Shopify in an increasingly competitive e-commerce market

An overview of the space post Shopify’s investor day

Shopify held its first investor day in four years which led me to revisit the company. It’s a company which I like a lot, as I invested in the shares shortly post IPO, holding the position for around 5 years.

Shopify is a software-as-a-service (SaaS) platform to manage e-commerce stores. This means that aspiring online retailers can start and scale a store without having to invest in infrastructure, as the software runs in the cloud in return for a monthly subscription fee, as well as a percentage of gross merchandise volumes (GMV) where Shopify takes care of the payment processing.

This is a good business as you get exposure to the growth in e-commerce combined with the attractions of a software business, meaning that customers don’t tend to switch software providers, especially if they run the core of the business on the software, and that over time we should get attractive margins when growth matures.

Competition is heating up in the e-commerce space. For example, in South-East Asia, there are number of strong players such as Shopee, Lazada and Tokopedia. Recently we also saw the introduction of TikTok in this market, taking rapidly a mid-teens market share. However, after Indonesian regulatory banning e-commerce over social media, TikTok has now decided to take a large stake in Tokopedia which should reduce competitive pressures, effectively moving back to a market with three large players.

Nikkei Asia describes the competitive pressures for Lazada: “China’s Alibaba has invested an additional $634 million in Singapore-based e-commerce subsidiary Lazada amid an intensifying battle with TikTok and others for the Southeast Asian market. The company is trying to defend its market share against rising competition in the region.”

Additionally, Shopee is expanding around the globe, opening an e-commerce platform in Brazil for example while taking a substantial share of the market. Its key competitors are both Amazon and market leader MercadoLibre:

Taking a bird-eye’s view, it strikes me that competition is heating up in e-commerce, as players around the world have replicated Amazon’s operating model and are now moving into each other’s markets. I suspect there will be around 3 strong platforms per market or region, and if those players decide to remain reasonably disciplined on pricing, that should translate into attractive profits still. A good example is MercadoLibre, which is generating attractive 15% operating margins.

Shopify is still heavily focused on the North-America market with 65% of GMV coming from this region so should be better isolated from the potential competitive pressures described above. However, other large platforms are trying to grow share in the US e-commerce as well, such as Walmart and Temu (more on the latter in a bit).

Traditionally Shopify has provided the software to SMBs who market directly to the consumer over social media or via Google Search. A good example here is ‘Mr Beast’ who runs his own webshop over Shopify. While Amazon is fairly dominant in e-commerce in Shopify’s core markets such as the US and the UK, it hasn’t stopped Shopify from generating attractive growth rates, indicating that their customers’ mom-and-pop e-commerce model is working:

In the meanwhile, Shopify’s GMV has gotten sizeable at USD 222 billion, compared to around USD 750 billion for Amazon.

However, fast-fashion retailers Shein and Temu — the latter owned by Pinduoduo — are another good example of increasing competition:

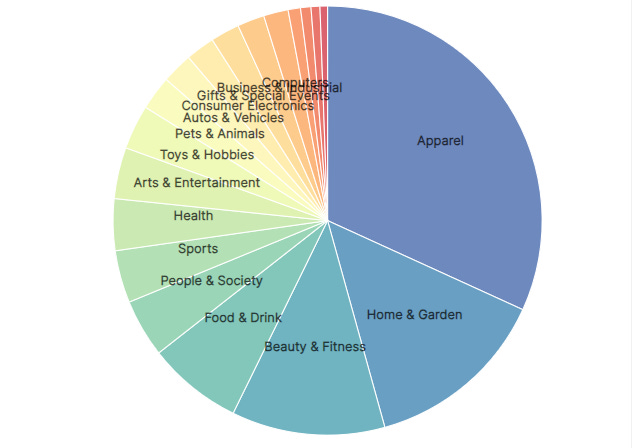

And as around 30% of Shopify’s shops are active in apparel, this could be a threat for a decent part of the business:

Temu doesn’t only sell fast-fashion, but a wide variety of categories, from Barron’s: “PDD’s overseas platform Temu — which became the most-downloaded app in the US and much of Western Europe after it was rolled out in September 2022 — has eaten into sales for Amazon and Shein, the latter of which it surpassed in sales revenue in May. PDD’s rapid rise is due in large part to its innovation in two key areas, said Doug Young, director of Hong Kong-based Bamboo Works, which analyzes Chinese companies listed in Hong Kong and abroad. The first is pricing, which Pinduoduo has kept low by working more directly with sellers, who are often actual manufacturers, giving the company much stronger pricing power, Young said. By comparison, Alibaba often works with merchants who aren’t actual manufacturers. The second is the social element, which ‘PDD has excelled at by getting people involved in group buying, and getting their friends and family members and anyone else they know to buy things,’ he said.”

