The outlook in the cloud & hyperscaling

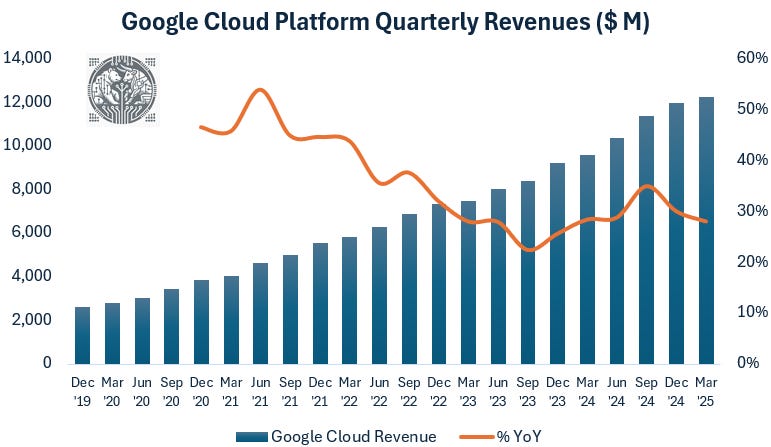

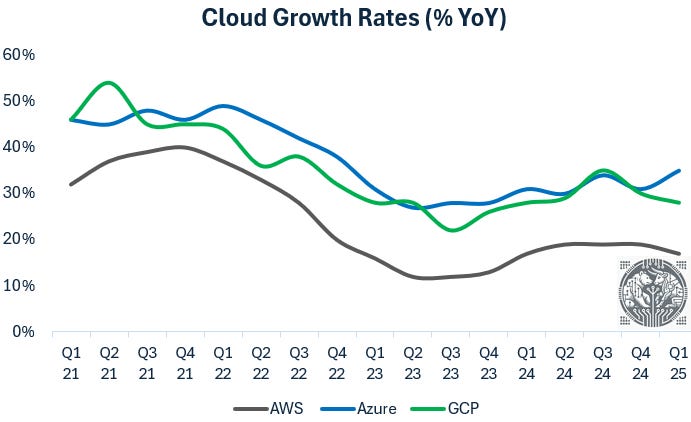

The three big public clouds were already amongst the best businesses in the world, and AI has again accelerated growth rates. For Google’s cloud platform, growth rates stepped up again towards the 30% range as from March last year:

Demand this year will be constrained by how fast Google is adding data center capacity, so clearly fast growth rates over the last year have taken them a bit by surprise as they haven’t been adding data centers fast enough. Getting a greenfield data center up and running takes around two-three years, and so sudden spikes in cloud demand growth can limit the availability of data center supply. This is Google’s CFO describing the current demand-supply environment:

“In Cloud, we're in a tight demand-supply environment. And given that revenues are correlated with the timing of deployment of new capacity, we could see variability in cloud revenue growth rates depending on capacity deployment each quarter. We expect relatively higher capacity deployment towards the end of 2025.”

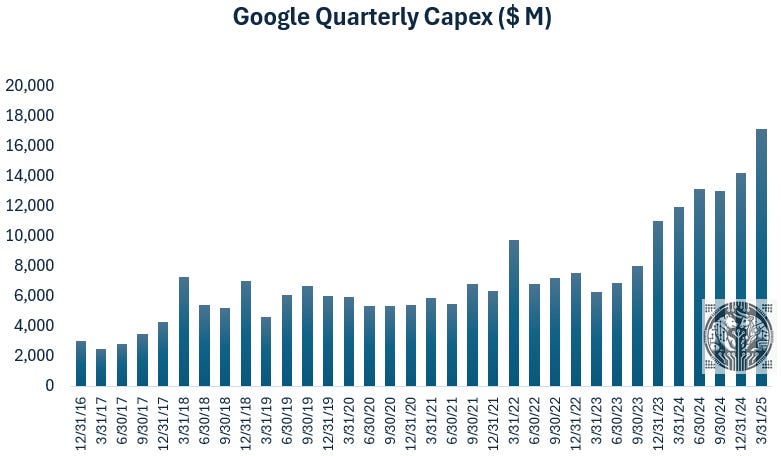

So it’s no surprise that the company keeps stepping up capex, as demand growth has been outstripping supply growth. The company is forecasting this year to invest around $19 billion in capex every quarter.

