare Earth Bottleneck

A tour of the space

Rare earth elements (REEs), despite their name, are relatively common elements within the earth’s crust. However, extraction becomes only economical when you have rich ore deposits. REEs’ unique magnetic, electrochemical, and luminescent properties make them irreplaceable across a wide range of modern tech. For example, robotics, modern military hardware, green tech such as EVs and wind turbines, high-tech electronics and computing, are completely dependent on them.

While there are many end products that make use of rare earths, permanent magnets are overwhelmingly the key application driving the current geopolitical rush. According to International Energy Agency (IEA) data, permanent magnets account for roughly 95% of the monetary value of global rare earth consumption. The key REEs for magnets are neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb). These four are also called the ‘magnet rare earths’.

")

A neodymium-based magnet is the strongest type of permanent magnet available on Earth. However, when you mine rare earths, you have to dig up all elements together. This creates a massive market imbalance—elements such as cerium and lanthanum make up the vast majority of what is physically dug out of the ground. Because these are in oversupply, they are very cheap and often trade for just a few dollars per kilogram. These low value REEs dominate volumes for low tech applications such as catalysts, glass, and polishing powders.

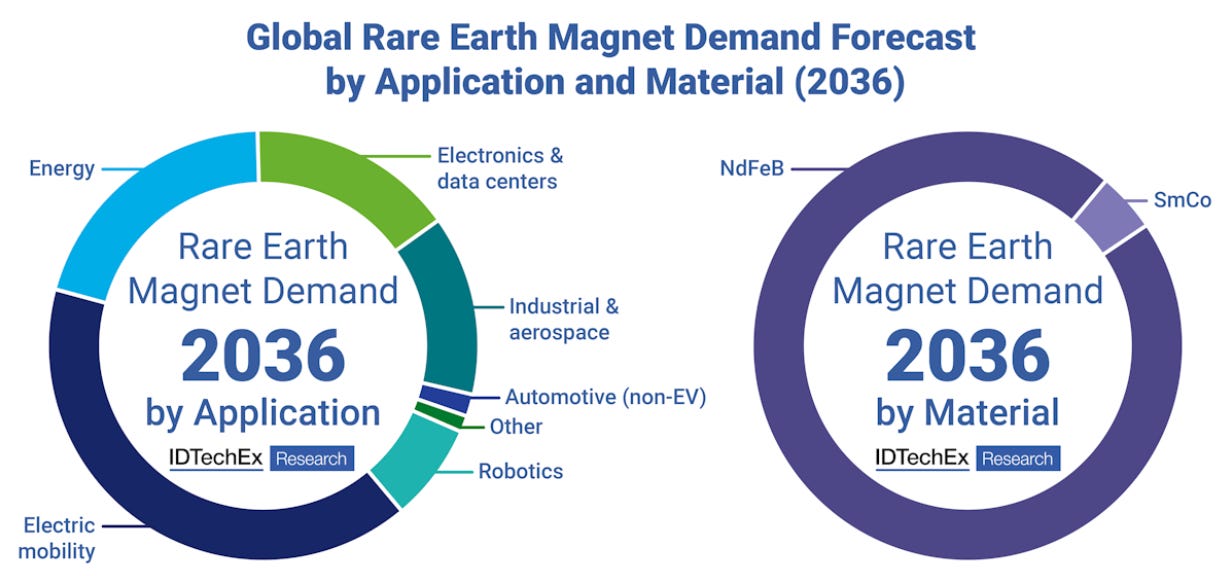

Pure neodymium is a soft, silvery-grey metal. On its own, pure neodymium is not a useful magnet. NdFeB (Neodymium-Iron-Boron) is the specific alloy created by combining neodymium with iron and boron. This combination locks electrons into a specific structure with high magnetic energy. As a result, geopolitically crucial end markets such as robotics, aerospace, electronics, data centers, and EVs will be dependent on NdFeB magnets:

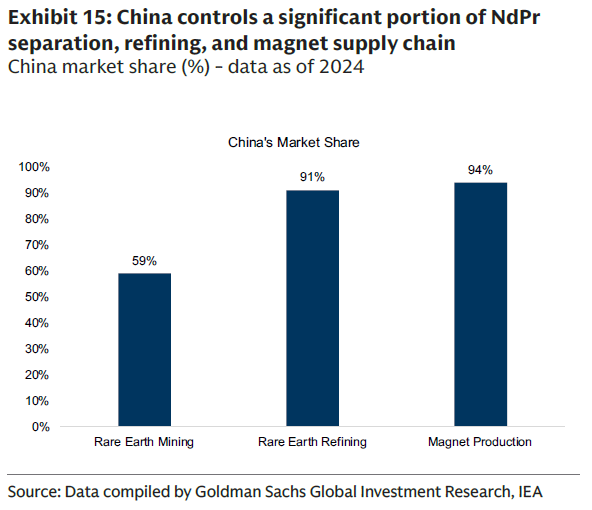

The big problem, however, is that up until recently, all rare earth refining was done in China. For example, in 2024, the US accounted for 16% of global rare earth production, however, these rare earths were then shipped to China for refining and magnet production. Needless to say, this gives China strong leverage over the US as they can halt, for example, manufacturing of US military equipment, and also block new advanced industries such as humanoid and industrial robotics from scaling up.

Goldman shows how China in 2024 had a 59% market share in rare earth mining, but an over 90% market share in both rare earth refining and magnet production:

Goldman estimates that NdFeB magnet demand could easily triple in the coming ten years. There is clear upside to this estimate if new industries such as robotics, edge AI, AI compute in space, and EVs take off. Due to environmental and other regulatory hurdles, limited access to high-grade deposits, high capital costs, and long lead times, it’s likely that there will only be a few players in the West that can provide rare earth mining, refining, and magnet production—i.e. fully vertically integrated mine-to-magnet operators.

As Western governments and big tech players such as Apple are now willing to pay premiums for non-China sourced magnets, and sign long term supply contracts, we see the long term outlook as attractive in this space. This is becoming less of a commodity market, and more of a high growth market with floor pricing guaranteeing attractive margins.

Next, we’ll go through key assets in the magnets and rare earths value chain, and we’ll review the key players involved. We’ll also discuss future TAMs, profitability, and potential returns.