However, going over Temu’s website, obviously it is a lot of cheap stuff, whereas Shopify’s merchants will also be selling brands. The only branded running shoes I found on Temu were ‘Skechers’, a brand I had vaguely heard of before.

When it comes to brands, Shopify is now even moving into the enterprise market, where brands such as Suntory and Unilever have decided to run their e-commerce operations over the platform:

To get access to these larger brands, Shopify has partnered with the typical IT services companies and listening to the investor day, it sounds like this will accelerate growth for the company. Shopify’s CRO discussing this:

“In ‘22, we went out and got Accenture and Deloitte. In ‘23, we’ve been working very hard to bring all these other strategic partners on board. Now here’s a datapoint none of you have heard before: $20 billion in GMV is in pipe right now from the partners that you see listed on this board. Three things are pretty clear that enterprise customers tell us over and over again, we win because of the best TCO (total cost of ownership), we win because we have the best converting platform on the planet (turning shopping baskets into a paid checkout), and we win because we future proof them with our speed of innovation.”

USD 20 billion is almost 10% of current GMV so that’s a nice uplift already. However, the margins Shopify is making on these large enterprises will naturally be lower than it generates on mom-and-pop stores. Nevertheless, this should provide nice earnings growth still.

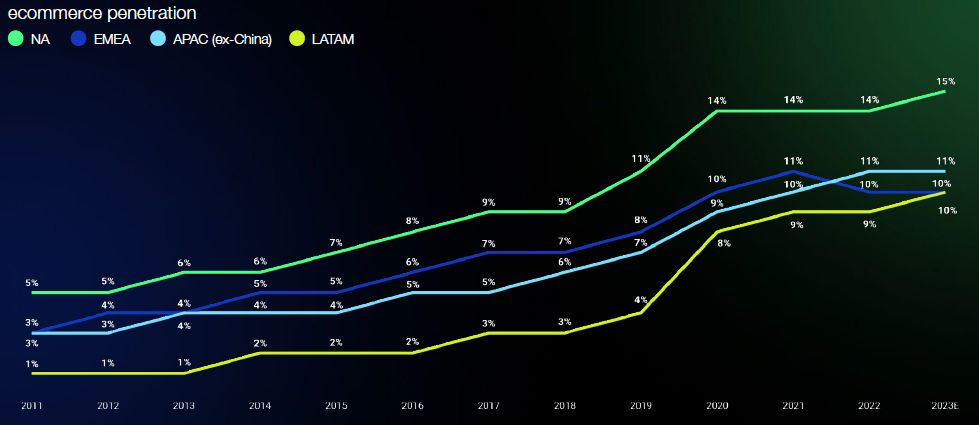

Another runway for growth is e-commerce’s still modest penetrations in the overall retail market:

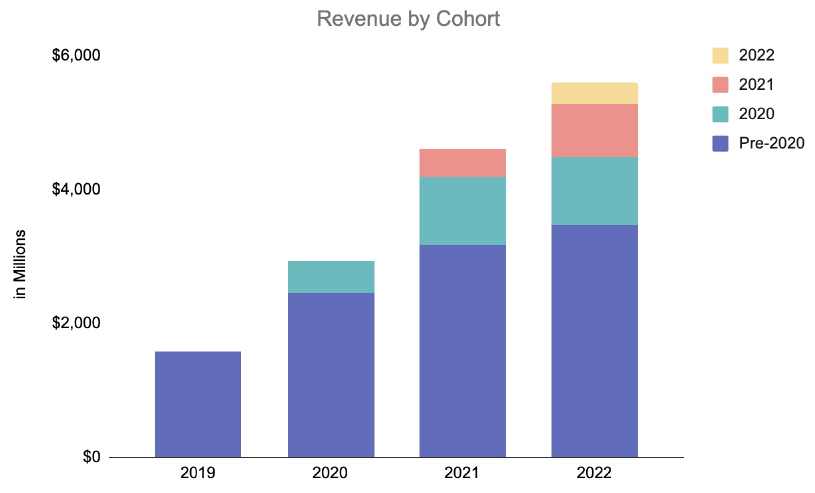

As a result, Shopify’s merchants are showing attractive revenue growth:

The company’s CRO discussing how they’re helping their customers grow in size: “The mid-market of today is the enterprise of tomorrow, 18% of our mid-market accounts are growing at over 40% and 25% of our large accounts are growing over 40%. We actually are now surrounding our fastest growing customers with increased technical capabilities and support to help them get to this next level of growth.”

