SpaceX - Frontier AI, Starlink, Terafab, Launch, Colossus

Pre-IPO Deep Dive

The SpaceX Vertically Integrated Platform

SpaceX has three key businesses—Launch, Starlink, and AI. In the first two, the company currently enjoys a near monopoly-like positioning. For example, over the past few years, SpaceX has launched more than 80% of mass to orbit. The mission success rate for its rockets is over 99%. Additionally, Starlink is the only high-speed internet and mobile provider that’s available to consumers from space, making it available anywhere you are—on a boat, in a plane, hiking in the mountains, etc. This business is already printing cash while still growing at hyperfast rates. Finally, in AI, the company is one of the frontier AI model providers with Grok and soon Cursor (which will likely be fully acquired post IPO), with the xAI business setting records to bring up new data center capacity with its Colossus data centers.

Normally, a company would do one of these activities well—e.g. being a neocloud, training a frontier AI model, being a space launch provider, or running the world’s largest fleet of satellites. A key reason is that founder Elon Musk has been able to attract some of the best engineering talent to work at his companies over the last decade(s), as here engineers can work on the hardest set of problems—rockets, space, etc. This allows SpaceX to run a vertically integrated platform—designing and manufacturing its own rockets, satellites, engines, avionics, writing a lot of its own software, and even making the tools to build all these parts. This extreme level of vertical integration gives the company a platform to innovate rapidly and continuously drive the cost down.

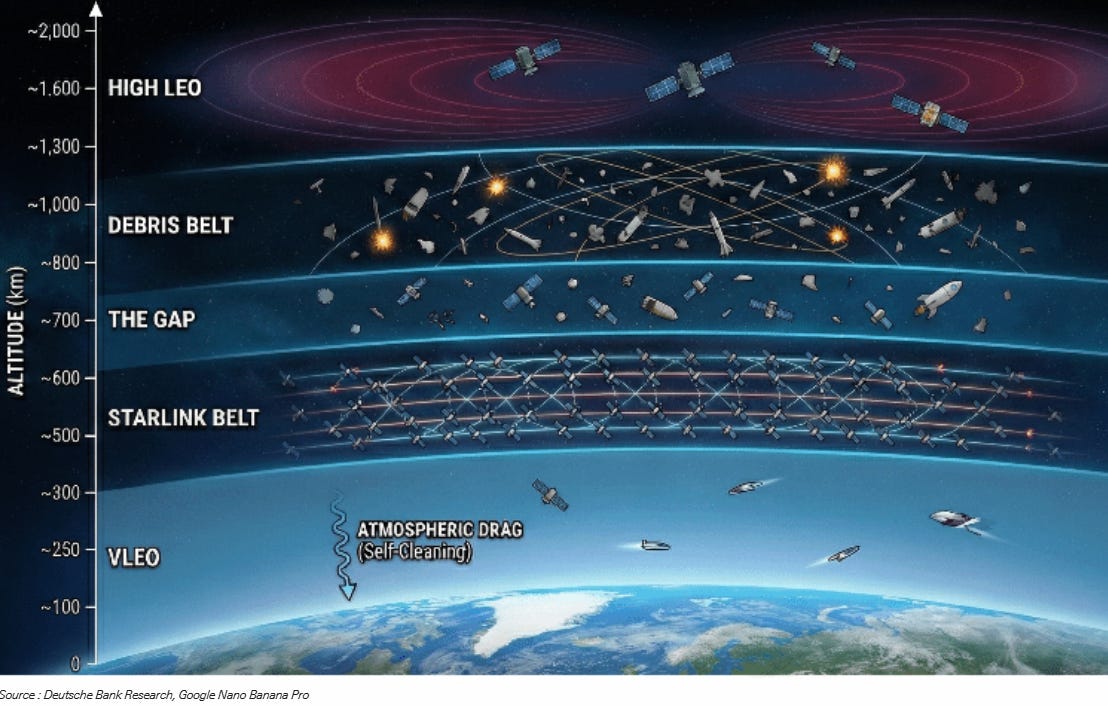

Basically, the company has built a platform to enable new economies in space, with Starlink being the first of these. Due to SpaceX’s manufacturing and launch capabilities, the company was able to put by far the biggest satellite constellation in Earth’s orbit. Its more than 10,000 satellites currently make up close to 70% of all active satellites orbiting Earth. And this number can be increased up to 42,000. Deutsche Bank illustrates the “Starlink belt”:

