Semi investors are accustomed to having to deal with cyclical downturns, and the supply chain for biotech and pharma is currently going through one of the worst in its history. Typically these types of huge cyclical corrections give opportunities to investors to pick up quality companies at beaten down valuations. And the rewards for long term investors are often high—once the cycle recovers, we see strong EPS expansion coupled together with sell side upgrades and also regularly multiple expansion as the outlook continues to improve. The market typically oversells shares during a downturn and overbuys during a strong upcycle—the reason is that a lot of money in the market is heavily short term oriented, looking to outperform in the next three to six months, and so that money is usually positioned where earnings momentum is currently strong. Naturally, this brings opportunities for longer term investors. In this post, we’ll dive into a number of quality companies which we like in the picks-and-shovels biotech space, with the goal of picking up long term multi-baggers.

Looking at the supply chain for the biotech industry, there are a lot of similarities with semiconductors. At the center of the semi supply chain are really the foundries, where chip design houses send their blueprints to have their silicon manufactured. In biotech, these types of fabs are called the CDMOs, or Contract Development and Manufacturing Organizations. Large pharma companies source their biological drugs from the best quality CDMOs, who got their drugs through the trials, making it hard for new entrants to take share. Just like in semis, there can be a mix between in-house and outsourced manufacturing. For in-house manufacturing, the pharma company produces 30% or so of its needed volumes in-house, mainly for risk diversification and to get some leverage in pricing negotiations. For outsourced manufacturing, Lonza is typically regarded as the highest quality player with the best product and reputation. A sort of mini-TSMC of the biotech industry.

Manufacturing plants have to be filled with manufacturing equipment. In the case of semis, we have blue chip names such as ASML, Applied Materials, and Tokyo Electron supplying the most advanced equipment to the foundries. Similarly for bioprocessing, this is a fairly consolidated industry with Danaher, Thermo Fisher, Sartorius, Merck (the European one) and Repligen being the highest quality providers. An attractive difference with semicap is that bioprocessing suppliers have a much larger exposure to recurring revenues, as they sell a lot of continuously needed consumables for the manufacturing process. For example, Danaher estimates that more than 80% of their bioprocessing business comes from recurring revenues. For semicap on the other hand this is typically only around 20 to 25% of revenues, increasing the cyclicality of the business.

In semi land, ASIC designers have to get silicon developed for customers—they design the chip blueprints, get the tape-outs at TSMC, and then schedule the wafers and packaging at TSMC. In biotech, CROs (contract research organizations) have to get the new drugs through the development pipeline. They provide specialized services ranging from drug discovery to running clinical trials and getting ultimately the regulatory approval. A former executive at Icon, one of the leading CROs, describes the harsh landscape the biotech supply chain currently is facing:

“The reality is that pharma is cautious right now. They are being extremely methodical around spending, and that's both on development and even where manufacturing will be. In my 30-year history in this sector, outside of some of the patent cliff-related issues that you saw in the early 2000s, this is probably the most tumultuous time within pharma, and specifically within R&D. Traditionally, you have seen pharma growth being at around 4% or 5%, with biotech being anywhere between 8% and 11% and large pharma being around 3% and 4%. There have been outlooks earlier this year and last year that that would continue. If you talk to most leaders, we'll see no more than 2%-3% growth in pharma R&D, and there is some question as to whether or not it will be flat for 2025 and 2026. You've seen most of the CROs earlier in the year saying that pharma is going through reprioritization, but that the back half of the year is looking optimistic; most have now adjusted that thinking. The cancellations that are happening are really tough for the CROs. Primarily the mid-sized pharma and biotech, they're awarding work that is sitting on the CRO's backlog, but they're not starting. They're delaying for two quarters to see how things work out around the tariffs and other things. That's what's creating these large cancellations.

The other thing I can tell you is that near term, it is a knife fight out there. I have never seen such repricing negotiations. In the COVID days, CROs couldn't get enough staff, and so you charge a premium. Now, you can find staff left and center. It is a rough business development, you have the large CROs that are knife fighting and you've got the mid CROs that are undercutting. Pharma and biotech know it, they can get multiple bids. They can go back three or four times on pricing. So it's rough, there's just not enough work out there. The question you should really be asking yourselves is, as pharma prepares for budgets for 2026—which we will start to hear about in the August, September time period—will it be the same spend as previous years, or are they going to cut back? I don't think anyone has a great answer on that right now, there are too many unknowns. A couple of things have to get sorted out to have pharma feeling as though the return is going to be there. They're going to continue with R&D spend, but they're certainly going to be more thoughtful about which therapeutic areas and which products.