Shopify’s software handles both the webfront as well as the back-office functions to manage a merchant’s business, such as managing orders, inventory, logistics, customer communication, analytics, sales channels, and marketing tools to compete with the likes of Hubspot. Clearly, Shopify has become a very comprehensive platform.

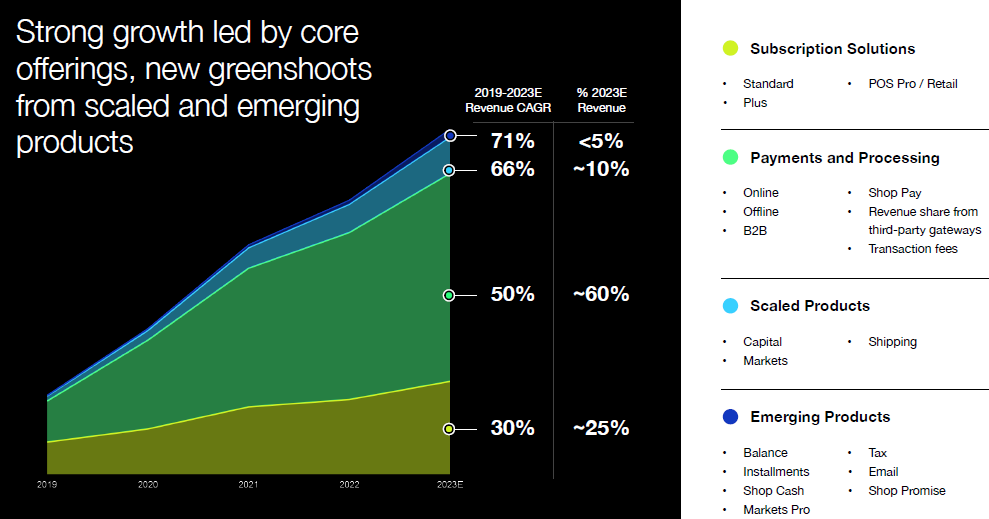

In the meanwhile, payments processing has become the largest source of revenues and the company has developed its own Shop Pay checkout button here to compete with the likes of Paypal. The below slide gives an overview of Shopify’s various revenue streams. For example, large companies pay a higher software subscription fee (the Plus solution) and the company is also working on emerging products such as providing their merchants with financing.

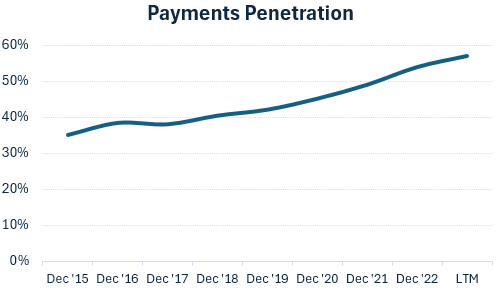

The party in payments growth is far from over, besides the clear growth path for the e-commerce sector as a whole, Shopify is currently only processing around 60% of their merchants’ GMV:

Shopify’s COO discussing the popularity of the Shop Pay button: “Shop Pay, as of a few months ago, is now the number one checkout method. Recently, it became more popular than guest checkout with a credit card. More than 100 million buyers have opted into Shop Pay.”

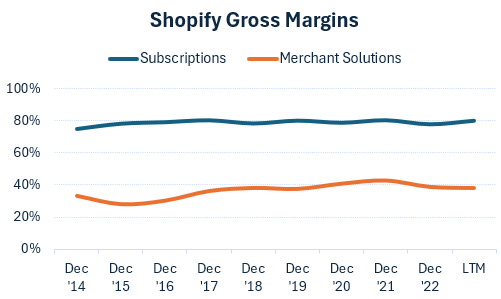

Shopify divides its revenues into two businesses, software subscriptions and merchant solutions (where payments processing is a large contributor). As the merchant solutions business is lower margin compared to software subscriptions, on a gross profit basis both segments’ contribution is more balanced (chart below). Although clearly the merchant solutions are delivering the highest growth:

