The All-in podcast discussed a viral tweet suggesting that AI data center construction will come to a halt, the key snippets:

“A 5-year backlog on grid transformers just killed half of America's 2026 AI data centers. Sightline Climate tracked 12 GW of 2026 US data center capacity announced across 140 projects. Only 5 GW is actually under construction. 11 GW sits in the "announced" stage with no physical progress despite typical build times of 12-18 months. 25% of those projects haven't disclosed a power strategy at all.

Nvidia is shipping. The gating constraint is high-voltage transformers, switchgear, and grid-tie batteries. Pre-2020 lead time on a high-power transformer was 24-30 months. Today it stretches to 5 years. Electrical equipment is under 10% of total data center cost and 100% of the bottleneck.

The winners under this regime are whoever locked in power purchase agreements and electrical equipment orders 3-4 years ago, before anyone was modeling hundreds of megawatts of inference load. Everyone else is waiting in line behind them. Second order is uglier. Hyperscalers buying $50B of GPUs that sit unpowered depreciate against Nvidia's annual cadence while paying carrying costs on empty data center shells. Every quarter dark is a quarter of compounding waste.”

There are three bottlenecks mentioned—high-voltage transformers, switchgear, and grid-tie batteries. Let’s focus on the HV transformer first, that’s the big one. You need a massive HV transformer when you connect the data center’s power supply to the grid, as transmission lines carry electricity at high voltages over long distances:

So, when you don’t have a HV transformer, the solution is to move behind the meter—i.e., a data center that generates its own power on-site. Local generation can produce electricity at a medium voltage (MV), or even low voltage (LV), avoiding the need for a massive HV transformer.

Fortunately, there are plenty of ways for a data center to generate power on-site. A recent HSBC report on AI bottlenecks discusses the trend to ‘bring your own power’ (BYOP):

“Grid equipment lead times are rising with some shortages in medium voltage equipment, but the key bottleneck is in high voltage substations, where lead times are 3-5 years. This shortage, along with long wait times for grid connection, has driven the rise of the BYOP (bring your own power) model of onsite power generation. Whilst many datacentre developers scrambling for electricity intend to use onsite power for a few years until the grid infrastructure can catch up, a few plan to bypass the grid indefinitely. Demand is rising for off-grid “energy islands” – cutting out the grid, under a colocation model. One project opting to forgo a grid connection is a Meta Platforms datacentre campus near Columbus, Ohio. In July 2025, regulators approved a plan by pipeline company Williams to build onsite natural gas power. Also Oklahoma state lawmakers passed a bill earlier in 2025 to let companies build their own power to take advantage of abundant gas supply.”

The problem with power from natural gas however is that now also gas turbines have massive backlogs. Leading turbine manufacturer GE Vernova for example still has some capacity in ‘29 and ‘30:

“We’re directionally at about 3 years lead time today, we’re sitting in the spring of ‘26 and we do still have capacity in both ‘29 and ‘30. What’s happened in the first quarter is we sold a lot of 2030 slots. We still have about 10 gigawatts remaining cumulatively in ‘29 and ‘30 together. It’s important to contextualize that the 100 gigawatts we have on contract today is with almost 90 distinct customers in 24 different countries. So there’s a need for incremental electrons for many different applications in many different countries, which has us continuing to work hard to figure out how in a very capital-efficient way we meet this moment and serve this market.”

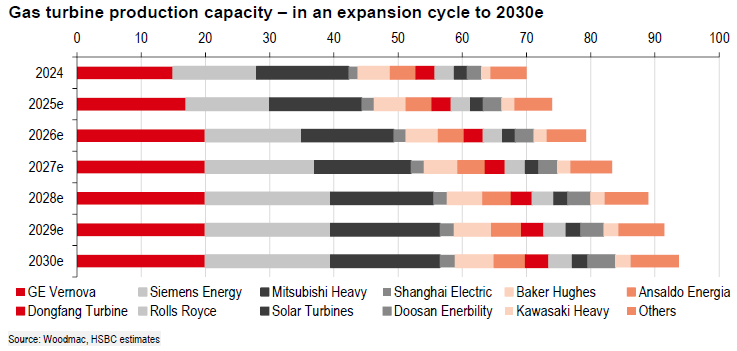

Note the focus on capital efficiency, i.e. GE doesn’t look to be planning to add much manufacturing capacity, further increasing gas turbine shortages. Looking at the HSBC analysis, Siemens and Mitsubishi are planning to add capacity however already as from this year, and overall gas turbine production capacity will rise from 70GW in ‘24 to over 90GW in ‘29:

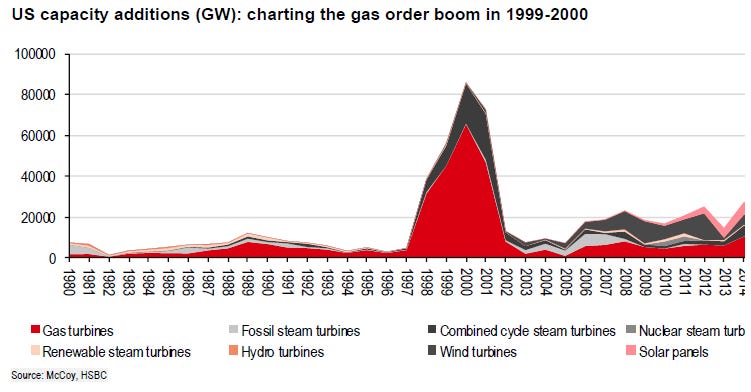

GE is probably reluctant to add capacity in the case that demand pulls back. This is what happened in the early 2000s. There was a boom at the time in orders following US power sector deregulation, after which HSBC notes that ‘key suppliers aggressively expanded capacity but then suffered from low utilisation as orders normalised’:

Besides the long lead times to actually get the gas turbines to a data center, another problem is that gas turbines are loud and cause pollution. Two factors which are especially important for infrastructure near residential areas. Due to these problems, other solutions such as fuel cells are seeing huge order growth. Fuel cells have numerous advantages—they’re clean, don’t make noise, and can output electricity at low voltages directly. This means you don’t need a HV transformer, or even a medium voltage transformer (which steps down MV to LV).

Bloom Energy is the big winner in fuel cells so far and recently saw a massive order from Oracle for up to 2.85GW of power. From Barclays:

“Oracle’s Project Jupiter provides insight into the shift by hyperscalers. Into the print, our channel checks did suggest that there were some turbine orders being canceled/slots being sold with customers switching to Bloom, but we weren’t sure if it was a one-off or an indication of something broader. On the call, BE confirmed that ORCL’s Project Jupiter pivoted from a conventional plan (gas turbines plus diesel backup) to a 100% Bloom, fully islanded microgrid - no grid interconnect, no diesel, no turbines, no batteries. Management emphasized that BE was selected not only due to its speed to power, but also because it is clean and community acceptance (air quality, water usage, noise pollution).

While investors tend to compare the capex cost of BE’s option to CCGT alternatives, this update would underscore that this may be an “apples to oranges” comparison like management stated on the call, as there are attributes and advantages to using BE’s fuel cells that may not be as easily quantifiable. This is especially the case when adding in the benefits of its native 800V DC fuel cells and considering the NIMBY attitude that we are starting to see regarding data centers. As more than half of current data center backlog is now comprised of non-ORCL hyperscalers, neo-clouds, and colo providers, this would also suggest this is not a one-off situation, but more reflective of a broader trend. We would expect future ORCL projects to also find their way into the backlog, solidifying the re-rate higher we have seen in recent weeks.”

Bloom’s Solid Oxide Fuel Cell (SOFC) can be supplied with either natural gas or hydrogen, and the technology is proven—the company already has 1.5GW of capacity installed globally. Another benefit is that you don’t need backup batteries to power your data center, or dirty diesel engines. While Chinese battery manufacturers are stepping up capacity—and we didn’t come across shortages in this area—batteries aren’t necessary to power AI data centers anyways.

Additionally, Bloom has been talking on their call how they can easily scale capacity to meet demand. Recent highlights from the call:

“The marketplace is recognizing and embracing our proposition of clean, reliable on-site power that is community-friendly and deployed at the speed of AI. Bloom is rapidly becoming the standard and go-to choice for on-site power. Last night, Oracle announced a new power paradigm for Project Jupiter, a multi-gigawatt AI factory to be built in New Mexico. We are thrilled to partner with Oracle and applaud them for their visionary leadership. This up to 2.85 gigawatt power block will replace Project Jupiter’s previously planned gas turbines and backup diesel generators with Bloom Energy Servers. It will be 100% Bloom. When completed, it will be one of the largest islanded microgrid power facilities in the world.

At a time where every quarter of delay translates into hundreds of millions in foregone AI revenue and loss of competitive advantage, speed of powered infrastructure development is the difference between leading and following. It’s not going to be a one-off project. Where Oracle is going is where the broader market is headed. More than half of our current data center backlog comes from other hyperscalers, neoclouds and colocation providers. Just like the Oracle Jupiter project, these microgrid installations will use no grid, no dirty diesel generators for backup, no battery banks for load following, no engines, no turbines, just Bloom.

