A bird-eye’s view of the payments industry

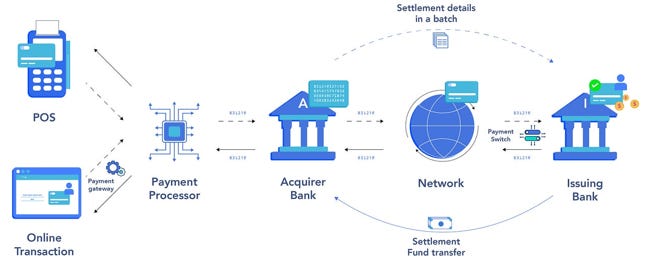

The payment ecosystem has become a rather complicated value chain with the move to digital payments. In prehistoric times, when payments were made in cash, the federal reserve would issue notes which could easily be used in transactions with immediate settlement. In the world of digital payments however, the key problem was knowing whether the buyer actually had the cash available in his bank account. So a payment network was installed which would check if the money was indeed there. Subsequently, the money would be transferred over from the purchaser’s bank account to that of the merchant. As both of these had to be connected to the same network to make this happen, this automatically become a highly consolidated industry with typically only a few number of players per country. The most widely recognized names operating in this space (payment networks) are Visa and Mastercard and are typically seen as the highest quality investments in the payments industry due to their wide moat.

At the point of sale, the merchant acquirer who manages the merchant’s bank account, provides a gateway so that a secure connection from the method of payment to the network can be made. Initially this was a terminal, but later on this would become fully digitized as well with a gateway running in the browser. Classic examples here are the Paypal button and the little form where you can type in your debit/ credit card details.

The overall ecosystem illustrated:

Also merchant acquiring was actually a pretty decent business. Typically you would have a handful of players in a country, and they would make high margins on smaller merchants with a take rate of around 3%, although in emerging markets with higher levels of fraud this can go up to 5%. Large merchants such as a Walmart on the other hand, providing large volumes, would get large discounts.

Some of the more recognizable names in merchant acquiring include Worldpay, Chase, Shift4, and Wirecard,.. but the latter is a story for another day (which goes somewhat like Enron).

An overview of some of the more notable players in each of these niches are presented below:

An introduction to Adyen

The ecosystem above shows that Adyen is active both in acquiring and in gateways. What made them really unique originally is that they have a global platform, running in a single codebase, able to accept the unique payment methods and currencies of around the world, and able to connect with local payment networks. The typical old-school merchant acquiring competitors on the other hand have legacy systems, cobbled together by acquisitions, giving them substantial problems in both cross-border integration and scaling. Worldpay is a notorious example here.

The image beneath highlights all the popular digital payment methods per European market. Adyen, having been born in Amsterdam, has a platform which is exactly designed to deal with this complexity.