Another growth angle is that SpaceX is currently transforming into a vertically integrated AI company as well. The goal is to manufacture its own GPUs, CPUs, and Memory in jointly operated fabs with Intel, the ‘Terafab’ project. It looks like Intel will bring in the IP and knowhow of 14A manufacturing, and then SpaceX and Tesla will bring in the capital and new engineering talent to scale up these fabs, with an aim to innovate rapidly on chip design and manufacturing. Also the tool makers such as ASML, Applied Materials, Lam Research, etc., as well as research houses in advanced semi technologies such as Imec can bring in substantial know-how. From the SpaceX prospectus:

“Our strategy for Terafab is to vertically integrate across the design of lithography masks, fabrication of logic and memory chips, and design of advanced packaging in a single closed-loop plant. Conducting all these activities end-to-end in a single facility enables rapid testing and iterations, allowing us to improve chip design and scale manufacturing faster. We expect that our speed and cost advantage from vertical integration will allow us to scale efficiently in AI chip manufacturing towards our long-term goal of producing one terawatt of compute each year.”

Then, one of the goals is to put this AI compute into space on satellite clusters, and power them with the cheap and abundant energy that the Sun provides:

“The Sun contains approximately 99.8% of the solar system’s energy and, as a result, we believe it is the only truly scalable solution to terrestrial energy constraints in the age of AI. Harnessing this energy in space is considerably more efficient than on land. Space-based solar arrays can generate more than five times the energy per unit area of terrestrial solar due to continuous illumination, lack of atmospheric interference, and optimal orientation.

In orbit, construction costs are replaced by launch costs and satellite production costs. We expect reusable launch systems and high flight cadence will significantly reduce the cost per kilogram to orbit, enabling more efficient deployment of compute payloads to orbit, and eventually approach the cost of fuel. We believe our advanced satellite manufacturing capabilities enable us to build AI compute satellites at scale and lower cost than competitors. Other terrestrial data center construction costs such as building the shell, MEP, and grid interconnection are not applicable in space. As a result, once Starship and our AI compute satellites are fully deployed at scale, we believe that the initial deployment costs of in-orbit compute in the aggregate will be less than construction costs of others’ terrestrial data centers.

In orbit, chips are expected to be powered by solar energy which is low cost and unlimited, and we expect to leverage radiative cooling architectures, which incur no operating costs compared to liquid or air cooling. Our integrated, space-based Starlink network architecture also enables more cost efficient routing of data between compute clusters and to end users on a global basis. We have already solved the hardest part in the development of AI compute satellites. AI compute satellites represent an evolution of spacecraft engineering already demonstrated at scale through Starlink’s connectivity satellites, and we believe development of AI compute satellites will be easier for us than for anyone else.

Connectivity satellites are primarily designed for communications, with substantial onboard equipment dedicated to phased-array antennas, radio systems, and data transmission. In contrast, AI compute satellites are optimized for high-performance computing. Key differences include significantly larger solar arrays to support higher power requirements, substantially larger radiators for thermal management, different electronics centered on AI accelerators rather than communications processors, and the removal of much of the communications hardware. Our V3 satellite platform already incorporates proprietary chips, providing a strong foundation for the ability to operate AI-focused electronics in space, and we expect to begin deploying our orbital AI compute satellites as early as 2028.

The primary remaining challenge is one of scale. For example, a deployment rate of approximately 10 gigawatts per year would require a materially lower manufacturing and launch cadence, which we believe would still enable a commercially attractive AI compute business with strong economic returns. While our long-term vision includes the ambition of deploying up to 100 gigawatts of power to orbit annually, which would require the deployment of thousands of launches per year, assuming 100 kilowatts of compute power per metric ton and Starship capacity to orbit of 100 metric tons, we believe we can be economically successful at significantly more modest volumes.

Specifically, we expect these satellites to leverage our already-designed V3 satellite platform. The core V3 satellite design is complete, and the AI compute satellites are expected to generate substantially more power than V3 satellites. This performance is expected to be achieved primarily through the use of significantly larger solar arrays. These satellites are targeted to generate approximately 100 kW of compute power per ton, which initially will require approximately five times the solar array output compared to V3 satellite designs. In general, the approach contemplates larger deployable solar arrays on each satellite, with no significant on-orbit assembly currently anticipated.

To ensure optimized thermal management and power generation, we will design each satellite’s solar arrays to face the sun for constant power while its housing radiator panels face cold deep space for radiative cooling. Space based compute also introduces orbital debris risk, which we already manage at constellation scale through our autonomous collision avoidance system across Starlink. To date, we have not experienced any failures of our autonomous collision avoidance system that have resulted in satellite loss.

