Outlook in Leading Edge Semis: ASML, TSMC, and Cadence

A tour of current developments in advanced semis

In this note we’ll do an in-depth analysis of current developments in leading edge semis, and in particular ASML, TSMC and Cadence. Let’s start off with ASML..

ASML, at the bottom of the growth cycle

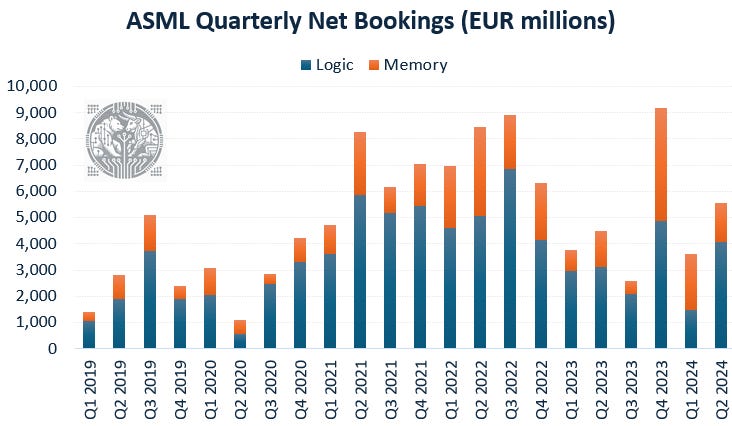

ASML’s orders came it at EUR 5.6 billion for Q2 which is a decent number, currently lead times are still over twelve months so these will only start showing up in revenues around Q2 - Q3 of next year.

Q2 orders were mainly driven by Logic, with Memory falling back again. Over the past two quarters, Memory orders have been fairly strong as the leading DRAM players are gearing up HBM production to meet the increased demand from data center GPUs. However, this time we’re seeing a starting strength in Logic orders with the leading edge foundries preparing for the battle at 2nm, where we will see four players compete — TSMC, Samsung, Intel and Japanese newcomer Rapidus.

The latter’s strategy is mainly focused on attracting orders from smaller semi designers such Jim Keller’s Tenstorrent. Also, given that leading edge customers such as Google and Qualcomm seem to be shifting orders at 3nm from Samsung to TSMC, it’s looking like TSMC’s dominant market share in advanced semi manufacturing will even increase.

For those hoping for a comeback from Intel, keep in mind that the company remains a key competitor for most of its potential clients, i.e. Nvidia, AMD, Qualcomm, Marvell and Broadcom, making it much less likely that these leading edge shops will share their blueprints with a core adversary. If US-based manufacturing would be a key criteria for them in allocating orders, it is more likely that they will tap TSMC to further build out its fab hub currently under construction in Arizona. Nvidia’s Jensen Huang recently even suggested that TSMC should raise its pricing, as they are so valuable to the ecosystem — this doesn’t sound like a customer who is about to switch. Also AMD has so far been stating to have no interest of working with Intel as their foundry.

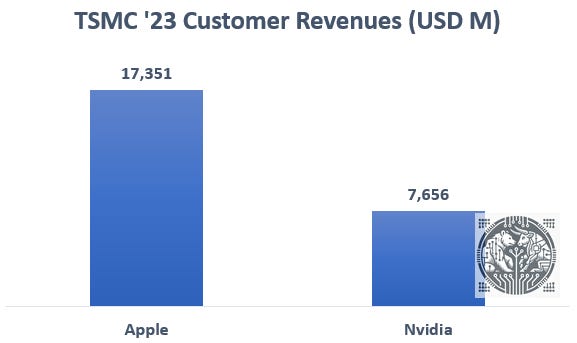

Remember also that these designers have decades long relationships with TSMC, who has always delivered, while Intel has been stumbling and on top of that remains a competitor. TSMC’s goals on the other hand are fully aligned with their customers, whereas Intel’s goals ultimately are to disrupt their customers’ strongholds, i.e. Nvidia in datacenter GPUs, AMD in datacenter CPUs, and Broadcom in datacenter networking. Therefore, the most likely customers who could potentially make the shift to Intel at some stage are the hyperscalers with their custom silicon, such as Google, Amazon, Microsoft and Meta, and also smartphone giant Apple, which remains TSMC’s largest customer contributing around 23% to revenues:

As manufacturing process steps and installed wafer capacity increase at 2nm, this has led ASML and other semicap players to be bullish on ‘25 shipments, bringing in a new growth cycle. Dutch cousin ASM International — which is more focused on atomic layer deposition and which will see higher insertion at the coming nodes — is seeing already a stronger momentum again, with quarterly orders coming in close to peak numbers generated over the covid semi boom:

This is ASML’s new CEO Fouquet on the near and long term outlooks:

“We see today improvements in litho tool utilization levels at both Logic and Memory customers. While there are still uncertainties in the market, primarily driven by the macro environment, we expect a continued industry recovery in the second half of 2024. We currently see strong development in artificial intelligence driving most of the industry recovery and growth ahead of other market segments. Based on discussions with our customers and supported by our strong backlog, we currently expect 2025 to be a strong year and the industry expects to be in a cyclical upturn in that year. As a result, we need to prepare for a number of new fabs that are being built today across the globe. Those fabs will be spread geographically and are strategic for all our customers, and they all scheduled to take our systems.

