Tech Stocks – Investment Ideas & Trades 24-Aug-2025

Q2 Earnings Season

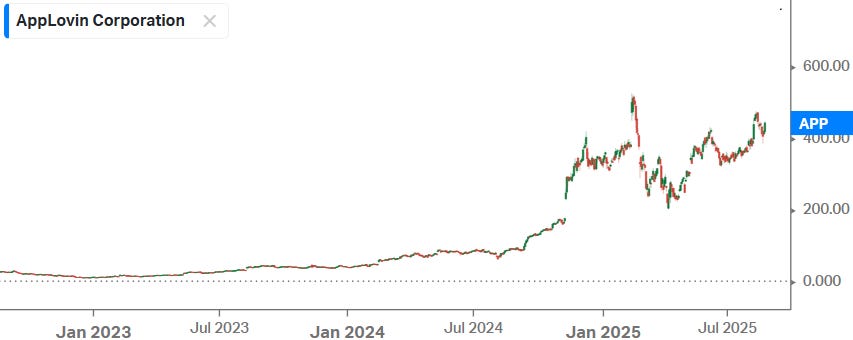

Applovin’s share price performance has been off the charts over the last two years as they massively improved ad targeting in their mediation platform which reaches 1.5 billion devices. Basically, mobile gamers have to watch ads during the games they play and these can’t be skipped, which creates a captive audience unlike with most other social media where you can quickly scroll past the ad. Obviously, this is very powerful and Applovin is now opening up their ad network to e-commerce companies so that gamers around the globe can be targeted with goods they’re interested in to purchase online. This has further accelerated revenue growth over the last year and e-commerce is now contributing already 10% to their ad network revenues.

A potential headwind is that Applovin’s platform is still somewhat immature with growing pains, so they’ve only been gradually opening to a select number of larger e-commerce retailers. Crocs is one of those retailers who has been increasing spend on the platform, however, as they kept increasing spend, they noticed that the return-on-ad-spend (ROAS) noticeably started to drop below that of Meta and Google. This is via a recent Tegus interview:

“It was eye opening and a really good learning for us to increase the budgets and understand the point of diminishing returns. For us, as we flex to that higher spend, it wasn't as effective. We weren't able to hold that same level of return that we were comfortable with and really scale in a profitable way. That led us to peel back to the previous lower spend levels that had proven to be effective. Applovin's team is actually digging in to understand what it is about our brand, product or creative that isn't seeing the same results that they've claimed to have seen with other clients when they scale to a higher level of daily investment. We will flex our spend at given times once we have more conclusions or a path forward of what we should try next. We want to continue to do a little bit more testing with AppLovin. It's valuable real estate from an advertising perspective, showing up on mobile where consumers are spending their time. I think there's more that we can be doing on the creative side. Also, I think that AppLovin needs to continue to develop their offering and provide greater visibility and controls into the inventory, if they can do that, I think there's opportunity for us to invest more and scale.”

Although there are a number of interviews on Tegus where larger e-commerce players are reducing their levels of investment, we actually remain positive on Applovin both in the near and the long term. The reason is that Applovin has only been gradually opening up their ad network to a more select number of larger retailers, whereas there is still a wave of especially small and middle-sized retailers that can be onboarded. SMBs are big ad spenders on Meta and Google, and as also further big retailers can be introduced to the platform, we suspect that Applovin has only been scratching the surface of the ad spend they can attract to their platform. These are the highlights from the CEO’s comments on the recent call, clearly indicating a strong growth opportunity ahead:

“Q2 2025 was another great quarter, driven by continued strength in gaming advertising. Our growth comes from improved technology, increased demand as well as from supply side expansion. The MAX marketplace creates the supply that drives our growth as well as the growth in the market. As marketing technologies in the industry continue improving, we expect the supply will keep growing quickly. While we don't disclose exact MAX marketplace growth rates, it has consistently been double digits, far outpacing growth in the in-app purchasing gaming market. The ongoing improvement in our models drive sustainable growth rates beyond the market growth rates, while we continue to expand our dominant leadership position. Based on all the opportunity in front of us in our core market, we are confident we can sustain 20% to 30% year-over-year growth driven by just gaming. However, what gets us more excited now than ever in our history before is the opportunity to really expand outside our core market.