Shopify’s software subscriptions are generating gross margins of around 80%, whereas merchant solutions is currently at 38%:

Competitive landscape in e-commerce SaaS

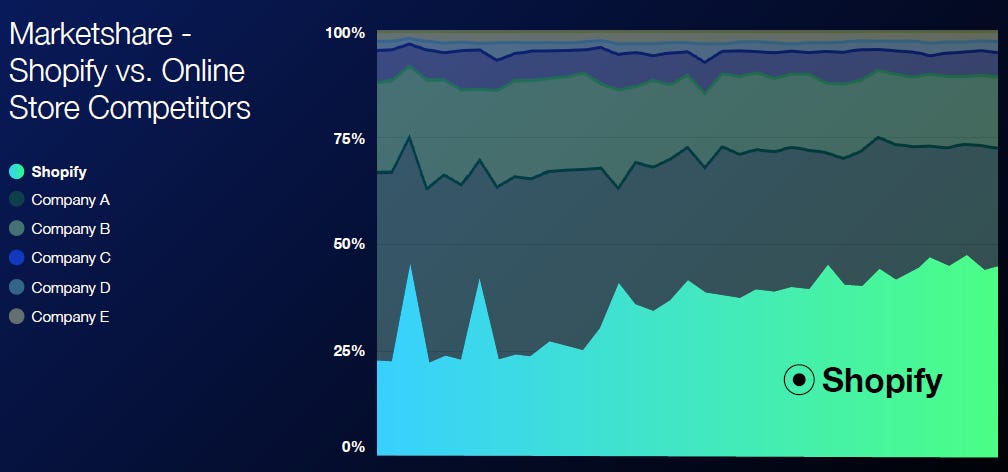

On Shopify’s provided market share data, the company is winning market share versus its competition in e-commerce SaaS:

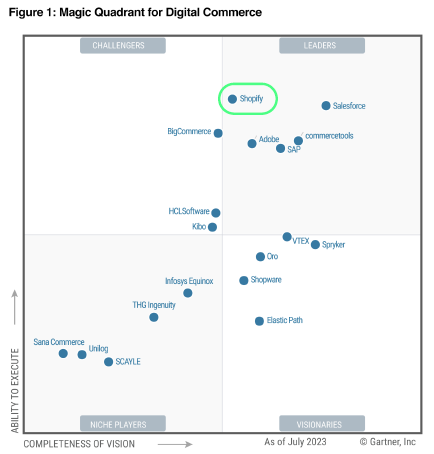

Also Gartner has selected Shopify as a leader (chart below). Both Salesforce and Adobe entered this field by acquisition, Salesforce acquired Demandware in 2016 and Adobe made the acquisition of Magento in 2018. Both of these names are oriented towards the enterprise market whereas Shopify’s bread-and-butter are SMBs.

Shopify’s CRO discussed their competitive position at the investor day: “Mid-market, we define as USD 2 to 20 million in GMV, we’re winning 43 to 1. That means we’re taking 43 of customers coming to us from competition for every one that we lose. When customers replatform to Shopify, very rarely do we see them leave. As we stretch up market, in large, we’re winning 26 to 1 and in enterprise, we’re winning 38 to 1. We are absolutely disrupting the competitive environment at all 3 levels in the marketplace. We’re taking real market share from all the major players. There is a lot of focus on future proof, companies are looking to modernize their stack. They don’t want to be locked in into a platform where they feel like the thing has not moved for a decade, like in the case of Demandware.”

The CFO afterwards discussed the enterprise market: “I don’t want to get ahead of ourselves on enterprise because they’re longer sales cycles and longer implementation cycles, but we are seeing the early signs of success and we’re going to continue to win more enterprise customers. Large enterprises generally have lower churn rates than the small businesses.”

So although the enterprise market will be lower margin, the lower churn rate is attractive for investors. SMBs typically have higher churn rates simply because 5 to 10 percent of them go out of business every year, which has to get replaced with new entrants.

Shopify’s strong position is translating into pricing power, the company recently took up pricing with very little pushback from their merchant base. The company’s president discussed this at the investor day: “It was the first time we increased pricing, we went from 29 to 39 dollars (on the standard software subscription), a 33% increase. We didn’t see much pushback from our merchants. When you think about a price-to-value ratio, it’s so far on the side of value. We like that and we want it to be almost too good to go from a pricing perspective, but it did obviously provide us with the proof point that there are other areas where we could increase the price.”