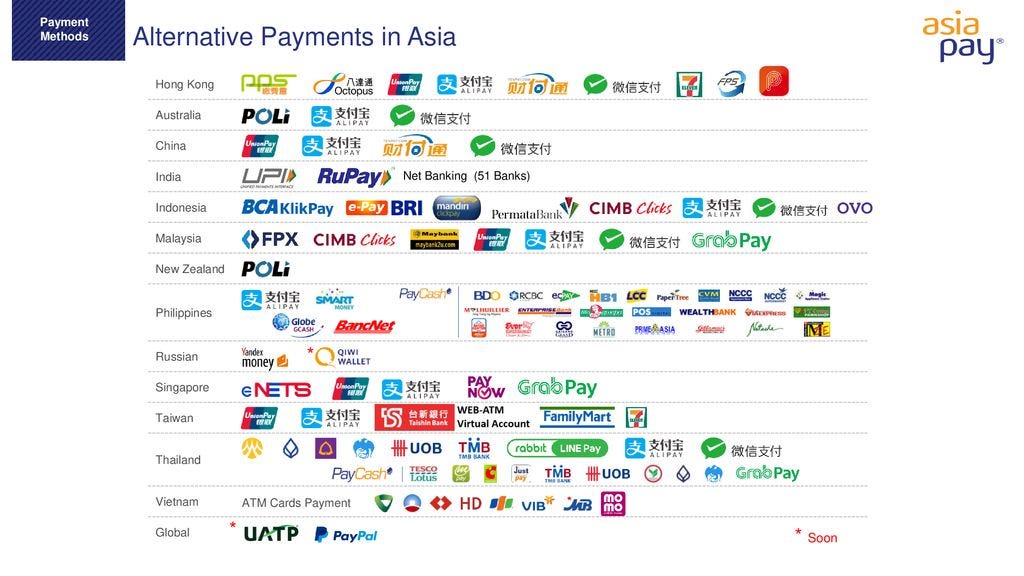

Similarly the Asian fintech scene has seen an explosion of local innovation:

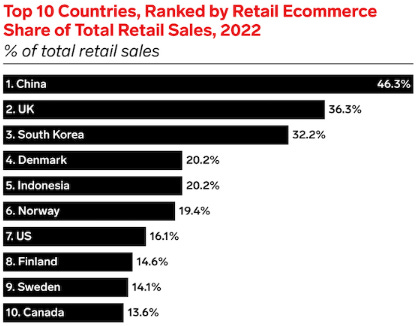

As a result, Adyen’s platform is really ideal for a large multinational enterprise who wants to be in an easy position to collect payments around the world. Its customers include some of the world’s most recognizable brands such as McDonalds, Facebook, Microsoft, Uber, Spotify, Netflix, H&M, Ebay, and Airbnb. The other attraction of Adyen is that you grow with these brands. And you get exposure to the rising penetration of e-commerce in these countries:

This business model has been extremely successful. When looking at the global enterprise e-commerce market, Adyen already has a 20% market share. However, enterprise e-commerce is only 10% of the overall merchant acquiring market, meaning that Adyen only has a 2% market share in the wider merchant acquiring market. This highlights the fragmented and competitive nature of this industry with over 3,000 merchant acquirers competing globally, although mostly only on a local level. The positive here is that there is lots of prospect for consolidation with legacy acquirers being replaced with modernized platforms.

That said, if you only have to provide in-store processing for merchants, typically you just need a regional datacenter which can provide low latencies in accepting payments. It really isn’t that complicated. So I suspect that Adyen will remain oriented towards the larger multinationals for its core business, although they have also started providing software for smaller merchants operating over peer to peer platforms (e.g. Airbnb) to manage their businesses. More on this below.