We have built one of the largest satellite manufacturing operations in the world with standardized bus architectures, rapid iteration cycles, and automotive-style production lines, enabling us to evolve bus architecture and subsystem design with limited reliance on third-party suppliers. Our satellite constellation provides a direct, orbital data path that circumvents the bottlenecks of terrestrial communications networks. This architecture is particularly suitable to support high-speed connectivity for latency-sensitive workloads, which we believe are increasingly valued in certain consumer- and enterprise-facing applications.”

Each of Musk’s businesses scales based on “the algorithm”, which is basically a philosophy that every manufacturing process should be as simple as possible, and then be automated. These are the five steps to optimize manufacturing, crucially, the steps have to be completed in order:

1. Question Every Requirement

2. Delete Any Part or Process You Can

3. Simplify or Optimize

4. Accelerate Cycle Time

5. Automate

Let’s go through SpaceX’s current businesses in more detail..

Business 1: Rockets & Launch

The key to understand about the launch business is that the overarching goal is to drive down the cost of putting cargo into space. There are two ways to do this—increasing rocket reusability and building bigger rockets. The more times you can relaunch the same rocket, the lower the cost will be to put cargo into space. Similarly, if you can build a bigger rocket which can carry more cargo at once, again, the lower the cost per kilogram of cargo will be.

So, these are the two key factors which SpaceX is innovating on—building bigger rockets and increasing their reusability:

SpaceX describes the state of the space industry before its founding and how the company is transforming it:

“According to NASA, until the 2000s and the introduction of the Falcon 9 rocket by SpaceX, global commercial launch activity averaged 25 to 35 launches per year. As a result, the space industry remained a niche domain with limited ability to support large commercial markets or scaled space-based infrastructure. During this period, satellites—which comprised the majority of launch payload—were typically bespoke, expensive systems requiring significant non-recurring engineering that consisted of development cycles that were measured in decades.

Fundamental breakthroughs in high cadence, reliable, and affordable access to space—driven largely by SpaceX—have expanded space from a purely mission-driven activity to a fully industrialized and commercial sector capable of supporting and enabling industries far beyond traditional launch and satellites. SpaceX’s advancements reduced the cost of access to orbit from tens of thousands of dollars per kilogram to just a few thousand dollars per kilogram.

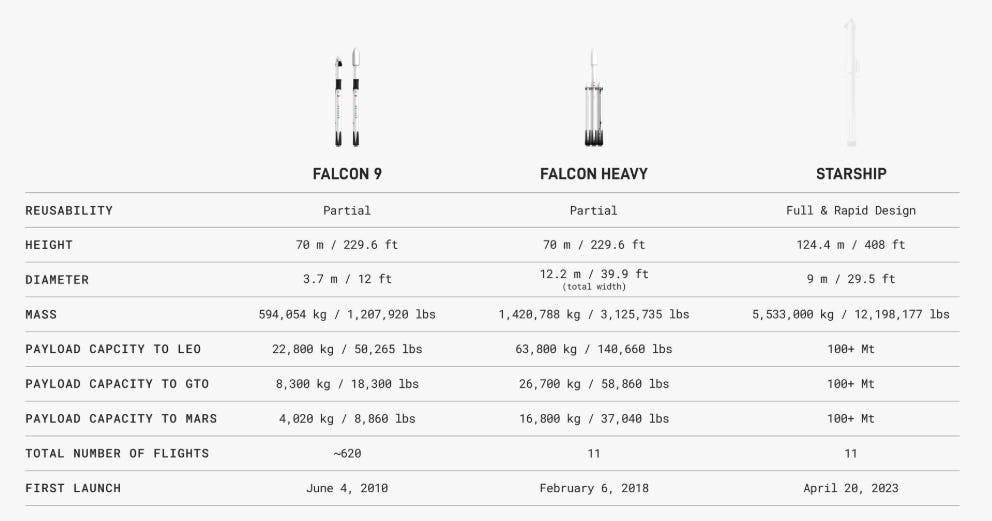

In December 2015, we achieved what many deemed impossible: landing a rocket launched to space back on Earth. By 2017, we were routinely recovering and reusing the Falcon 9 first-stage booster post-launch, delivering another step-function drop in space access costs via groundbreaking reusability. As of March 2026, our Falcon 9 rockets have demonstrated the ability to refly a first-stage 34 times. With the future deployment of Starship, which is designed to be the world’s first fully and rapidly reusable spacecraft, we aim to reduce the cost to reach orbit by 99% or more relative to the historical average launch cost, establishing the most affordable and scalable path to creating new opportunities in space.

