Ansys' strengths in semiconductor simulation

Ansys has a variety of software simulation tools used in the design of semiconductors with its RedHawk platform now integrating most of these. Semiconductor design utilizes a chain of software tools, each focused on a particular task. The three companies that dominate this industry are Cadence, Synopsys and Mentor Graphics (Siemens), while Ansys is the strong player in the overall simulation market. Around 30% of Ansys’ revenues are now coming from the semiconductor end-market (chart below), while the company’s other two large revenue exposures, and more traditional end-markets, are aerospace & defense and automotive:

Ansys is widely known for its physics-based simulation tools, such as fluid dynamics and structural analysis. The company has much more capabilities than the three shown below, but it should give a feel of what their software can do.

These tools are used by PhDs and advanced engineers, both of which have been trained for years on the tools, making revenues extremely sticky.

The company’s CEO explaining the business of simulation at the Barclays conference:

“So Ansys is an engineering simulation software company. And what that means is we build software that allows our customers to be able to analyze and evaluate the behavior of a physical product, completely in the virtual domain. Using our technology, our customers can visualize the behavior, the failure potentials, the response of any product that they’re trying to design completely in the computer without the need for physical prototype and without need for experimentation. The way we do this is our software really encompasses the basics and the fundamentals of mathematics, of physics, of computer science.

It’s the accuracy of the simulation that is really important because you’re using simulation as a way of evaluating a physical phenomenon. And you have two possibilities. You can rely on a physical experimentation, i.e. you could build a prototype and then physically evaluate it in the lab. So if you were testing the safety of a car, you could build a model of the car and you could slam it against the wall at 30 miles an hour, and that will give you some perspective. Or you could do that in software. The price differential is significant. Building a physical prototype in advance of the production model of a car can be quite expensive. And then slamming it into the wall requires a significant amount of instrumentation. That’s very expensive, maybe $1 million to do a single crash test. And that gives you one scenario, a head-on collision at 30 miles an hour for example. But if you could do that in software, you can do that with significantly less cost. You can run multiple experimentations and you can do so really early in the design process before you lockdown any of the decisions. So there’s real advantage to doing it in software, but it only works if the software is accurate and we certainly pride ourselves at being very accurate across our simulation capabilities.

The other thing that I’m really proud about is the completeness of the portfolio. The problems that our customers are dealing with are not tied to a single individual physics. These are not uniquely structural, fluid dynamics or electromagnetics problems. This is really the integration of all of these, that’s what we refer to as multi-physics problems. So if you take the example of a car crash, you might imagine that it is a structural analysis i.e. you’re trying to analyze the physical integrity of the car to see if the driver would be safe. But the reality is it’s a multi-physics analysis because you’re simultaneously analyzing the deployment of the airbag and that’s a fluid dynamics problem.

We’ve got representation across structures, fluids and electromagnetics in the semiconductor space; also optics, safety analysis, embedded software and I could go on.

We moved our portfolio from being tool-oriented towards more of a platform-oriented view. So while we have a lot of simulation capabilities as individual tools and customers can use them, we have also integrated this together as part of a platform. So that evolution has put us in a very strong position to deal with these emerging use cases that customers have.

If you look at aerospace, the trends there are towards sustainability. So moving away from traditional fuel to sustainable fuels, electrification, hydrogen, thinking about VTOL aircraft. They’re making design decisions now that are going to stay with them for the next 25 years. And to facilitate this transformation requires multi-physics analysis.”

Ansys is the top player in the simulation space, with an estimated market share of above 25%. Competitors include Altair Engineering, but also the CAD software providers such as Dassault Systemes, Autodesk, Siemens, Cadence and Synopsys among others. Designed models can be uploaded from the CAD software into Ansys’ tools, to analyze and simulate them under a variety of physical conditions.

According to Ansys, the global annual market for product failure avoidance is $750 billion, while $8 billion is spend on simulation. Obviously not all product tests can be digitally simulated, but it does suggest large room for growth, especially as the physical world can get better modelled in the digital world over time. In the future, it is conceivable that at some stage we’ll have good digital models of a human cell and the human body as a whole, which would allow new drug molecules to be initially tested digitally.

Another reason for this low penetration of simulation tools in the failure avoidance market is that Ansys’ software is typically used by PhDs and other advanced engineers, but the company has been working on making their tools more user-friendly so that they can be used by a wider range of people. Ansys’ CEO discussed at the JP Morgan conference for example how they’ve been integrating their simulation engines into software from other providers:

“At our last investor day, we talked about how there’s a company that’s providing software to eye surgeons. And under the covers, unbeknown to the physician because the physician really has no interest in learning how to use simulation software, the technology is taking advantage of simulation and presenting the results to the surgeon. So the what-if analysis that the surgeon would normally go through based on their experience, they can actually use physics-based analysis to drive them towards the best surgical outcome. That’s an example of a next-generation use case where simulation is embedded, and that goes well beyond anything that we have done in the past.”