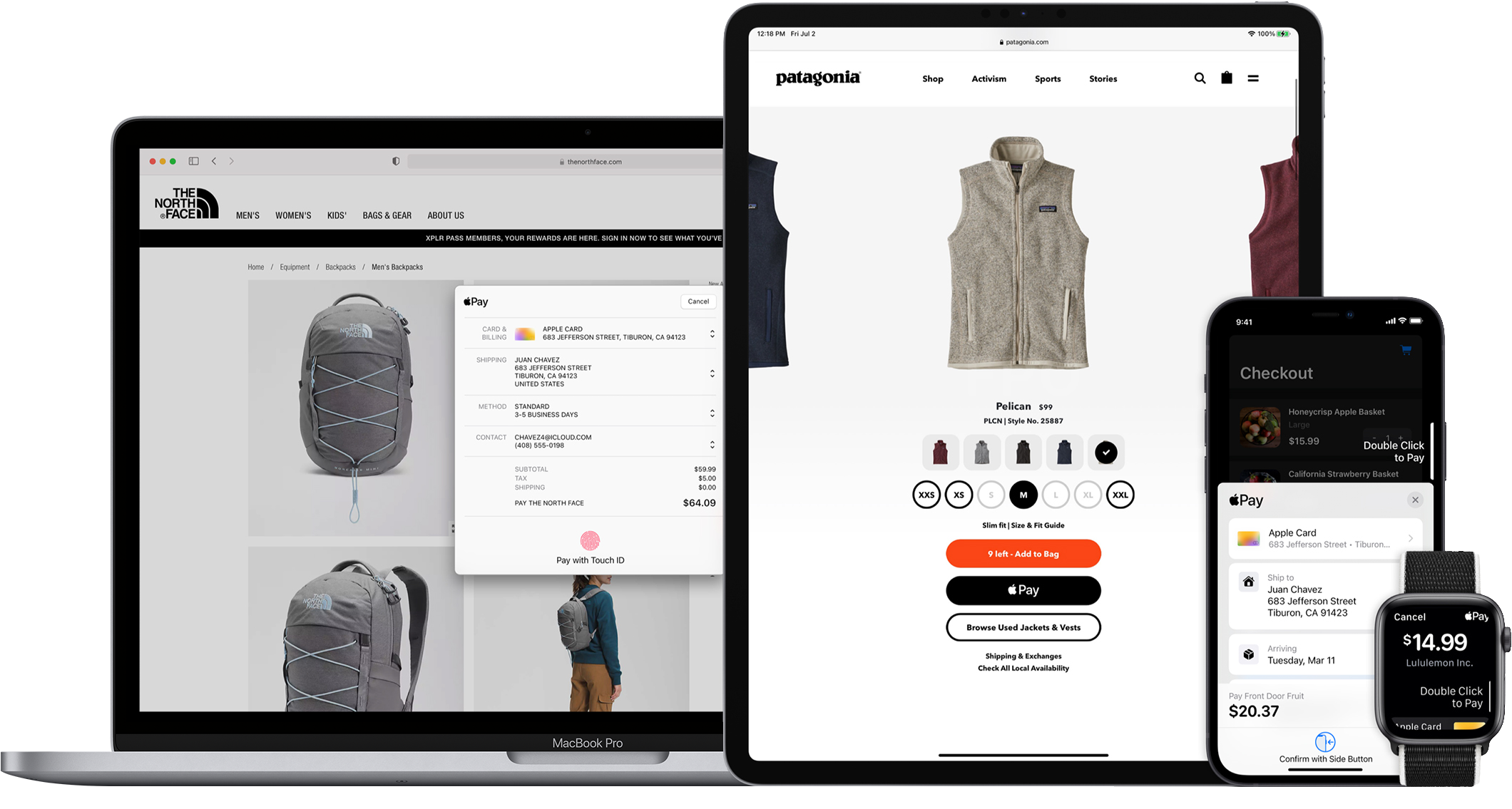

A customer can connect to Adyen’s platform with API calls from their codebase, i.e. within their web app or within their smartphone app. This a simple encrypted JSON-style call which gets transmitted over the internet to Adyen’s datacenters. Within the encrypted JSON message, a secret token will be passed along to verify the customer making the call. Adyen will subsequently take care of the transaction and send a message back that the payment has been accepted, or alternatively that a particular type of error has been found and that the payment can’t be accepted.

A customer can integrate an interface for accepting payments within their (web) app exactly the way he wants. Although Adyen also provides templates which can be inserted into the app and subsequently customized with coding such as CSS. So McDonalds might go for a red looking background with yellow letters in the McDonalds font for example. This level of customization is a big positive for large brands.

The company has also started to provide dashboards, similar to Square or Toast, so that a small merchant on a peer to peer platform can easily keep track of his business. This isn’t really in demand from Adyen’s enterprise customers, as they would access this data from their ERP (e.g. SAP) and analytics (e.g. Snowflake) systems.

Dashboards also provide Adyen with the opportunity to sell additional services, of which the most interesting is BaaS (Banking as a Service). As the platform provider knows the cash-flow profile of each merchant, smaller type loans can easily be made if there is the need for an investment to grow the business. These loans are provided by a financial institution such as a bank, private equity, or an asset manager, and the customer automatically pays these back from the revenues he generates over the subsequent year.

As Adyen also has a banking license in a lot of countries, the peer to peer platform can issue a business banking account to these smaller merchants, including a debit/ credit card. The advantage for the small merchant is a faster receipt of payments, as well as having everything in one platform, from banking to their business dashboards. The attraction for the platform partner is that Adyen is invisible to the customer, so Airbnb for example could leverage Adyen’s tech and banking capabilities, but branding everything under their own logo.