Starship V3 is designed to deliver 100 metric tons to Earth’s orbit in a fully reusable configuration while enabling rapid turnaround times akin to commercial aviation. Future generations of Starship are being designed to double this payload capacity. To date, we have executed 11 Starship flight tests. We have also scheduled a 12th flight test, which will debut the next generation Starship vehicle and Super Heavy booster, powered by the next evolution of our Raptor engine and launching from a newly designed pad at Starbase. We expect Starship to commence payload delivery to orbit in the second half of 2026. We have achieved innovative milestones such as catching a booster using “chopstick” arms on the same tower it launched from. We expect this capability will facilitate rapid refurbishment and reuse, allowing for multiple launches per day at reduced costs.

Starship’s core design innovation is its full and rapid approach to reusability: both stages return to Earth for catch and rapid refurbishment. The Super Heavy booster returns to the launch site following stage separation and is caught mid-air by the launch tower’s mechanical arms, also known as “chopsticks,” to facilitate immediate inspection, refurbishment, and relaunch. The Starship upper stage, after orbital delivery or missions beyond, is designed to reenter protected by advanced heat shield tiles, execute a propulsive landing burn, and be similarly caught mid-air by the launch tower’s mechanical arms. We believe that Starship’s full and rapid reusability will enable sub-one hour reflights, causing a paradigm shift in launch cadence.”

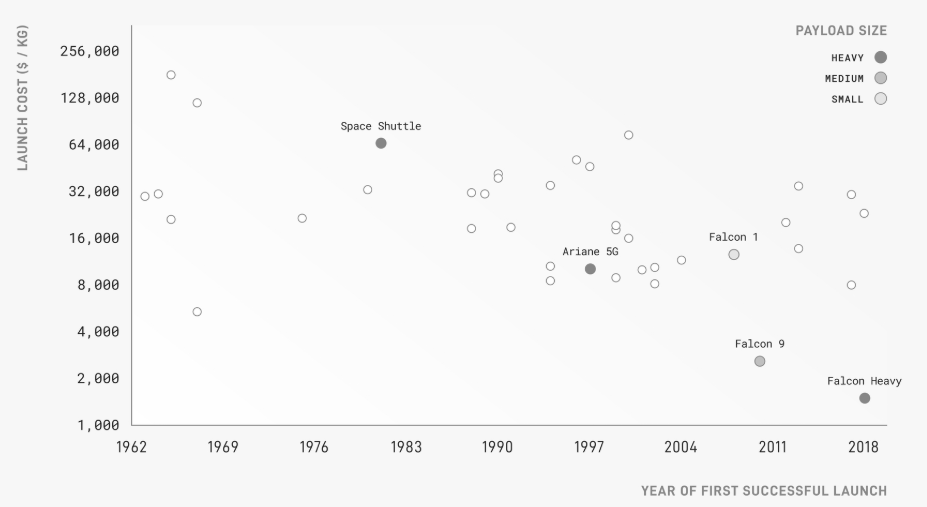

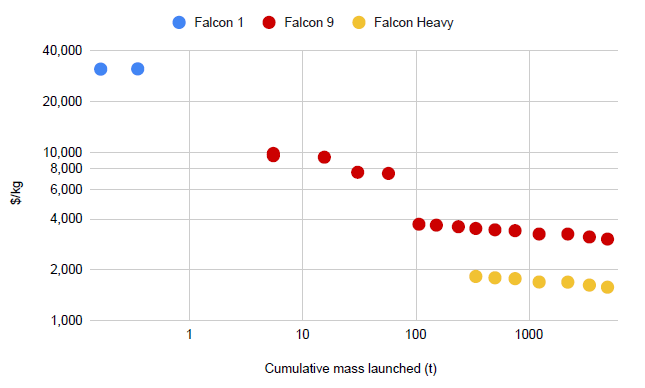

Historically, launch costs were high—it used to cost about $8,000 to $64,000 to put one kilogram of payload into orbit. As a result, not much was being put into orbit before SpaceX’s founding. You can see that SpaceX’s Falcon 9 and subsequently Falcon Heavy really drove down the cost, which then allowed the company to put its massive Starlink constellation into space:

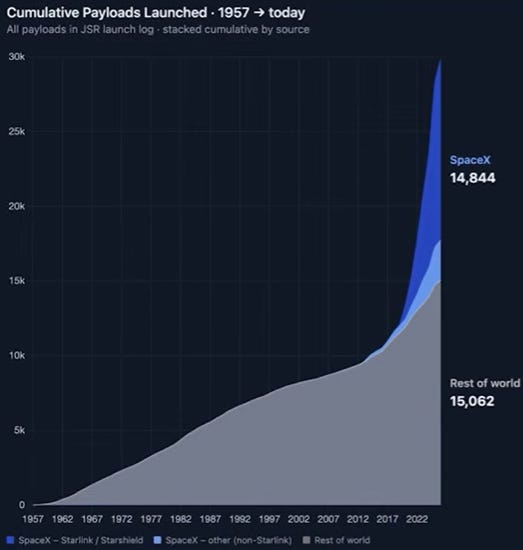

Basically, half of all payloads which have been put into space throughout history have now been carried out by SpaceX:

The initial goal of Starship is to reach a cost of $185 per kg to put a payload into space, although Elon has mentioned that $20 per kg is the real goal. Google estimates based on historical learning rates in other industries that SpaceX’s launch costs should fall to less than $200 per kg by 2035, a level at which it would become economical to put their TPUs onto satellites. This is Google’s analysis on the learning rate of Falcon 9 and Falcon Heavy, and how these have been driving down the launch cost per kg:

SpaceX sees its competitive advantage in the launch and space industries as vertical integration, allowing the company to innovate quickly to improve its products such as rockets:

“While conventional aerospace manufacturing relies heavily on fragmented and outsourced supply chains, we operate with extreme vertical integration. By designing and manufacturing a significant portion of our components in-house, we bypass many of the slow, bloated sourcing channels that structurally constrain the rest of the industry. For example, approximately 80% of Starship, SpaceX’s next-generation launch vehicle, is manufactured in-house. Our vertical integration allows us to achieve iterative cycles in weeks, compared to years for some legacy companies, enabling us to build newer, more technologically advanced products faster than many of our competitors.”

A good example here is the Raptor engine, with the latest version being shown on the right below, and which will power Starship:

Business 2: Starlink

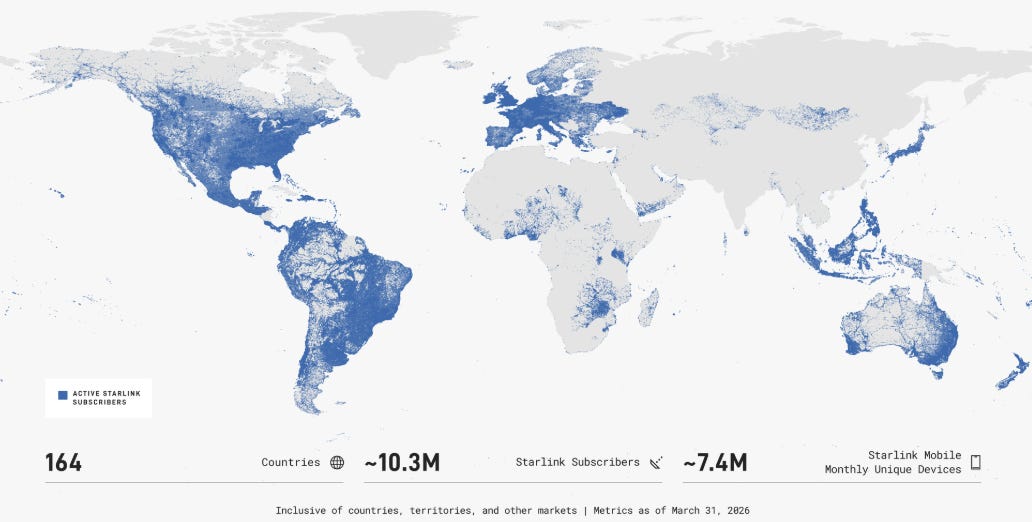

Starlink is currently the high-growth cash cow for SpaceX. The service already has 10 million subscribers, up more than 100% from one year ago. The below map beautifully illustrates where those subs are located. Obviously there is still large growth potential as more people become aware of Starlink, more countries will allow the service in the future, and as SpaceX will launch a mobile service as well.

SpaceX provides further details on Starlink:

“We operate the world’s largest and most advanced space-based internet broadband service with median latency at approximately 25 milliseconds. We provide fiber-like download speeds—at a median of 225 Mbps during peak hours for residential users—and the technological capability to provide service everywhere on Earth, including the poles. This service quality is enabled by our vast network of approximately 9,600 Starlink broadband and mobile satellites in Low-Earth Orbit, which accounted for approximately 75% of all active maneuverable satellites in orbit as of March 2026.

We expect to commence deploying our next-generation V3 satellites, designed to offer one Tbps of downlink capacity per satellite, using Starship in the second half of 2026. We expect that a single Starship launch will be capable of deploying up to 60 V3 satellites to LEO, representing a potential twenty-fold increase in Starlink downlink capacity deployed relative to a Falcon 9 launch.