Logic customers continue to digest the significant capacity additions made over the past year. With this digestion, we see lower revenue from Logic this year relative to last year. In Memory, demand is primarily driven by DRAM technology node transitions in support of advanced memories such as DDR5 and HBM. In support of this transition, we expect growth in revenue from Memory this year relative to 2023. For our installed base business, we continue to expect a similar level of revenue compared to last year.”

This is the ASML’s CFO on the coming expected order flow:

“If you look at the orders that came in, it is a healthy start for the N2 foundry business. It's also clear that obviously, not the full capacity that you would need for this node is in there, but that is pretty logical, this customer is going to ramp and then you will see a gradual buildup with at some stage additional orders coming in for that ramp. The foundry customer has indicated that they're looking at N2 in the second half of 2025 and typically for this customer you’re looking at a lead time of around a year.”

So the CFO is basically guiding here for Logic orders to pick up in the second half of the year as TSMC will start ramping its N2 node one year later.

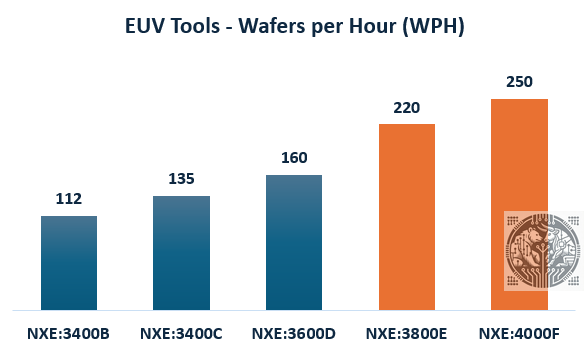

ASML continues to increase the productivity of its EUV tool, its latest model now is the 3800. While these tools will start shipping in the second half of the year, these won’t be at full productivity levels of 220 wafers per hour yet, so these will have to be upgraded later in the field. However, as this gets implemented next year, more revenues will get recognized as higher productivity tools come in at higher ASPs.

This is Fouquet updating the market on the latest 3800 tool:

“We have seen very big progress there. We have measured 195 wafers per hour on the tool and we expect to see the final specification being measured in the coming weeks.”

So it sounds like they are close to getting over the final hurdles of getting the productivity up to 220 wafers per hour. Typically this involves improving a number of components which can either boost processing speeds or alternatively, reduce downtimes. Both of these will improve the overall productivity of the tool.

And after the 3800, looking at the material produced by ASML’s scientists, we’ll get the EUV 4000 tool which will run at 250 wafers per hour:

As a result, ASML will increase the ASP of its EUV tool from around EUR 175 million to north of EUR 200 million. Clients are happy as their overall manufacturing costs decrease due to the higher productivity of the latest EUV tool, and ASML is happy as more revenues are flowing in.

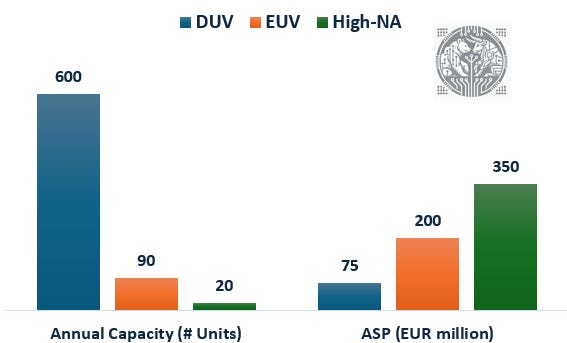

The below chart illustrates ASML’s near term manufacturing capacity per tool, and the ASPs:

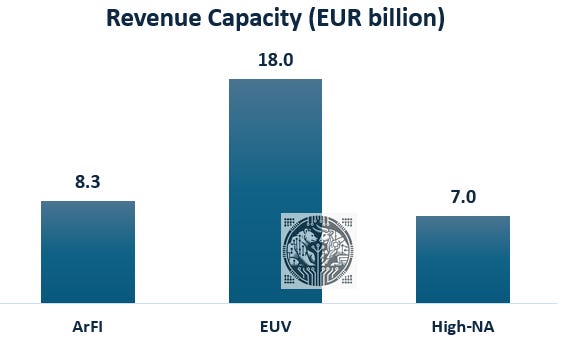

From this we can work out what ASML’s annual revenue potential is from each tool (i.e. capacity times ASP):