Adyen’s CEO discussed the opportunity in platforms at the Goldman conference: “We did some research where we see that about one-third of SMBs get payments from platforms today, but that will likely go to something like three-fourths of SMBs. So making sure that we have an offering that helps these platform customers is really key for us. And there, we're seeing really strong traction. Excluding Ebay, we grew 82% in the first half on the platform side. That's especially in Europe and the US.”

Adyen’s website gives some further stats: “Our research found that, by offering embedded financial services, platforms could unlock a potential revenue uplift of up to 70%. The market for SMB embedded finance is still at an early stage of development, with less than 5% of penetration.”

Another area where Adyen is investing strongly is omnichannel, which is useful for retailers that both sell from physical stores as well as online. This enables them to track customers across these channels, so that better promotions, services, and more relevant advertising can be offered. If a consumer buys an item online for example, the platform could tell the retailer that this customer lives close to a certain store, allowing for same day delivery.

Adyen’s CEO detailed how a large chain like McDonalds is using them for omnichannel: “If you had basically discussed this like 3, 4 years ago that a fast food chain would work with a processor like ourselves to accept payments, I would have said that likelihood is relatively low because they just need pipes at a counter to process quickly. But now it's completely shifted because it is about consumer insight. It is about how making sure that no matter if you pay in the app or at a counter that you have to write the information. So it opens up a lot of new verticals, and that's what we're focusing on right now. The unified commerce opportunity is huge. We're ahead of competition, like there's no global player that can offer this in a single platform.”

Adyen’s founding & engineering ethos

Adyen stands for ‘start again’ in the language of Suriname, a reference to the fact that this was the founders’ second payments company. The first, Bibit, was sold to Worldpay in 2004 (as I told you, a company cobbled together by acquisitions). After this first experience in the industry, the founders had learned about all the problems with legacy systems (having worked two years at Worldpay post acquisition). And they decided that a new, integrated platform would replace these legacy providers. They got to work in their Amsterdam apartment.

Pieter van der Does, Adyen’s co-founder in an interview with Techleap detailed the company’s background, history, and culture: “When we sold Bibit to Worldpay, we had so many lessons learned. And when we sold the company, we didn't think we would go back into payments. But 2 years later, we regrouped and thought of starting a company again. We started a company called Adyen. At that time there were so many fragmented solutions. Our idea was to build in-house something that connects directly to the endpoint of payment and does not make a patchwork of systems. We believed that if you could make this product of the highest quality possible, then you’d be able to sell it to the best companies in the market. So we had a very unusual market entry strategy and a very ambitious plan - we know this market, we're going to build something that outperforms and we directly target the high-end.

Our first sizable merchant was in 2011, and we started in 2006. That took us 5 years. One of the difficult things to overcome at the beginning of your journey is that you need volume in payment. Breaking through that problem is what took us time. And then a few years after 2011, we started to build a point of sale because we thought it's great to provide payments for internet companies. We also saw that a lot of internet companies, such as CoolBlue, moved to physical stores, which was unexpected at that time. While we felt that the infrastructure we built actually worked really well for physical stores, it was particularly excellent for companies that had both online and offline presence.

We have turned down many offers along the way from the very first days when we were founded. Already then we got an offer to stop doing what we do and be acquired as a team. So along the way, on the road to IPO, we got many offers, frankly. And it’s not always easy to turn them down with your shareholders. After selling Bibit, I stayed in the company for another two years, and as a result I had to run it under the umbrella of a larger company that made all sorts of decisions that I wouldn't personally make.

This is how we approached our first investment round with the first big VC: we don’t want to give board seats because we are building a large company. And if you build a large company, you know that at a certain point you will need an independent board. So we didn’t want to give anything other than common shares.