I don't see how pharma is going to make up some of these patent LOEs (loss of exclusivity). The replacement of new products is not happening fast enough to replace major things that are happening in the market. Steve's comments on the call were like, "Pharma can't restructure its way out of this. They'll have to grow, they'll have to come back and develop at some point." I think Steve is right, once the IRA issue will be sorted, the tariff issue will be well understood, pharma's smart, they're going to figure it out. That will happen, and the only way to do that is they're going to have to do more investments. That's the reality. I think that gives organizations like the IQVIAs and the ICONs the ability to offer through the continuum of FSP (functional service provider) to FSO (full service outsourcing) solutions, which is very much needed.”

We do suspect that current cancellations and reductions in drug development investment were due to macro fears that became widespread following President Trump’s tariff announcement. Markets sold down heavily in early April, after which a macro downturn became the consensus view of most market pundits. However, since then, markets have been rallying sharply over the last three months, which is generally good for business confidence. Thus, after a weak Q2 for some of the picks-and-shovels names in biotech, especially those heavily exposed to new drug development, the outlook should be much better already heading into Q3. A lot of those projects which got cancelled in April-May could already be coming back in the coming months.

The bioprocessing names have high exposure to drug manufacturing and thus less cyclical consumables revenues, although Goldman is also more bullish on future equipment orders after hosting Sartorius at their conference:

“Sartorius stated that after 2 strong quarters of order intake and sales progression, the bioprocessing recovery is clear in consumables, with a recovery being seen in all geographic regions. The company highlighted that this consumables recovery is driven by real underlying demand post the destocking period with no extraordinary or one-off impacts they can see (i.e. no pull forward of orders). On equipment, the company noted the demand picture remains muted, however, the increase in consumables is indicative that the equipment installed base is being utilised more. This should eventually lead to more equipment orders down the line (as capacity utilisation increases across the industry) however the timing of equipment orders picking up again is uncertain. Sartorius noted while equipment spend is always more volatile than consumables, the company does not see any seasonality or cyclicality in equipment CapEx other than the Covid-19 impact.

Sartorius highlighted after an exceptional period of orderbook dynamics during Covid-19, the order intake is now becoming a good forward indicator of revenues again (emphasizing the importance of looking at order intake on a 12 month rolling average basis given the relative volatility). Sartorius stated the split of recurring/non-recurring revenues is 80:20 and the recurring revenue portion does come at a higher margin. With recurring revenues slightly elevated and growing faster than nonrecurring revenues (previous split was 75:25), Sartorius noted there will be a mix effect, but the main profitability driver is volume growth.

The company noted despite the numerous headlines and general sentiment on R&D budgets and spend, there is still strong innovation and new therapies that will eventually drive manufacturing volumes, especially if the new modalities or therapies require more advanced tech processes where Sartorius can add value. The company noted funding constraints would result in a refocus and optimisation of industry pipelines on the most promising assets which could even have a positive effect on manufacturing volumes and so does not expect any potential ‘air pocket’ down the line. Sartorius highlighted in clinical stages, single use penetration is very high, however penetration in commercial manufacturing is only c.10-20%. Going forward Sartorius expects single use to outpace stainless steel in the commercial setting with a key driver of this including (1) better cost modelling for single use vs stainless steel, (2) better yields from processes meaning single use starts to become more economical.

Sartorius noted while the cell and gene market is relatively young, it is important for the company to entrench early to be a relevant player later. The company highlighted their very strong footprint with roughly half of every drug in the gene therapy pipeline using Polyplus transfection technology. The company stated M&A is still a big part of their strategy and their focus is to acquire important technologies the company needs to effectively compete and take market share in bioprocessing.

Sartorius highlighted China experienced more pronounced overcapacity compared to other regions with the region still experiencing weakness. While Sartorius was impacted by local competition during COVID (for less technologically advanced products), the company noted in the past year some customers are reshifting some orders back to Sartorius, and innovation will help the company compete with local players.”