The CFO continued:

“If you’d like to see the data, the core simulation market is about $8 billion, and our estimates are that over the next 10 years, that core market could roughly double. The emerging use cases that Ajei just referred to in terms of contextually embedding simulation for non-experts, our estimations are that if that would continue to progress over the next decade, that doubling could nearly triple.”

So the company is guiding here that their market could double to nearly triple over the next decade:

One really interesting feature of Ansys’ business model is that revenues not only grow with the number of software seats and modules being sold, but also how much computation the clients’ workloads need. This is very similar to Synopsys and Cadence, where they are working out new pricing models as their CAD software is being used for compute intensive AI workloads, such as generative AI in semi design.

Ansys’ CEO detailing their business model and the computational nature of their software:

“In our case with simulation, a single engineer could kick off a job that could run for across thousands of cores and for days or weeks at a time because you’re solving these incredibly large problems. And a single engineer could kick off a number of different jobs. So many of our customers have invested in datacenter technology to try to build out compute capability. And in fact, this is a dimension of growth for us, which separates us from traditional enterprise companies because when they sell software, they can grow by selling to more users or more products. We can sell more users and more products, but we can also sell more computation. We sell a license to be able to use our software across more hardware, so that’s a really interesting avenue of growth. With our cloud strategy, we also support them to use our technology in the cloud for scale-out compute. We work with Microsoft Azure and Amazon AWS.”

During the 2000s, Ansys acquired a range of software tools focused on semiconductor simulation, below we’ll go through the most important ones.

PathFinder simulates the effects of electrostatic discharge (ESD) on a designed IC (integrated circuit). ESD occurs when there is a sudden buildup and release of static electricity, which can damage and destroy electronic components. PathFinder analyzes the physical layout of an IC and its underlying circuitry to identify potential weaknesses. The software can simulate different types of ESD events to help designers understand how their designed ICs will perform under real-world conditions. The software can help in optimizing the placement and sizing of ESD protection devices, improving the robustness of the IC. The software is both available in the cloud and on-premise.

RaptorH is an electromagnetic (EM) simulation software for ICs. Early analysis helps pinpoint issues, minimizing later debugging and accelerating overall development. The company has a similar software for analyzing superconductive processors called RaptorQu, enabling the design of tens to hundreds of qubits (the ‘transistor’ in a quantum processor which can have four states).

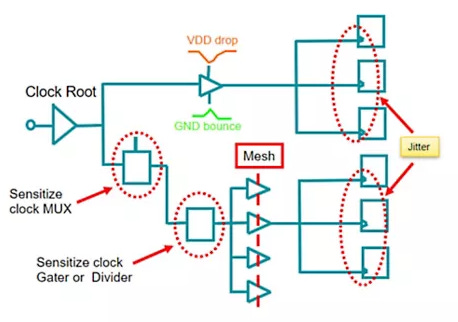

Clock FX simulates all clock paths in an IC design and identifies contributors to jitter. The clock path is the network of wires and buffers that distributes the clock signal throughout a chip, and must reach all parts of the chip with minimal delay and skew.

Most of these tools have now been integrated into the RedHawk multi-physics platform, which can also analyze voltage drop, electromigration, heat dissipation and signal integrity for chips, multi-die packages, interconnects, and printed circuit boards (PCBs). The platform is also delivered over the cloud.

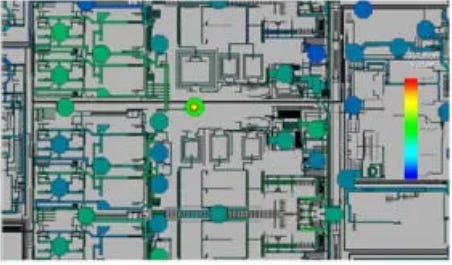

A detailed thermal analysis of a PCB with RedHawk — pretty cool software:

Ansys’ CEO discussed the trends in semiconductor simulation:

“When you’re considering a traditional system on chip (SoC) and IC analysis, you use your more traditional tools. But the moment you’re now considering a 3D-IC structure, you have to worry about the integration and the interaction between the different layers. So you’re thinking about electromagnetic interference, signal integrity, and other kinds of analysis. And that requires physics-based analysis, which is where we come in. We have customers like Nvidia for example, they’re taking advantage of our technologies to pursue the physical design limits as they start to use RedHawk, Raptor, all of our products to improve their design.”

An example of a 3D-IC with HBM DRAM dies stacked on top of a base die, connected by through-silicon-vias (TSVs). These are the types of modules you can create with the latest advanced packaging techniques such as SOIC and CoWoS.

- TSMC - WikiChip")

This semiconductor software portfolio has been built up both by acquisition and internal R&D, Ansys’ CEO detailed their strategy here:

“Ansys started of as a structures company, and for many years was essentially growing organically. If you look at our expansion into the second major physics area which was fluids, it was driven by two acquisitions, one in 2002 and one in 2004. Then subsequently, we’ve done over a dozen acquisitions in the fluids space. It’s been a combination of both organic investment as well as inorganic activity. So that’s a great example where we’ve got really good capability, electronics as well.