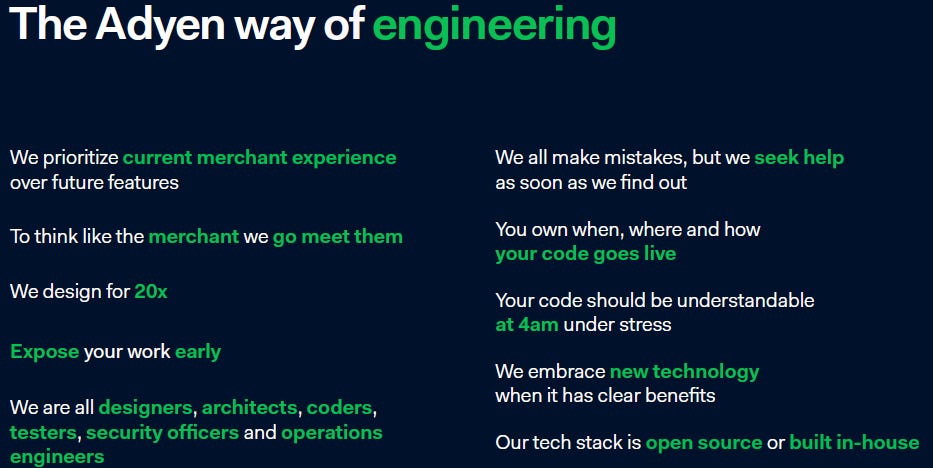

With Adyen we have a great preference for simplicity. Because if it’s simple, it’s easier for us to control it. So therefore we never made an acquisition. We only run one system. We only have engineers that are educated in the languages we use within the company. The board still oversees every hire, regardless of the role. You cannot be hired at Adyen without speaking to one of the six board members. The reason we do it is to put the bar high to ensure that only the best talent joins Adyen.”

The ethos which Adyen’s founders have been installing in the company:

Thoughts on Adyen’s H1, Paypal, and the competitive payments landscape

So after this long introduction, even if you’re new to the payments industry, you should have enough background now to understand the variety of problems which I’m about to go into. Theoretically, Adyen’s story should be of interest to investors, i.e. a platform which currently has a competitive advantage and with a long runway for growth, both as they replace legacy systems and and as they grow together with the rise of e-commerce. As the company’s cost base grows more slowly, we should get great operating leverage in terms of earnings growth. And obviously, this is an extremely well-managed business, designed with simplicity and low-cost in mind, with the whole platform running from one codebase. Which has translated into strong margins.

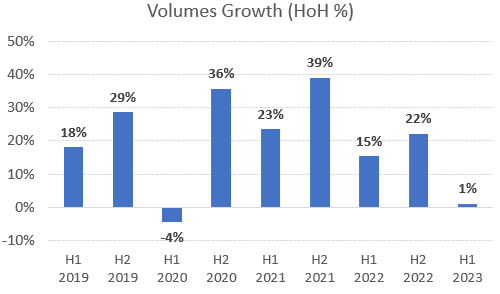

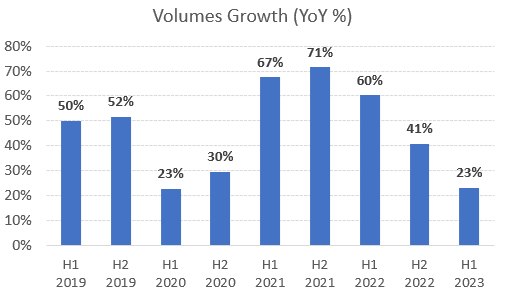

However, at Adyen’s recent half year results, sequential volume growth (transactions processed) came in at a measly 1%:

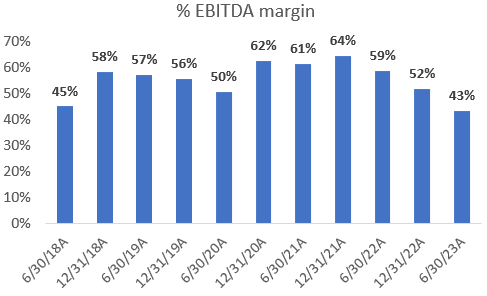

On top of that the company’s margins took a nosedive coming in at 43%, a historic low:

The billion dollar question is what’s going on here, are we looking at a temporary blip or has the company started struggling with more structural and competitive pressures?