We charge our Starlink Subscribers a monthly subscription fee, which varies based on geographic market and download speed, plus typically a one-time upfront terminal cost. SpaceX is a critical partner to a wide array of enterprises. We offer Starlink to enterprise customers across industries including construction, agriculture, retail, telecom, hospitality, aviation, maritime, and land mobility. Starlink’s unique capabilities are well‑suited for deployments across field offices, remote worksites, research stations, drilling rigs, rural hospitals, aircraft, cruise ships, trains, and hotels. Our enterprise customers include companies such as United Airlines, Carnival, Maersk, and John Deere, among others. We also serve a broad fixed‑site customer base across industries such as retail and financial services that require high availability for critical operations.

Our enterprise contracts are based on a combination of subscriptions, data consumption, capacity, or other pricing models depending on each customer’s particular needs. Since 2023, no Starlink Enterprise customer having contributed more than $750,000 of annual revenue has voluntarily discontinued their service, demonstrating the strong performance and value of our offering.

We provide satellite-to-mobile connectivity. Our current capabilities under our “V1” constellation (consisting of approximately 650 V1 Mobile satellites in orbit) include light data, text messaging (SMS), and over-the-top voice services (e.g., WhatsApp and FaceTime). We are developing more comprehensive satellite-to-mobile services, including broadband data and IoT connectivity, which are expected to deliver resilient, infrastructure-independent connectivity worldwide and enable 5G connectivity. We have partnerships with approximately 30 MNOs on six continents, covering an area that is home to approximately 1.9 billion people. We charge MNOs either a fixed fee or a per-mobile user fee-based amount, which is typically passed through to the customer via the carrier as an “add-on” feature.

According to the Global Satellite Operators Association, terrestrial network infrastructure only covers approximately 20% of global land mass, resulting in significant unserved and underserved regions across both developed and developing economies. This terrestrial connectivity gap spans areas that are remote, difficult to build in, or economically impractical to serve—and also includes mobile “dead zones” within otherwise well-connected areas and in urban markets. According to the J.D. Power U.S. Wireless Network Quality Performance Study, U.S. wireless customers experienced service problems in approximately one out of every 11 mobile interactions, even in well-connected areas. As demand for ubiquitous, high-reliability connectivity continues to rise, terrestrial networks alone are increasingly unable to bridge the widening gap between user demand and available coverage.”

Starlink is an attractive partnership for mobile network operators (MNOs) as they can offer their customers connectivity everywhere as a premium service.

Starlink is also a business with a huge moat—you need enormous amounts of capital to launch all these satellites into space, you have to get SpaceX to agree to launch these satellites for you, and you also need huge capital to buy the spectrum to offer mobile services. SpaceX disclosed they’ll be spending close to $20 billion to purchase spectrum.

The raised capital from the IPO can also be used to advertise this business worldwide, as many target customers won’t even be aware it exists:

“We intend to grow the number of Starlink Subscribers by expanding our consumer distribution network across thousands of authorized retail stores globally and execute region-specific marketing campaigns to increase Starlink brand awareness. By clearly demonstrating Starlink’s superior speed, low-latency, affordability, and ease of installation—not only in rural, remote, and infrastructure-limited areas, but also in suburban and urban areas with wireline broadband options—we expect to drive meaningful subscriber and revenue growth.”

Business 3: Frontier AI & Colossus

SpaceX, due to its xAI acquisition, has quickly become the most impressive builder of AI capacity in the world:

“COLOSSUS and COLOSSUS II collectively provide approximately 1.0 gigawatt of compute power, with additional power capacity available for data center operations. We believe speed is a competitive advantage. In order to bring compute clusters online as fast as possible, we employ a vertically integrated, nimble approach to construction.

At COLOSSUS, we brought online the first cluster of approximately 100,000 H100 processors, approximately 130 megawatts of compute power, in just 122 days, repurposing the shell of an existing factory. At COLOSSUS II, we brought online the first cluster of approximately 110,000 GB200 processors, approximately 210 megawatts of compute power, even faster in 91 days. As an illustrative comparison, an industry benchmark to bring online a 100 megawatt greenfield data center is approximately two years.

Furthermore, in the case of COLOSSUS II, following the initial cluster, we brought online the second cluster of 110,000 GB300 processors and 220 megawatts of compute power in 64 days, demonstrating our ability to rapidly scale our facilities once built. We expect that once fully operational, the next phase of expansion at COLOSSUS II will bring online at least 220,000 additional GB300 processors and over 400 additional megawatts of compute power. We also demonstrated a significant improvement in cost efficiency, achieving data center construction costs for COLOSSUS II that are considerably lower than industry benchmarks on a per megawatt basis.”