Recently, we took the first step towards opening up our platform broadly, quietly launching our new AXON ads manager, our self-service portal, which will serve as the foundation for our next decade of growth. Our ads manager has many benefits. It puts day-to-day controls directly in advertisers' hands, reducing friction. It enables credit card billing, eliminating the hassle of monthly invoicing. It provides the architecture for agents that can eventually automate every workflow. It establishes the framework for automatically generating ads. It simplifies onboarding through our recently launched Shopify app. It deepens integrations with attribution providers, giving customers more accurate reporting. With the rollout going smoothly, we are ready to widen access. On October 1, 2025, we plan to open the AXON ads manager on a referral basis, perfectly timed for the holiday season. Feedback from these partners will guide our global public launch in the first half of 2026. To date, web advertising campaigns have been limited to the United States. On October 1, we plan to open our platform to most major international markets.

Now stepping back, we have spent the last decade assembling the pieces, reach more than 1 billion users, best-in-class optimization and now a self-service interface. Together, they position us to help any business, of any size, and anywhere in the world grow profitably. The opportunity is so big that we will be launching the platform under its own brand, AXON. Once AXON is fully open next year, we plan to begin paid marketing to recruit new advertisers, which will drive predictable compounding growth.

Obviously, we have very small penetration in terms of advertiser base against global advertisers count. And the way we look at our business is if the model works this well at this small amount of penetration, what happens when we can really open it up and go service all the small businesses in the world. Our aspirations are to help any business of any size be able to acquire customers profitably.

In Q4 last year, we saw a huge ramp-up in the e-commerce category when we went into this pilot phase, and recruited hundreds of advertisers that we disclosed. Now the reason is that new customers that come into our platform are extremely incremental to our business. Since then, we knew that we had to go build a whole bunch of things into the platform to be able to service advertisers at the level that we like to do. And we set a really high bar for the products we deliver. We wanted to build the ads manager, which we released and will continue to innovate and iterate through. We wanted to build dynamic product ads that came out in the last couple of quarters. We wanted to do better integrations with attribution companies, which happened inside this quarter. And we want to launch a Shopify app and other apps that allow for seamless integration amongst the advertiser base.

So, we ended up constraining the advertiser onboarding process for a couple of quarters while we made sure that the product was at the level that we wanted to get it to. Now, in Q4, we're looking at a referral-based opening. Accounts on the platform, they obviously like our solutions because they're spending substantial amounts of money on our platform. They'll get the chance to refer others onto our platform and have them go live in a self-service way. We expect that will increase the advertiser count quite quickly and it will also allow us to go through live examples of advertisers coming in self-service and all the way to scale on our product. Assuming all that goes well, we will open up the platform entirely to the world in the first half of next year. We think as advertiser count grows, especially in categories outside of gaming, you're going to see a lot of upside in the numbers that we're able to report.

Now, we've been focused on growing the cohort that's live. The growth from the cohort that's live, the majority of our growth came from gaming. Gaming is still a 30% to 40% grower for us. Now e-commerce, you're also going to have new onboarding happening for the first time in our history at a rate that's much higher than we will have ever seen before. So we fully expect that e-commerce will see a pretty substantial ramp-up through that, what you can call a soft launch period and then as we go into a broader global release. And then the last point to remember is the fact that we have constrained the advertisers we even have live today by not allowing them to buy our audience that's international. The vast majority of our user audience is outside the U.S. We will be releasing almost all markets once we go into this October 1 release.”