Well, the results aren’t as bad as implied in the two charts above. The first half of the year is the seasonally weaker half, as it doesn’t include the Christmas holidays shopping period and the summer vacation spending. Looking at revenue growth on a year over year basis, the easiest method of stripping out seasonality, we still saw 23% revenue growth. Although this was far below what the market was expecting and still a historic low.

On the margin side, the company is guiding that this will be a year of headcount increases, to drive the R&D in peer to peer platforms and omnichannel, after which headcount growth can be slowed down again. So we’re currently in an investment phase which should drive accelerated revenue growth and operating leverage in the coming years.

The pressure point for the weak result seems to come from the competitive environment in the US e-commerce market, which Adyen has been targeting for growth. Adyen originally grew in the European e-commerce market, where due to a plethora of localized payment methods and currencies, the company had an obvious competitive advantage. In the US on the other hand, payment methods are much more limited. If you’re able to accept Visa, Mastercard, American Express, Paypal, Google Pay, and Apple Pay, you’re probably in a position to accept payments from almost any consumer. And authorization rates will be extremely high already. Adyen due to their strong localized know-how will be able to increase authorization rates in emerging markets for example, but this advantage isn’t a factor in the US. This results in the US being a much more competitive market, with more processors being able to compete as well as the legacy players.

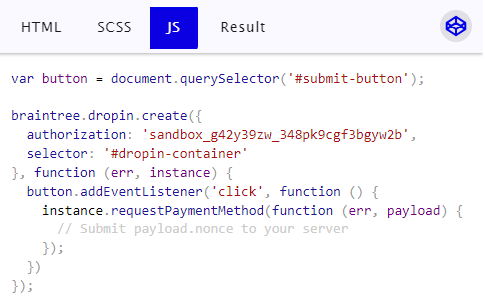

The competitor which is frequently being cited as competing aggressively with Adyen on price is Paypal’s Braintree. Braintree is a gateway and acquirer similar to Adyen which can easily be integrated into a website and app. Similar to Adyen, this is a gateway targeted at mid to large corporations who like to customize their payment experience. The below image highlights how you can insert some Braintree-provided Javascript into your code, which will provide you with a nice widget which you can customize to fit your digital store.

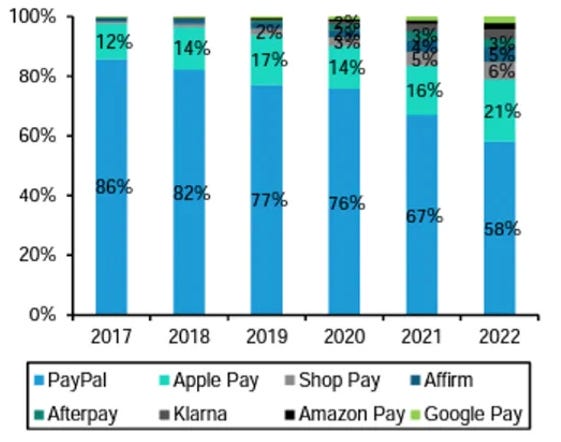

A contributor to Paypal’s aggressive stance in the Braintree business is that their famous checkout button has come under pressure. Bernstein calculates the following share losses in the US, with especially Apple Pay gaining share but also Shopify with Shop Pay and buy-now-pay-later (BNPL) providers such as Affirm.