The CEO also discussed how they’re looking at price increases on other products during the Q3 call: “We’re really thinking about how to monetize which products and when. And we’re doing that across the board, whether it’s when do we monetize Audiences, when do we look at pricing on Shopify Plus, or the enterprise offering. And I think the success of the Standard price change earlier this year proved to us that we can incrementally change our pricing in the future.”

Additional growth drivers

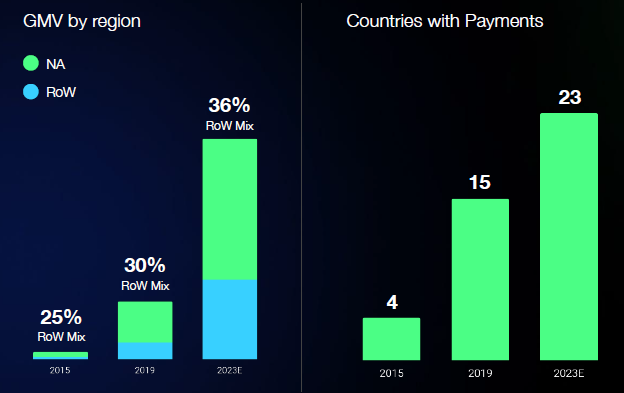

Historically Shopify has been heavily focused on North-America and this region still contributes more than 60% of GMV today. However, the rest-of-world has gradually been expanding in the mix:

Shopify’s CEO discussing their international growth on the last earnings call: “We delivered considerable GMV and merchant growth in key European markets like Germany, France, and the UK, with GMV in these three markets growing greater than 2x for all other geographies. With our growing international and cross-border tools, we are increasing the ways for merchants to reach customers in new markets with ease. And with our growing network of partners, merchants can offer their products on even more channels and surfaces. Cross-border GMV was approximately 15% of total GMV in the quarter.”

Shopify has been building new tools for merchants to easily sell into other countries, such as converting the website to the appropriate currency and providing the back-office tools to handle international taxation and shipping. Shopify’s CEO explaining this:

“In late September, we successfully launched Markets Pro in the US, attracting thousands of merchants to this new product. Markets Pro takes on the most stressful and time-consuming elements of international transactions so our merchants don’t have to. Markets Pro is a great option for merchants looking to scale to new countries quickly without having to navigate international tax compliance or fraud while tapping into the best-in-class international shipping options with prepaid duties. We’ve introduced things like foreign exchange hedging, express international shipping, tax compliance.. And now merchants like Mr Beast, WOLFpak and Made by Mary, very large merchants, are already using it. Since the rollout, the product has become one of the fastest growing and we cannot wait to expand its accessibility to other countries in 2024. It’s built on top of our Markets platform which has been out for a while, and which gives merchants the simple tools to launch localized products and essential features for international selling.”

The platform has also been adding integrated functionality to easily sell over other market places such as Amazon, Ebay, Etsy, and Walmart, as well as social media. This module is called Marketplace Connect. The highest profile of these is that merchants will also be able to offer shipments over Amazon Prime. Shopify’s CEO detailing this: “We announced our partnership with Amazon, which will release an app in Shopify’s ecosystem in the coming weeks, giving merchants the choice to offer ‘Buy with Prime’ directly within their Shopify Checkout. All of it will be processed by Shopify Payments.”

So this looks like a win-win relationship for both Amazon and Shopify. Amazon gets higher utilization rates within their logistics network, and Shopify makes profits on the payment processing.

Shopify is also moving offline, providing terminals and software to physical stores. Who can then run a true omnichannel experience over the platform, combining both online and offline sales management. Currently offline is contributing around 7% to revenues and Shopify has closed a partnership with widely used accounting software Intuit to cross-promote the product. Shopify’s CEO discussing this on the latest call:

“Offline GMV increased 26% year-over-year in the quarter, driven primarily by larger retailers joining the platform. The strength of our unified commerce platform and scalability of our retail channel continues to draw in major omnichannel retailers like Banana Republic, Princess Polly, and the Sacramento Kings. We have worked consistently to build out the features and functionality that larger multi-location retailers require. Of the business we did in Q3, 68% came from people who did not have Shopify as e-commerce already.”