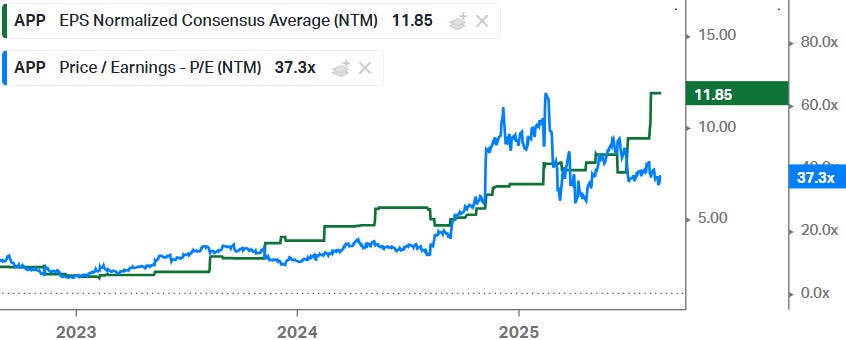

Looking at current valuation, 37x forward EPS is pretty accommodative for a company that should be looking at a long runway of growth. Obviously, it’s not on a 15x PE anymore like at the start of ‘24 when we first recommended these shares – the market has now caught up that this is a well positioned company exposed to high growth rates – however, even with shares having gone up tenfold since then, we continue to happily hold a position in this name.

Thus, we continue to see share price sell offs as temporary and that the trajectory of the share price in the coming years will remain in the upwards direction.

William Blair went to Austin to compare Tesla robotaxi and Google Waymo:

“Tesla vs. Waymo. In Austin we took multiple robotaxi and Waymo rides; the contrast was clear. Aside from the visual difference between each pulling up to the curb, the robotaxi was comfortable and familiar, and it felt as though a friendly ghost chauffeur was driving our personal car. Driving was smooth and human-like, recognizing and patiently waiting for pedestrians, switching into less crowded lanes, patiently waiting to execute a safe unprotected turn, and yet, discerning and confident enough to drive through a light that just turned yellow, so as not to slam on the brakes. Waymo also provided a top-notch service and we did not encounter any safety concerns, but if we were to be overly critical, if felt more ... robotic. In the cabin you have to listen to an airline-esque preamble on Waymo and safety protocols, and during the ride you can hear all the various spinning lidar sensors spooling up and down with electronic whizzing sounds. In short, robotaxi felt like a more luxurious service for half the cost and the driving felt more human-like.

Robotaxi pricing was consistently half that of Uber, confirming our thesis that Tesla could win market share by leveraging its lower cost structure. We estimate Tesla’s autonomous tech stack is one-tenth the cost of Waymo, with significant manufacturing scale and cost optimization multiple years ahead. In our robotaxi model, we forecast Tesla to continue to undercut price by 50% and achieve the target of $0.30 cost per mile in the 2030s as the dedicated robotaxi vehicle scales.

Tesla has the ability to leverage its lower cost structure and weaponize pricing—charging 50% less per mile, it can still achieve near 60% EBITDA margins. We expect Tesla to win 35% market share versus competitors Waymo at 15%, Uber at 38%, and Lyft at 13%, generating almost $250 billion in revenue in 2040. After discounting the robotaxi EBITDA of $145 billion at 8.5% discount rate, we estimate an implied value of Tesla’s robotaxi business at $298.61 per share, energy business at $30.73 per share, and auto business at $28.09 per share, totaling an implied fair value of $357.43 per share.”

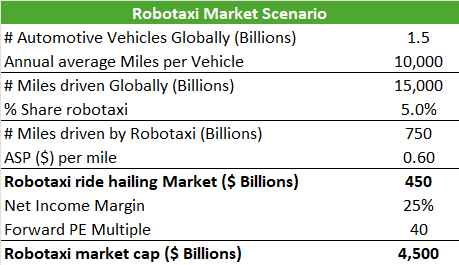

Tesla is working on two huge opportunities – humanoid robotics and robotaxis. We think that the first is by far the largest opportunity, however, robotaxis are a compelling opportunity as well. For example, a robotaxi company that could capture 5% of the global number of miles driven at a price of $0.6 per mile could already result in a $4.5 trillion market cap:

For premium subscribers, we will discuss six more investment ideas – including smaller tech names that are unknown to many investors, like Applovin was at the start of ‘24, and we will also give insights on better known tech names that are seeing high levels growth.