Power semiconductors, SiC vs GaN

Power semiconductors are everywhere, as they are used in all applications where electricity needs to be controlled or converted (from AC to DC for example). Therefore, they will be essential as we transition the economy from being powered by fossil fuels to one running on green energy, for example solar and wind power in combination with large scale battery storage.

Traditionally, power semiconductors were silicon based. However, there are two materials showing much greater efficiency at handling power, i.e. silicon-carbide (SiC) and gallium-nitride (GaN). The advantages of these are numerous, but essentially, due to much lower heat generation and lost power, battery lifes of equipment such as electric vehicles and smartphones can be increased. As well as that devices can be made smaller, e.g. thinner TV screens.

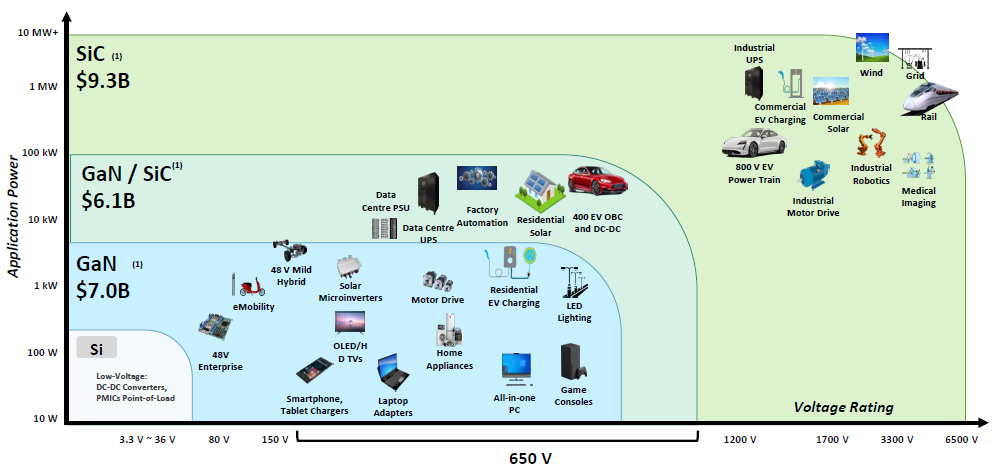

SiC is being used to handle high voltages, such as in electric vehicles, trains, wind and solar, and industrial robots. GaN on the other hand is being inserted in low voltage appliances such as laptops, TVs, smartphones and other home appliances. Although the material is now also seeing adoption at mid-level voltages where it will have to compete with SiC, or can be used in combination with SiC, such as in the data center, residential solar, and EVs. Navitas provides the following overview chart:

SiC is generally expected to be the far larger market, and also as the life cycles of these types of products is much longer, as a car model can be in production for 10 years vs 2 years for a smartphone, SiC should be the more interesting market of the two. This is a key reason why I reviewed Wolfspeed previously, a pioneer in SiC across the entire value chain, from wafer manufacturing to semiconductor fabrication. As well as that both SiC and GaN should remain high-growth markets for quite a while:

Generally, semiconductor companies providing to shorter lifecycle-type products such as smartphones are typically seen as lower quality. A smartphone model is only in production for a few years and in the subsequent generation, you might lose the slot for your semi. Suppliers to Apple especially will lead a nerve-racking life, as Apple has increasingly been taking semiconductor design in-house. However, even in this very competitive space, we have seen some highly successful semiconductor business models, with companies such as Qualcomm and Arm being prime examples. Even a less differentiated supplier like Dialog was taken over by Renesas and investors did great in these shares.

Navitas’ recent investor day

Navitas’ CEO started by explaining the benefits on GaN:

“Gallium-nitride and silicon-carbide are widely known as the key technologies to displace silicon and make the transition happen. The frequency is the key to GaN and SiC switching fast, because more than half of the bill of materials (BoM) of almost all power systems are in the magnetic and mechanical components — the EMI filters, the transformers, the inductors, the PCBs on the mechanical side, the housing plastic or metal — all of that is usually half or more of the system. The faster we switch the power device, the more we shrink the size, weight, and cost of that other half of the BoM. So it’s actually far more important to get the frequency up and reduce the cost of the rest than it is to take the cost of the GaN or SiC chip down. It allows you to have less energy burned up as heat. So you spend less money, time and effort on thermal management.”