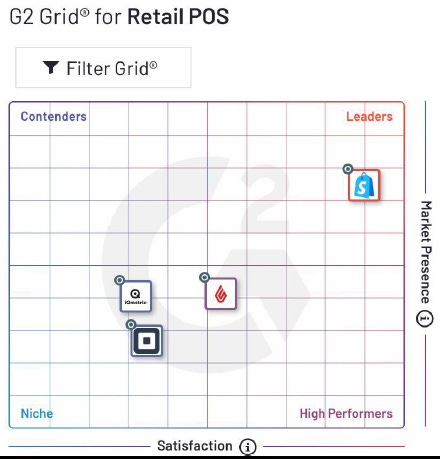

So the company is really starting to compete here with the likes of Block (Square), Toast and Shift4. For what it’s worth, take it with a grain of salt for the moment, according to the below consultant Shopify has a very strong offering in this market. This could be the case thanks to their partnership with Intuit, which naturally has a lot of clout to promote Shopify’s product. But naturally Square is the gorilla in the room here, so take the below chart with a healthy dose of scepticism:

Given Shopify’s widespread merchants and customers network, there is obviously a lot of data to train large language models on and develop copilots. The COO discussed this at the investor day:

“Over 150,000 data entry points come in every single week and we catalog every single client engagement we have. What this allows me to do, as a product builder, is hear everything every Shopify customer has said, summarized by AI, and be able to click deep into the actual conversation.

Copilot Magic basically takes out all the administration out of sales: which customer to call, what should we be talking about.. It will also score the sales’ client engagements, it will tell you how to get better, help you address those opportunities coming out of calls, and write the emails to the clients. So our sales teams can spend more time talking with customers.

Shopify Sidekick encapsulates all the knowledge of what Shopify is and make that disposable for the merchants. Thinking about everything from ‘is this the right layout of my website’, ‘am I selling the right SKUs’, ‘should I go into this geography’, and ‘which analytics should I be looking at’.”

The Shopify platform also has an app store which makes another 11,000 apps available that merchants can make use of. This is obviously a nicely differentiating feature which will be hard to replicate for new competition trying to get into the industry.

Shopify Audiences helps merchants to buy better ads online and the company mentioned this can lower merchants’ customer acquisition costs up to 50% in some cases. The CFO disclosed that they’re not monetizing this product yet, currently the only monetization is from the payments processing on the increased sales merchants are generating.

Shopify Capital makes a lot of sense, as Shopify knows their merchants better than the banks. So the company can opportunistically provide short term loans when the their clients might have to make an investment for their shop. Shopify is partnering with both Stripe and Adyen to organize this.

So this section should make clear that the company is building products at high speed and has the room to increasingly start monetizing these over time.

Shopify’s software engineering ethos

Quite some time at the investor day was spent on Shopify’s pace of innovation and how this came to fruition, the company’s COO diving into this:

“Most companies are built around managers, the people who don’t build things. Our commitment is to make Shopify a crafter’s paradise and we are going to continue to push the company away from layers and layers of management. So our senior engineers at Shopify are spending 22% less time in meetings than they used to and the number of projects completed by product manager is up 56% year-over-year. Flatter companies just tend to be faster and we want Shopify to be incredibly fast. When companies get big, everyone becomes a vice president, we don’t want Shopify to be governed by an organizational chart. So we built a piece of software, GST is a lightweight operating system that provides visibility on projects across Shopify. Everyone at Shopify works on a project and those projects ladder up to missions. All missions at Shopify are reviewed every six weeks by Shopify’s leadership team, which is full of nerds and engineers.

Tesla builds cars but they spend a surprising amount of time building bespoke robots that build the cars rather than building the cars directly. We spend a lot of our time building software to build the software. This has been incredibly rewarding. This summer, we invested some time in automating HR tools. We’ve been able to write code to reduce the number of workflows handled by talent operations by 50%. No matter where you look across the company, we’re finding ways to make things happen faster. People at Shopify don’t waste time waiting for responses, we’re building APIs, and we think that will help make Shopify have the ability to stay flat over a very long time.”