Time to power has gone from a procurement consideration to an existential necessity. The companies driving the AI transformation are racing against each other and bumping into bottlenecks such as permissions, permits and community acceptance. The winner will be the one who can grow and deploy faster. The legacy power industry’s model is long-cycle times and capital-heavy capacity additions. Our model is different at every layer. We innovate and improve continuously—in our technology, how we manufacture, in our capital intensity, how we deploy. That is what allows us to deliver double-digit cost reductions year after year, expand capacity with materially less capital than industrial-era players, and meet our customers’ schedule. We are adding lines and expanding capacity to meet growing demand, and innovating to reduce cycle times, space needs and costs.

Our competitors’ supply to current orders arrives only in 2029 or later, our supply arrives this year or the next, whenever the customer is ready. Based on the demand profile, we have now shifted to adding capacity continuously, hundreds of megawatts a quarter as opposed to lumpy one-off additions. The traditional power industry has spent the past 2 years celebrating its backlog that is 4 and 5 years out. Our ability to expand capacity is our competitive advantage.

Our current manufacturing footprint will allow us to deliver 5 gigawatts of product annually. We will expand that capacity and meet the delivery dates needed by our customers. Today, we are not capacity-constrained. The pace of our revenue growth is decided by how fast our customers can build their greenfield sites, not how fast we can power them. Going beyond the 5 gigawatt capacity, our supply chain and manufacturing strategy allows us to build that capacity significantly faster than any other option in the market using our copy exact model.

We have a 100% attach rate between our product sales and our service. Even with the data center opportunities, on average, it’s 10 to 15 years of servicing, and so it’s a tremendous source of annuity revenue that we see.

Communities care deeply about what kind of infrastructure shows up next door. Bloom preserves local air quality. We do not combust and pollute the air like conventional technologies. We use minimal water at startup and none during normal operations. We are quiet, compact and efficient with land use. We integrate well with environments rather than disrupt them and become an eyesore. As permits and permissions become the gating factor for AI infrastructure, community acceptance matters increasingly. Our solution does not raise the monthly electricity bill for community residents.”

Goldman notes that fuel cells are actually cheaper than gas turbines when natural gas prices go higher:

“Overall, fuel cells currently have a higher LCOE (Levelized Cost of Energy) than gas turbines - roughly 40% higher than that of simple-cycle gas turbines (at natural gas price of 4$/mmbtu). The cost gap is mainly driven by the high cost of fuel cell systems and limited deployment scale. However, as natural ‐ gas prices increase, the cost gap narrows in favor of fuel cells, because fuel cells consume less gas per unit of electricity. At spot natural‐gas prices of $13.3/MMBtu, our LCOE analysis indicates that fuel cell generation is broadly comparable to, or around 7% lower than, gas turbine based generation. Finally, as manufacturing expands, we expect the LCOE of fuel cells to improve substantially, gradually approaching the competitiveness of advanced gas turbine technologies in the longer term.”

While in the US, natural gas is dirt cheap, in Europe and Asia spot prices are much higher. This will make the economics of fuel cells especially attractive for European and Asian AI data centers.

So, Bloom’s fuel cells solve the bottleneck of transformers, which has gotten a lot of attention. The other bottleneck mentioned is the switchgear. However, listening to the conference call of European industrial giant ABB, additional capacity is now coming online and switchgear shouldn’t be the limiting factor in the AI data center buildout:

“The capacity expansions are now coming online, that money was spent 2 years ago and last year. I don’t think we are the limiting factor when we’re talking about build-out. We know the equipment like gas turbines, large power transformers, is more of a limiting factor than we are on switchgear and the component level. We’re also expanding capacity by appointing new partners, what we call the OEM partners, and the ones who do the system integration on ABB’s behalf.”

While Bloom is bullish on adding capacity, they have a few flagship sites when it comes to manufacturing and assembly. So, when those get to full capacity, it is possible that the company won’t be able to meet demand until new sites are added.

Therefore, besides Bloom, there should be room for other players with other competitive technologies to start capturing orders as well. Next, we will go through two small caps with two different technologies that are also well positioned to start capturing orders to power AI data centers. We see the risk-reward as compelling in one of them—with minimal downside and substantial possible upside. Additionally, we’ll also analyze the valuation for Bloom and the company’s outlook.