Customers are migrating large amounts of data to the cloud to fine-tune AI models, as well as AI workloads by querying LLMs in the cloud over API. An API is basically a web address where your code can send requests to, and then the server will process your query and send a response back. For example, a front-end app that’s running on a smartphone can send customer queries to the servers, and then AI agents running on these servers will help the customer sort things out. This is Microsoft’s CEO Satya Nadella on the data migration to the cloud:

“Microsoft Fabric has more than 21,000 paid customers, up 80% year-over-year. Fabric brings together data workloads like data warehousing, data science, real-time intelligence, along with Power BI into one end-to-end solution. Real-time intelligence is now the fastest-growing workload in Fabric with 40% of customers already using it in just 5 months since becoming generally available. And the amount of data in our multi-cloud data lake, OneLake, has grown more than 6x over the past year.”

Microsoft Fabric is basically a Databricks-clone, which is the hottest app for data science workloads in the cloud. The advantage of Databricks is that you can run it in multiple cloud environments, reducing vendor lock-in risk for customers. But the drawback is that the large cloud players such as Microsoft, Google and Amazon could subsidize their own data and analytics platforms, as they’re making enough money elsewhere in their clouds anyways, such as in basic compute. This is Nadella on how customers are using Azure as a platform to train and run AI models:

“Now on to AI platform and tools. Foundry is the agent in AI app factory. It's now used by developers at over 70,000 enterprises and digital natives to design, customize and manage their AI apps and agents. We processed over 100 trillion tokens this quarter, up 5x year-over-year, including a record 50 trillion tokens last month alone. And 4 months in, over 10,000 organizations have used our new agent service to build, deploy and scale their agents.

This quarter, we also made a new suite of fine-tuning tools available to customers with industry-leading reliability, and we brought the latest models from OpenAI along with new models from Cohere, DeepSeek, Meta, Mistral and Stability to Foundry. And we've expanded our family of SLMs with new multimodal and mini models. Model capabilities are doubling in performance every 6 months, thanks to multiple compounding scaling laws.”

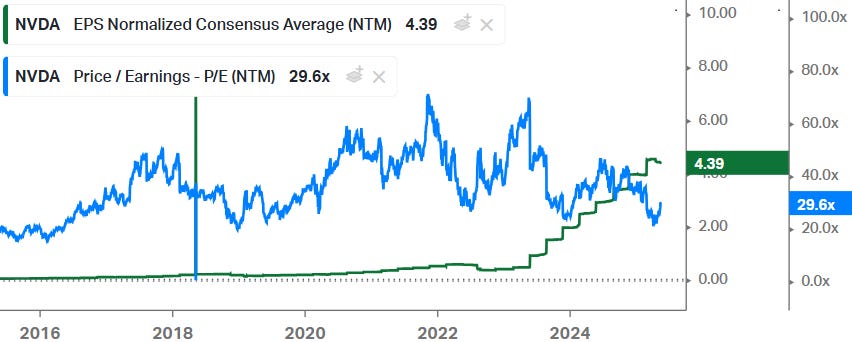

Note that half of all tokens processed over the last year were processed during the last month, which means that AI is exploding in the cloud. This all sounds promising for the hyperscalers and their suppliers, especially Nvidia where the market is currently assigning a bottom valuation multiple to its earnings, on the assumption that we’re about to peak in terms of AI spend. However, listening to both Google’s and Microsoft’s calls, this isn’t happening anytime soon.

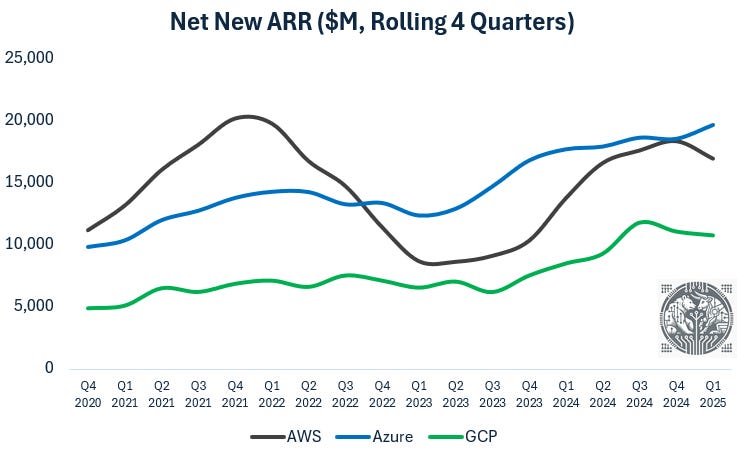

Microsoft has been a beast in the cloud—you can see clearly how they’ve strongly outperformed Amazon Web Services (AWS) over the last two years, adding much more annually recurring net new revenues to their business:

Google Cloud Platform (GCP) is the smaller cloud, but is gradually picking up steam as well. The chart below shows how their revenue growth rates are slightly below Microsoft’s Azure. Thus, Azure is not only adding the most revenues on an absolute basis, but it is also growing the fastest percentage-wise.