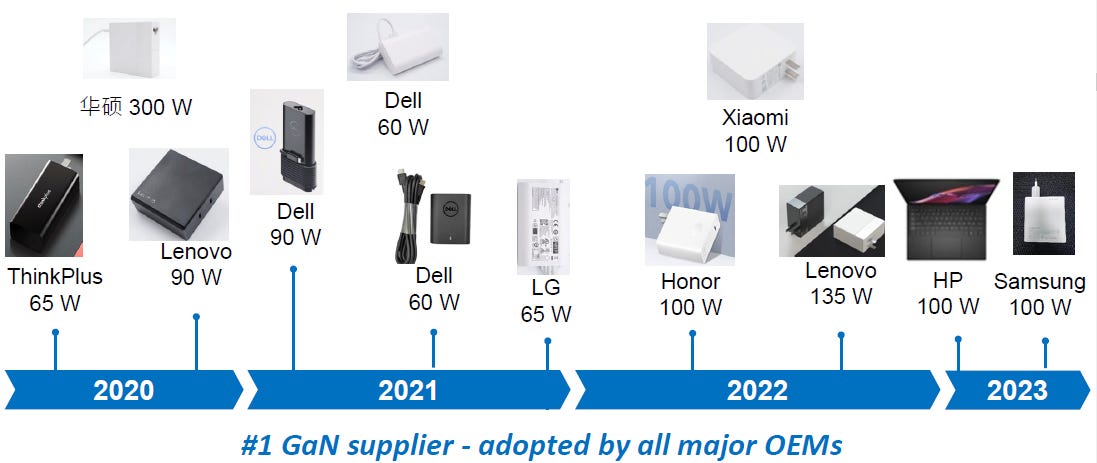

As GaN can switch much faster than purely silicon-based power semiconductors, one of it first applications has been in fast charging. The company gave the example of how one of their clients built a smaller fast charger with Navitas’ new GaN module:

Navitas’ CEO detailing this market:

“Over 250 GaN chargers are shipping in production, all 10 of the top 10 smartphone and laptop guys are already in production with Navitas GaN Fast chargers. By leveraging our proprietary technologies, we have created a 150-watt multi-port charger that is 38% smaller than Apple’s 140-watt single port charger, but it’s powerful enough to charge 2 laptops at high speed or power up to 4 devices simultaneously.”

Obviously Navitas has an extremely strong position in this market and attractively, there is plenty of room for growth as overall adoption of GaN-based chargers is still only at 10%.

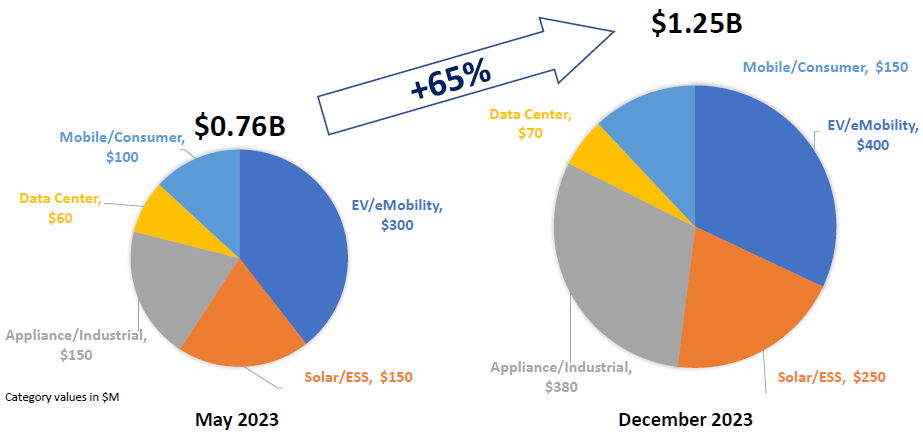

While the mobile charging market was the initial application of GaN, Navitas highlighted their $1.25 billion pipeline of programs expected to go into production in the next several years. This will shift the revenue mix towards more interesting markets such as solar, EVs, industrials, data centers, and home appliances. The estimated pipeline was raised with $500 million over the last 7 months alone, highlighting the strong momentum the company is seeing:

These new markets have been taking some time to come online as new chips have to undergo rigorous testing before they can get a win into a new product line. This is especially the case for EVs as a vehicle can be on the road for 10-15 years and under a wide variety of conditions, from the Canadian winters to the hot desert of Dubai.

The company’s CTO discussed the pipeline at the capital markets day:

“We’re taking conservative lifetime estimates for these different market segments, meaning 1 to 2 years in the mobile and consumer space, and 3 to 5 years in the other market segments. In EVs, we’re targeting diverse applications, starting with on-board chargers as well as roadside chargers. Today, we have significant SiC revenue in tier 1 EV players and we expect to ramp our GaN revenue in 2025. Today, we have our SiC technology in more than 50% of roadside chargers in the United States through our partnership with SK Signet. We are expanding and growing that footprint into other partners in roadside charging, and we’re working closely to develop solutions that will take the current 350 kilowatt state-of-the-art roadside charger from Tesla up to 1 megawatt or more.

Solar and energy storage, we have multigenerational GaN designs currently underway with the microinverter market leader, and we have GaN programs kicked off in the North America string inverter market leader.

We’re engaged with 7 of the top 10 home appliance manufacturers and we’ll start to see revenue late ‘24, ramping in ‘25 and beyond. We have strong and broad customer engagements across industrial applications: pumps, air conditioning, heat pumps, industrial motor drives. Specifically, we have a heat pump design in a top 3 player in that market, that could be $25 million to $50 million in just that design alone. And then we have 2 out of the top 3 industrial pump players that are currently designing with our solutions.