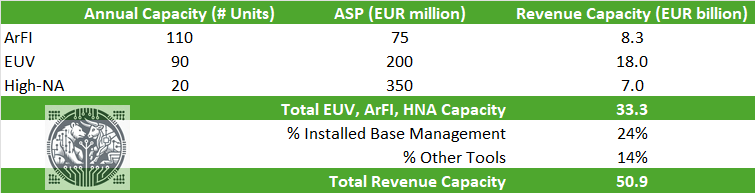

Assuming a revenue contribution of 24% from installed base management, and 14% from the company’s various other tools, this leads ASML already to have a EUR 51 billion annual revenue capacity near term:

So ASML’s EUV capacity is already running ahead of its 2030 high-demand scenario, which we’ll take into account when we get to valuation later on.

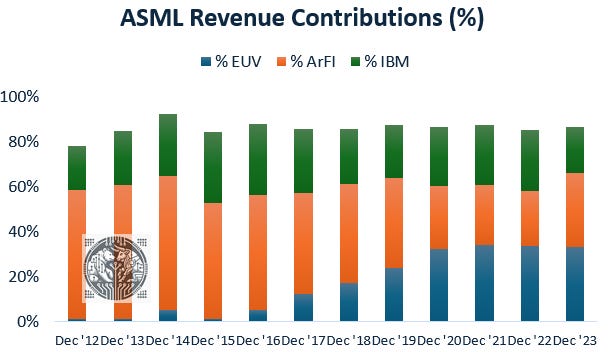

Whereas currently there is more of an even split between revenue contributions from EUV and immersion (ArFI), going forward the above means that revenues will become more heavily EUV-weighted.

This is what ASML’s revenue mix looks like in absolute numbers:

For premium subscribers:

We’ll go through the recent semi sell-off and discuss the potential risks for ASML, TSMC and Cadence.

We’ll discuss in-depth current developments for all three companies, as well as other topics in leading edge semis.

We’ll address the current bear case on AI demand which is doing the rounds, and we’ll have a look what the AI capex environment in the coming years is likely going to look like.

We’ll do a detailed analysis of the financials for all three companies and discuss whether it makes sense to enter or add to the shares here at current valuation levels.

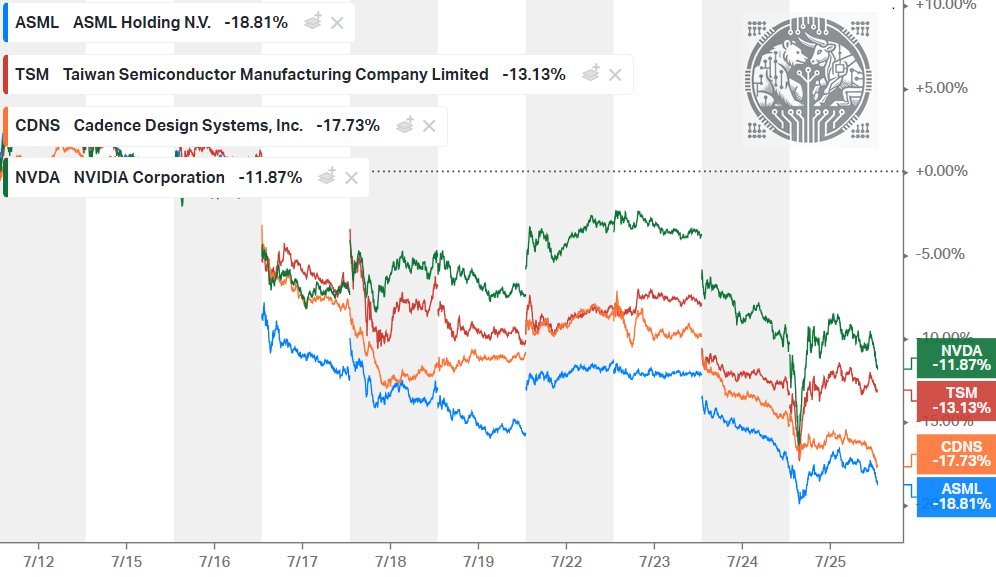

The semi sell off & ASML’s China risk

Semi names sold off sharply on the news that the Biden administration could introduce further measures to limit China’s access to advanced technology. And shares have been trending down since, also as market concerns around the sustainability of AI demand have been on the rise.