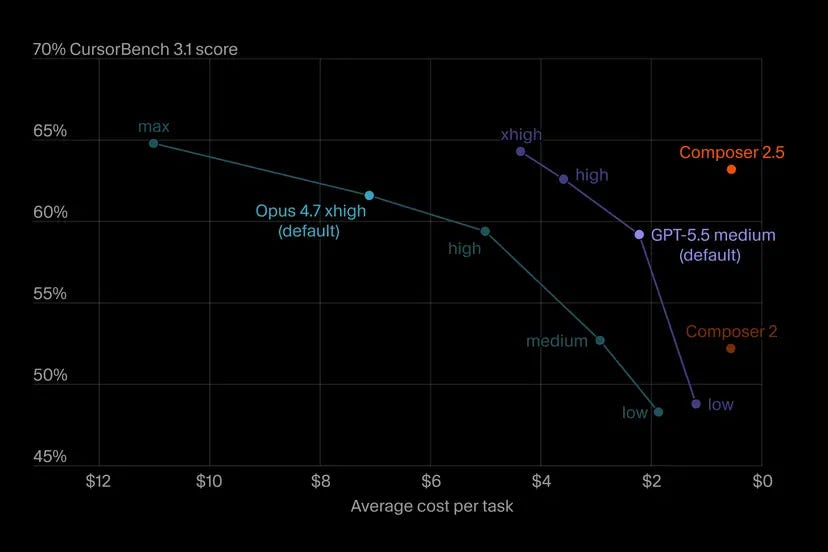

These data centers serve a dual purpose. On the one hand, a Colossus data center can be used for inference and training of internal AI models such as Grok and Cursor’s Composer model. Note that SpaceX already has an agreement in place to acquire LLM coding specialist Cursor later this year. With Cursor obtaining access to xAI’s data centers, they quickly have been able to improve the capabilities of their Composer LLM via reinforcement learning. Based on the below benchmark test, Composer 2.5 has similar coding capabilities to Claude Opus 4.7 and ChatGPT 5.5, but at a much lower cost per task:

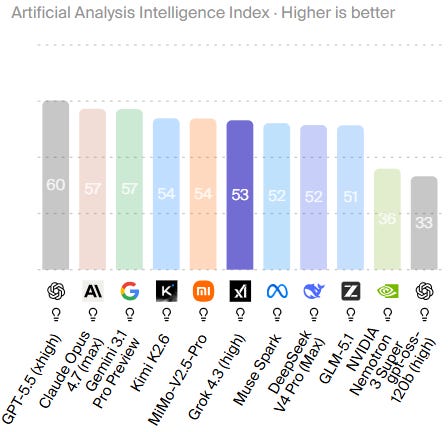

Artificial Analysis finds similar results:

“Composer 2.5 sits in third place on the Artificial Analysis Coding Agent Index, behind only higher-effort variants of Claude Opus 4.7 and ChatGPT-5.5 which cost ~10-60x more per task. This release puts Composer among the leading coding agent models, something that wasn’t clear for past releases.”

In addition, Grok is also an extremely capable model that is competing at the frontier of intelligence. Now that Elon is completely overhauling xAI—last year he was still leading the DOGE effort in the Trump administration, so xAI was more of a side project—xAI should become more competitive in the coming years.

However, three factors are crucial to compete at the frontier in AI—one is compute power, second is access to the best quality data sets, and third is engineering talent to innovate on algorithms and model performance. As the company has access to a massive training cluster with its Colossus data centers, xAI is obviously extremely well positioned when it comes to compute power. In coding data sets, Microsoft/OpenAI can have an advantage due to Microsoft’s ownership of Github, however, due to reinforcement learning, huge synthetic data sets can be created. Anthropic currently has the lead in coding which suggests that Microsoft’s ownership of Github might only be a limited competitive advantage.

Finally, access to engineering talent is crucial as well. Obviously, Google, OpenAI, Anthropic, Meta, as well as various AI startups, are all well positioned to attract AI talent. This is likely the reason that SpaceX made an agreement to acquire Cursor and is looking to acquire other AI startups as well—i.e. to get access to top talent. In addition, xAI recently formed a specialized recruitment unit made up of engineers themselves reporting directly to Elon Musk. These recruitment engineers are tasked solely with finding unconventional top talent and poaching them. There is a lot of math, physics and engineering talent around the world, and so looking outside the obvious circles where every AI lab is recruiting could give the company some unique capabilities. For example, Albert Einstein was also just an employee at a patent office who started writing physics papers in his spare time. Nikola Tesla never graduated university and gained his insights with self study. There are lots of examples throughout history of finding rare talent in unexpected places.