So data center is a very exciting space. We see AI driving and pulling the power density and efficiency ever higher, and that’s a perfect fit for Navitas. We have reference designs that we can leverage and we have engagements with the top 3 power system players. And we’re going to continue to drive that bleeding edge tier of power density and efficiency with the major data center providers in the US, as well as in China and around the world.

We’re now shipping in 10 of the top 10 mobile players, including the 5 major mobile phone players as well as the 5 largest notebook OEMs. In China, Xiaomi and Oppo expect that at least 30% of their mobile phone chargers will be GaN-based in 2024. These are not niche phones or expensive phones, these are mainstream phones with great battery life and huge screens. So it’s pretty compelling, having a battery charger taking less than 10 minutes to go from 0 to 100.

We’ve had some good successes in desktop PCs, gaming PCs, but now we’re seeing real traction in the gaming console market. We’re actively engaged with the top two console players worldwide for future generation development. They can leverage the smaller sizes to make more compelling products.

TVs are getting larger, but they are also getting thinner while requiring more power. That’s a perfect fit for our integrated GaN IC. So we have multiple tier 1 OEM design engagements underway, where we expect that we’ll be announcing shipping starting in the first part of ‘24.”

The company also mentioned a competitive advantage in chip size, Navitas’ CEO going into this:

“Also chip size is important. It’s not just about wafer price, our chips are 20% to 50% smaller across SiC and GaN compared to the majority of our competitors.

We spent a lot of time hiring the best engineers for each application, digging into the system requirements, understanding how to optimize for that, and now creating joint labs with our customers where we can co-develop each of these applications and drive that final phase of customer adoption.”

The final point of building labs around the world is an interesting one, as they will enable forming deep relationships with their customers.

They also showed a lot of the logos they’re working with, which included interesting names. For example in EVs, there is BYD, BorgWarner and Hyundai:

In solar, we can see both Enphase and SolarEdge, as well as CATL:

In data centers, there are Dell, HP, AWS, Azure etc:

In mobile, we have Apple, Samsung, Xiaomi and Sony.

On the last earnings call, the company discussed a win with Samsung:

“Navitas GaN has been adopted at Samsung to power the latest Galaxy S23 among other models, and is already contributing to our Q3 and Q4 revenue ramp.”

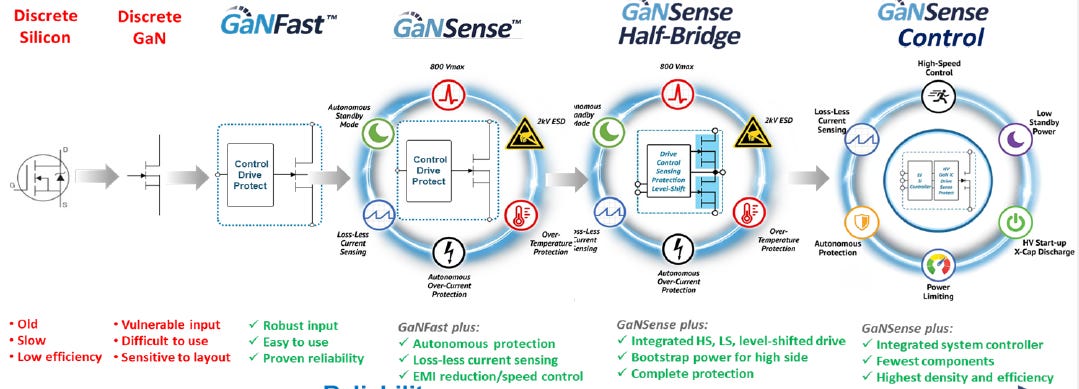

The company also highlighted well how their GaN solutions are evolving from generation to generation, from basic discrete semiconductors (i.e. one switch) to complete modules. For example, they highlighted a module which includes a controller to switch the device off if the current becomes too high. This was all packaged in a tiny 6 by 8 mm module. Innovations like these have been realized both from internal R&D as well as via acquisition.

A good example of how they’re innovating was given on the last earnings call:

“Potentially the most exciting and impactful announcement is a breakthrough innovation called bidirectional GaN. Now for the first time, GaN ICs can operate quickly and efficiently, conducting and blocking currents in both directions. This bidirectional GaN allows the replacement of up to four discrete power transistors, providing similar functionality while dramatically reducing component count, cost, and complexity, and delivering the speed and efficiency benefits of gallium nitride. We believe this invention has the potential to create innovative advances in energy storage, grid infrastructure, motor drives, and many other emerging topologies across multiple markets.”

For premium subscribers, we’ll review:

The GaN industry

Navitas’ move into SiC

The semiconductor cycle

Navitas’ foundry strategy

The key risk for the supply of Gallium

A detailed analysis of the financials and valuation of the company