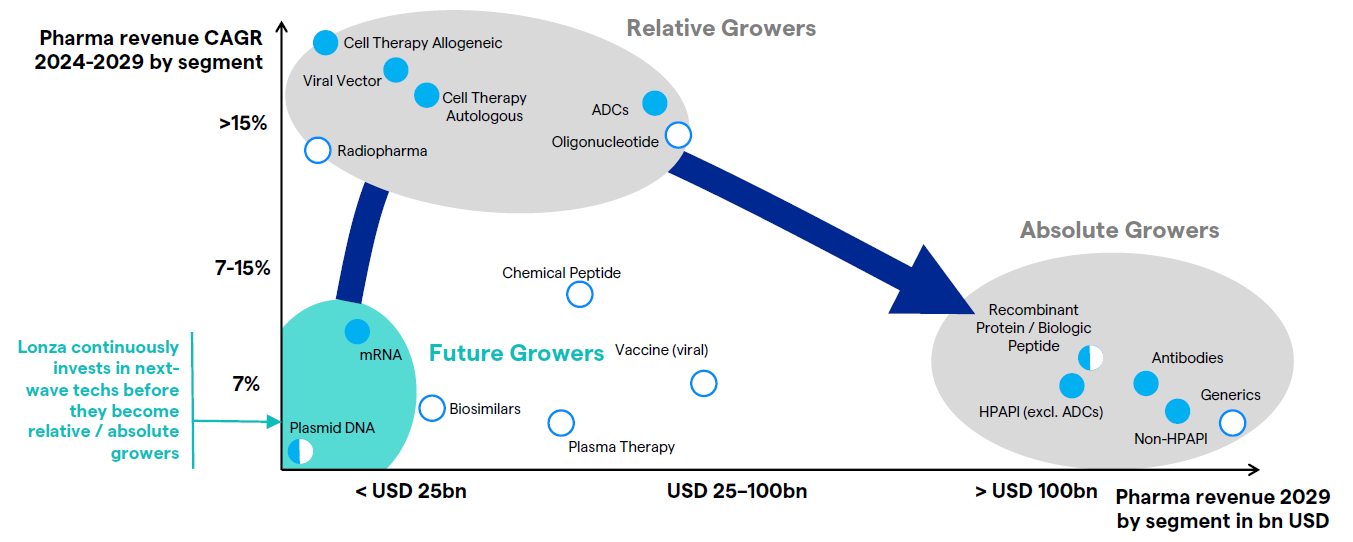

While we think that AI will be the largest opportunity in the market for investors in the coming 5-10 years, it’s worth keeping an eye on the biotech space as there similarly is a high pace of innovation with truly revolutionary technologies, especially in genetic editing. The leading player in the CDMO space, Lonza, illustrates how certain types of therapies are expected to grow at high teens CAGRs and potentially above:

Thus, we see the biotech supply chain as an interesting ground for long term stock pickers. Similar to how dominant providers in the semi supply chain were able to reap the rewards from the massive growth in chips—examples include TSMC, Cadence, ASML, Arm etc. Long term, demand in the biotech supply chain should be attractive—we have an aging population in all developed countries, combined with plenty of innovation potential across the supply chain. Sartorius is a good example here. The company was the pioneer in single-use bioreactors, which make use of disposable bags, so that you don’t have to clean out anymore a steel bioreactor with high precision. This is obviously difficult and costly, as it has to be perfectly clean to prevent contamination in the next manufacturing batch. So, Sartorius is seen as the strongest player in upstream bioprocessing technologies.

To add some further background, in bioprocessing, cells are grown in upstream bioreactors where they then produce the needed biological therapeutic molecules such as proteins, mRNA, viral vectors etc. The simplest method to understand is fermentation. Here you grow genetically modified bacteria, or other cells, in a bioreactor, then feed them sugar and other nutrients, so that they produce the biological molecules you've edited their DNA for. Thus, thanks to genetic editing, we can put sugar into the bioreactor and bio-molecules come out. Subsequently, you purify and filter these molecules out of this soup and voila, you have the active pharmaceutical ingredient (API).

For premium subscribers, we will dive into three smaller names in the biotech supply chain, where we see the outlook as attractive given accommodative valuations, a strong market positioning, and the potential to grow at attractive top line CAGRs long term.