Given that xAI has the compute power and that they should have sufficient access to quality data sets, its success will likely hinge on factor number three, getting access to top talent that can train models that enterprises and consumers want to use. SpaceX disclosed that Grok 5 is currently being trained in the Colossus II data center.

We expect frontier AI to be a high-moat business with scale and networking advantages. SpaceX makes a similar conclusion and thinks that they will obtain a competitive advantage in hardware and energy:

“Only operators with access to massive amounts of power, very large GPU clusters and tightly integrated training infrastructure can train cutting-edge models, and these systems exhibit non-linear performance advantages that compound over time.

Companies that can structurally reduce energy, compute, networking, and deployment costs per token will be positioned to train faster, iterate more rapidly, and ultimately manufacture greater intelligence, scale models more rapidly, and deliver increasingly powerful and accessible AI solutions. This creates a self-reinforcing advantage in which lower token costs drive greater model quality and user adoption, reinforcing AI leadership. This is because lower cost per token enables more frequent model training, larger and more sophisticated models, longer chains of processing for reasoning and agentic workloads, and significantly higher inference volumes at economically viable prices.

Accordingly, for a given level of intelligence, we expect the long-term economics of AI companies to be driven by the ability to consistently deliver bleeding-edge compute at the lowest possible cost per token. Put simply, we view cost per token as a function of three primary inputs—the underlying AI model, the compute hardware, and energy, and we expect to have a competitive advantage in the latter two cost components. We believe we have a pathway over time that will significantly reduce compute hardware costs through continued vertical integration and development of proprietary chips, building on our experience designing custom silicon for our Starlink satellites. We also expect that the marginal cost of energy for our AI compute satellites will be minimal because our satellites are powered by solar arrays in space. By driving the energy component to minimal levels and pursuing improvements in compute hardware cost, we believe we can achieve a meaningfully lower overall cost per token in the future.

We believe that diversifying our long-term access to the supply of processors, including through our Terafab initiative with Tesla and Intel, will be a key driver in reducing the overall cost of compute hardware over time. By combining internally manufactured, lower cost chips with those we source from third-party suppliers, we expect the overall cost of our processors to decline.”

Our reading here is that SpaceX is banking on Terafab to give them a competitive advantage in hardware development, where a closed innovation loop with their fab will enable fast iteration to drive hardware innovation. Secondly, due to the company’s prowess in launch and satellite manufacturing, the vision is to have a competitive edge on the energy side as well, with the company’s AI compute being powered by continuous and low cost solar energy in space.

SpaceX’s current Colossus data centers can also be utilized as neoclouds with capacity being rented out to other AI providers. The company recently signed an extremely lucrative contract to rent out its Colossus I data center to Anthropic. Anthropic had massively underestimated demand for its Opus model, and so the AI lab has been scrambling to get more access to compute. Thanks to the Colossus I data center, Anthropic can now double each user’s rate limits, which had been severely restricted. The SpaceX-Anthropic deal also includes an agreement to explore building multiple gigawatts of AI compute in space.

SpaceX estimates that $7 trillion in AI capex will be needed through 2030 given that frontier AI remains infrastructure constrained:

“Massive demand for frontier AI models is accelerating the build-out of AI infrastructure at a pace and scale with few historical precedents. Meeting projected AI needs will require $7 trillion in global data center investment through 2030, with generative AI workloads expected to account for roughly 70% of total data-center power demand by the end of the decade. Each new generation of frontier models requires exponentially greater compute, following well-established scaling laws that link model performance to the volume and quality of training data, parameter count, and total compute expected. The rise of agentic AI and the potential emergence of artificial general intelligence are expected to further amplify inference workloads, driving a step-function increase in compute requirements and the corresponding data center capacity needed to support them. Frontier AI has become fundamentally infrastructure-constrained.”

SpaceX is clearly a highly innovative and vertically integrated company that’s working on a set of the hardest problems in engineering. The company dominates in the rockets & launch industry, Starlink is obviously a crown jewel, and the company is now competing at the leading edge in AI, which is already the fastest growth market of all time. We expect AI to grow into a massive industry over the coming decades, where the winners will likely become the biggest companies in the world in terms of market cap.

Below, we’ll go through SpaceX’s current businesses and opportunities to assign a valuation to each of these. At the end, we’ll sum up all these individual valuations in a sum-of-the-parts framework to see at what valuation we’d be interested to purchase the shares. IPOs are volatile. Facebook crashed more than 60% in the months following its IPO—which gave a tremendous buying opportunity for long term investors. So, it’s a good exercise to go through at which levels we’re ready to buy.