Under Nadella’s leadership, Microsoft has transformed from a rather solid, but dull, software provider associated with Windows, Office and other enterprise software such as databases and ERP systems, into a developer friendly platform providing both the world’s leading cloud as well as the best tooling to develop and manage software with such as GitHub, VSCode and even Linux on Windows.

There was some panic in the markets around Microsoft reducing their investment outlook over the last few months, however, the capex outlook remains strong. This is the company’s CFO on their investment plans:

“We remain committed to investing against the strong demand signals we see for our services. So our earlier comments on FY '26 capital expenditures remain unchanged, we expect CapEx to grow. It will grow at a lower rate than FY '25 and will include a greater mix of short-lived assets, which are more directly correlated to revenue than long-lived assets. These investments will ensure we continue to lead in the cloud and AI opportunity ahead.”

Also Microsoft is seeing a tight demand-supply balance in the cloud, this is the CFO during the Q&A:

“We talked a little bit about pulling some of that space to be ready earlier and being able to deliver that to customers this quarter, which is really good work by the teams as we continue to get more and more efficient at that process. I did talk about in my comments, we had hoped to be in balance by the end of Q4, but we did see some increased demand as you saw through the quarter. So we are going to be a little short still, a little tight as we exit the year, but we are encouraged by that.”

This is Nadella on how they’re thinking about what’s needed in the data center buildout:

“There's a demand part to it, there is the shape of the workload part to it, and there is a location part to it. So you don't want to be upside down on having one big data center in one region when you have a global demand footprint. You don't want to be upside down when the shape of demand changes because, after all, with essentially pre-training plus test-time compute, that's a big change in terms of how you think about even what is training. The idea that you can have test-time compute plus pre-training and then some of the great optimization at inference-time that has all happened, for every Moore's Law change and movement, there's probably a 10x improvement because of software. That's sort of what's happening with these models.”

Spreading investments out globally makes a lot of sense as AI inference will become a large market in the coming years, and it’s necessary to run these workloads closer to the end customer. The main risk to being able to capture this strong and structural demand growth in the cloud, is having access to the necessary power supplies. A director at Microsoft via Tegus discusses current constraints the industry is facing:

“The power and space constraints for data centers are still there, and it's a growing problem. Earlier, the constraint was GPUs. Right now, we have power and space constraints, and the way we are dealing with it is long-term planning. We are going and building ahead on data centers aggressively. Microsoft is looking for new ways of power, Google is looking for new ways of power, and hyperscalers are partnering with multiple other organizations to get rental power for example. Recently, there have been a lot of innovations around nuclear power and small modular reactors. Heavy investments on renewable power with contracts ranging up to 10-15 years have been in place. In summary, we're doing a lot of thinking for long-term as well as for short-term needs, and we're renting out capacity, space or power from different colocation facilities. There is no demand risk for this capacity. Right now, the demand is more than the supply for sure.”

For premium subscribers, we’ll dive deeper into current developments in hyperscaling and AI. We’ll discuss current developments in custom AI acceleration as well in AI apps, which long term will capture most value in the AI value chain. Historically, investing in differentiated software, ideally with network effects, has been the most lucrative area in the tech value chain. Examples include Google, Meta, Microsoft etc. This time, during the current AI revolution, of which we’re still in the early stages, this historical pattern will be repeated.

Note also that historically, during each new technology wave, the winners of the new wave eventually dwarfed the winners from previous technology waves. So, the winners from the PC and client-server era became much larger than the winners from the mainframe era, and the winners from the internet and cloud eras again dwarfed the tech winners from previous decades. Again, we think that this time will be no different as AI has the capabilities to automate large swaths of the economy. Thus, we think that the big winners in the AI era will dwarf the winners from the internet era in the coming decade. It’s a good bet that the first company with a market cap north of $10 trillion will leverage AI to automate parts of the global economy. Thus, this is a space we’re regularly keeping track of with the aim of identifying companies that are well positioned, with a competitive advantage, to capture these large opportunities.