What I would point to recently is optics. A few years ago, we didn’t really have an optics presence, and we identified autonomy as an area where there was going to be growth, and we didn’t have support for camera and lidar. And so we looked around for an appropriate partner and then eventually decided to acquire a company called Optis. This was in 2018 and that obviously went well. And then from there, we used that as an anchor to build out a couple of other optics capabilities. We acquired a company called Lumerical which gave us photonics capabilities, and we acquired Zemax which gave us lens design.

But more than just simply the acquisitions, we’ve organically invested in them and integrated them together to have an integrated optics offering, and that’s typically what we do. It’s not just simply a matter of doing an acquisition and letting it live separately from the rest of the business. It’s doing acquisitions, integrating them together because ultimately, customers are not looking for point solutions. They’re looking for an integrated offering across multiple physics, and that’s what we try to do with our offering.”

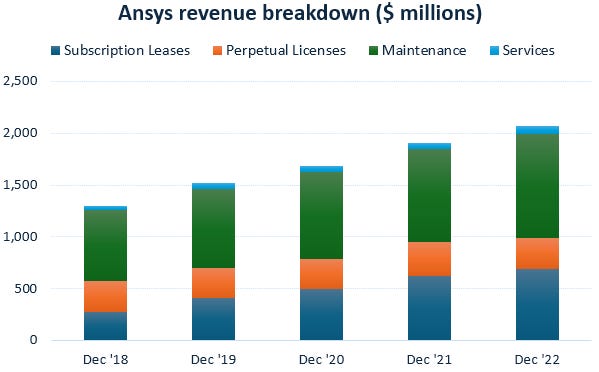

The company’s revenue breakdown shows how revenues are now largely recurring, i.e. flowing from subscription leases and maintenance fees. Old-style, one-off perpetual licenses are only 15% of revenues now and have been declining in the mix — I suspect Synopsys will try to move away from this business model entirely, transitioning customers to more attractive, annually recurring subscriptions.

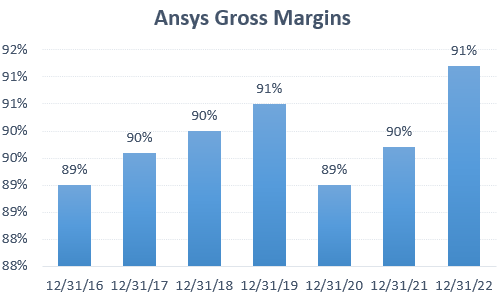

Ansys makes attractive gross margins of above 90%:

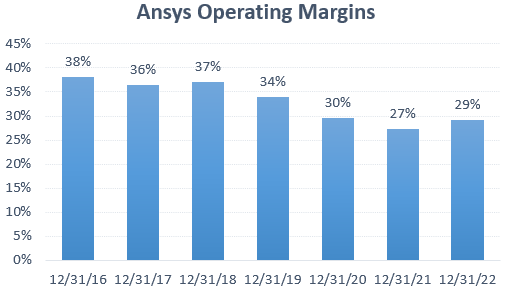

However, operating margins have been sliding:

Ansys’ CFO discussing the outlook for their operating margins at JP Morgan:

“We were kind of in the low to mid-single-digit growing category with very high margins, and the intention was to make deliberate investments to accelerate growth. So if you look back 5 years up until about 2021, you would have seen that margin investment in the business. And if you look at our outlook, the guidance that we gave at our investor day was that we see significant operating leverage in the business through our cumulative unlevered operating cash flow guidance of $3 billion from 2022 to 2025, that compares to approximately $2 billion over a comparable period prior. Underwriting that is the 12% CAGR of ACV (annual contract value) growth that we guided to over that time period and operating expenses growing at a relatively slower pace than that ACV.”

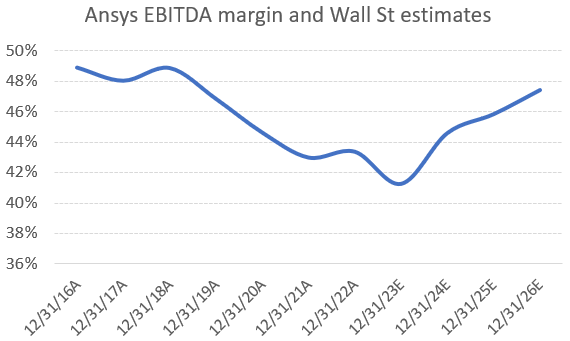

If investment can now gradually be reduced relative to top line growth, this will allow for margin expansion going forward. Wall Street does look very bullish on this story:

For premium subscribers, we’ll go further into:

Synopsys’ business

The potential roadblocks to the Synopsys - Ansys deal

A detailed analysis of the merger

A financial model of the Synopsys - Ansys combination with thoughts on valuation for both names