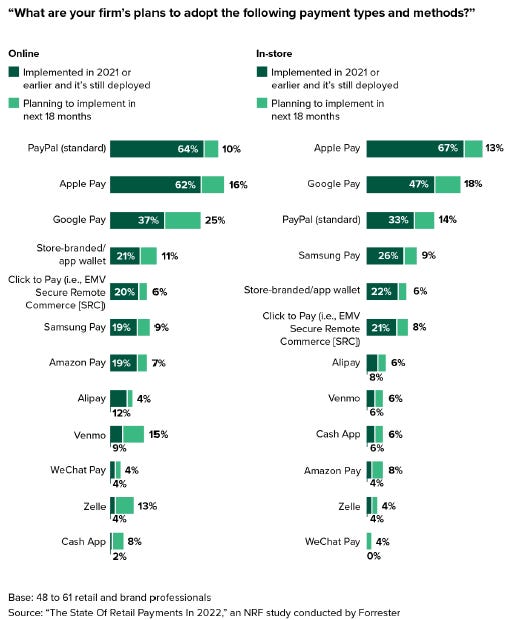

And the pain isn’t over. According to a study by Forrester for NRF’s state of retail payments in the US in 2022, Paypal is still leading when it comes to online payments, however, more are planning to offer Apple Pay within 18 months. This would give the latter the lead. Clearly also Google Pay has strong momentum, including those retailers that are saying they will adopt it, this would make the gateway’s acceptance rate jump from 37% to 62%. Both of Apple Pay and Google Pay lead in in-store payments with Paypal only coming in third.

You might think that Apple is only 50% of handsets in the US, so that they will only be able to capture 50% of the payments market. Well, iPhone users are twice as affluent on average, making them two-thirds to three-quarters of consumer spending. That’s a big chunk of the market which Apple Pay could grab. Naturally Apple is making their payment button pop-up everywhere they can:

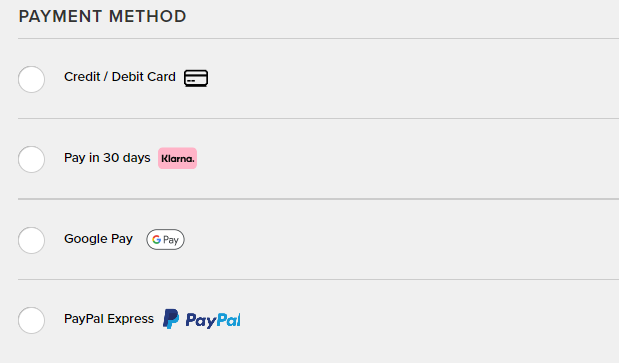

Forrester’s results are sort of in line with what I’m seeing anecdotally living in London. Over the last year, I’ve started seeing the Google Pay button more frequently than Paypal’s when shopping online. And it’s also usually ranked above the one from Paypal, as Google’s take rates are lower. A typical checkout layout I’m coming across these days is highlighted below. In my opinion, the Paypal button has become fairly commoditized..

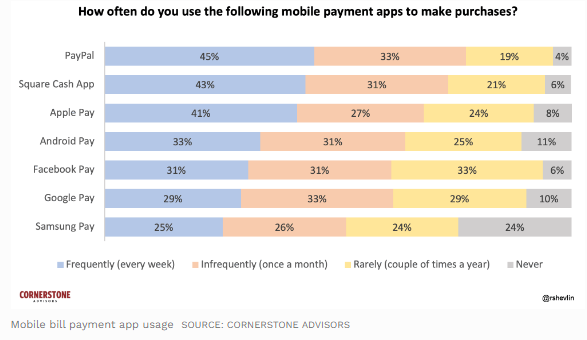

Also when it comes to mobile payment apps, Paypal is facing a competitive environment with respondents in a study from Cornerstone using a wide variety of apps. The positive here is that there is still plenty of room for growth with mostly young people only using these. But the negative is that Paypal is not making any money here, with very low monetization rates.

Going through all this data my suspicion is that Paypal’s take rates will likely be heading (further) south in the coming years, mainly coming from further market share losses in their bread-and-butter Paypal button business. And I guess Paypal’s management is making the same calculation — “If only there’s a way to protect our Paypal button business..”

For premium subscribers, we’ll further dive into:

The competitive battle between Adyen and Braintree

The increased competitive environment Adyen is facing, especially in the US and from startups

Adyen’s biggest problem, payment orchestration platforms

A financial analysis and thoughts on valuation for both Adyen and Paypal