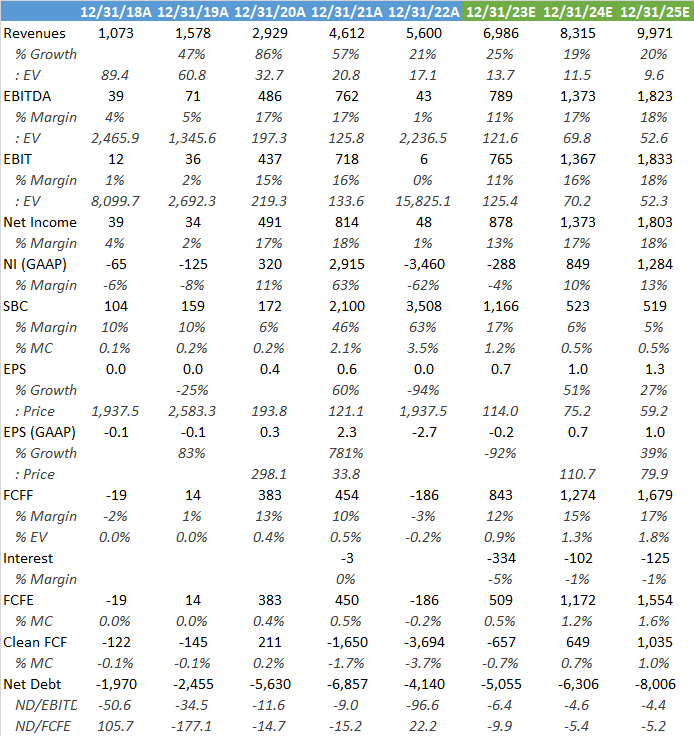

Financials - share price of $77.5 at time of writing, ticker ‘SHOP’ on the NYSE

Shopify has been a very appealing, high-growth story. Although growth has now been somewhat maturing post the covid e-commerce boom. That said, GMV growth is still above 10% which remains attractive. On top of that, the company has additional growth levers such as novel software modules which can be monetized, price increases, additional financial services, and increasing the amount of payments processing.

As a result, Wall Street is looking for around 20% top line growth over the coming years. The business has turned FCF positive with a net cash position of around $4 billion currently, so the financial situation is extremely healthy. That said, valuation looks a bit expensive for me here, even on ‘26 consensus numbers, the FCF yield is still only 1.7% and taking into account SBC, this would fall to 1%. As a positive, operating expenses were down 23% compared to last year, so the company has successfully been cutting costs.

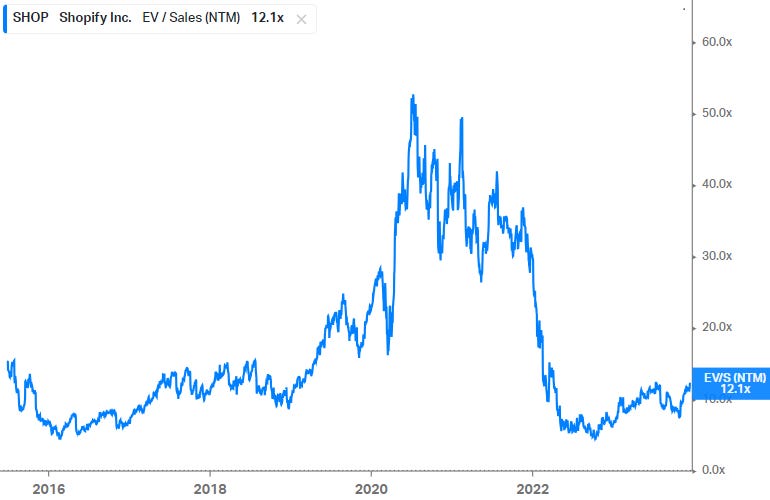

Obviously valuations got quite insane during the covid tech bubble, and even today, 12x forward Sales is high for a business only generating 50% gross margins and where growth is maturing.

Overall, this is an attractive business, but well reflected in valuation. Personally I would stay on the sidelines for the moment to potentially take re-entry on a strong pullback.

If you enjoy research like this, hit the like button and subscribe. Also, please share a link to this post on social media or with colleagues with a positive comment, it will help the publication to grow. All shares are appreciated.

I’m also regularly discussing tech and investments on my Twitter.

Disclaimer - This article is not a recommendation to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it can not be guaranteed that all information used is of this nature. The views expressed in this article may change over time without giving notice. The future performance of the mentioned securities remains uncertain, with both upside as well as downside scenarios possible. Before investing, I recommend speaking to a financial advisor who can take into account your personal risk profile.

Last year, there was a visible slowdown in e-commerce. However, strong businesses remained strong. Recently, I did a write-up on Shoper, also known as the Polish Shopify.

https://activebalance.substack.com/p/refining-e-commerce-with-a-polish

“Personally I would stay on the sidelines for the moment to potentially take re-entry on a strong pullback.” - todays the day