Introduction

Advanced Driver Assistance Systems (ADAS) are likely to be be one of the highest growth areas in tech in the coming decade. Currently penetration rates are still low, but due to the strong progress of Tesla’s FSD, where the vehicle is now increasingly able to drive long and complex routes with zero or minimal human interventions, other large OEMs are starting to feel the heat. Even BYD, which historically was dismissive of this technology, is now introducing autopilots based on Nvidia’s hardware and Baidu’s mapping.

The autopilot industry exhibits attractive characteristics for investors. Due to the need for high quality and vast AI training datasets, the necessary engineering talent of which there is shortage, and large R&D budgets, this industry is likely to consolidate with only a limited number of strong competitors over time. The advanced players in self-driving tech are currently implementing two different strategies, with the first one being to offer an integrated hardware and software solution. Obviously Tesla has a very impressive product in this category, and Elon has mentioned they’re in discussion with one other OEM who is potentially interested in adopting Tesla’s FSD. The other strong player in the West with this strategy is Mobileye, who mentions they’re in discussion with 14 OEMS, which represent 52% of automotive production. And they have some impressive wins, most notably with the Volkswagen Group who will introduce Mobileye’s next-generation autopilots in its premium brands, which include Porsche and Audi.

The second strategy being pursued by leading players in this space, is selling the bare AI hardware so that automotive OEMs can train their own algorithms to drive their vehicles. The two key players here are Nvidia and Qualcomm. Nvidia goes one step further as they have developed an entire virtual world that is simulating a large variety of real-life traffic conditions, where OEMs can train their neural nets in. The company made a very lucrative deal with Mercedes, where they sell the Nvidia chip at a bargain, but subsequently take a 50% revenue share of Mercedes’ Drive Pilot. With a subscription starting at $2,500 per year.

Mobileye should be an interesting name for investors who reckon that a large number of automotive OEMs won’t have the necessary tech talent, know-how and data to develop an advanced self-driving product. This means that they’ll have to rely on a specialized and scale player to source this system from.

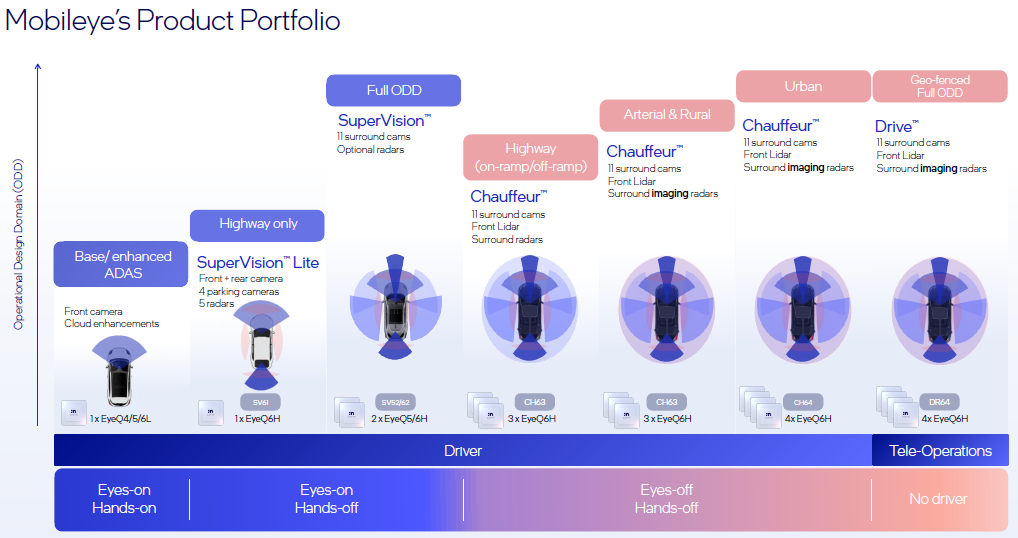

For its next generation autopilots, Mobileye has developed a hands-off system called SuperVision, an eyes-off system called Chauffeur, and a robotaxi system called Drive. These systems can make use of surround cameras, radars and one front lidar:

The main idea is that the vehicle can leverage the radar and lidar input when visibility is poor, such as under heavy rain, fog or at night. Radar is also excellent to detect the speed and velocity of surrounding vehicles or other objects, giving the autonomous vehicle a complete dataset of its surroundings. Mobileye has also been working on turning these radar and lidar based inputs into a second independent decision making neural net, so that the vehicle can continuously take the option with the highest confidence score out of the two input models, either the camera based one or the radar-lidar based system.

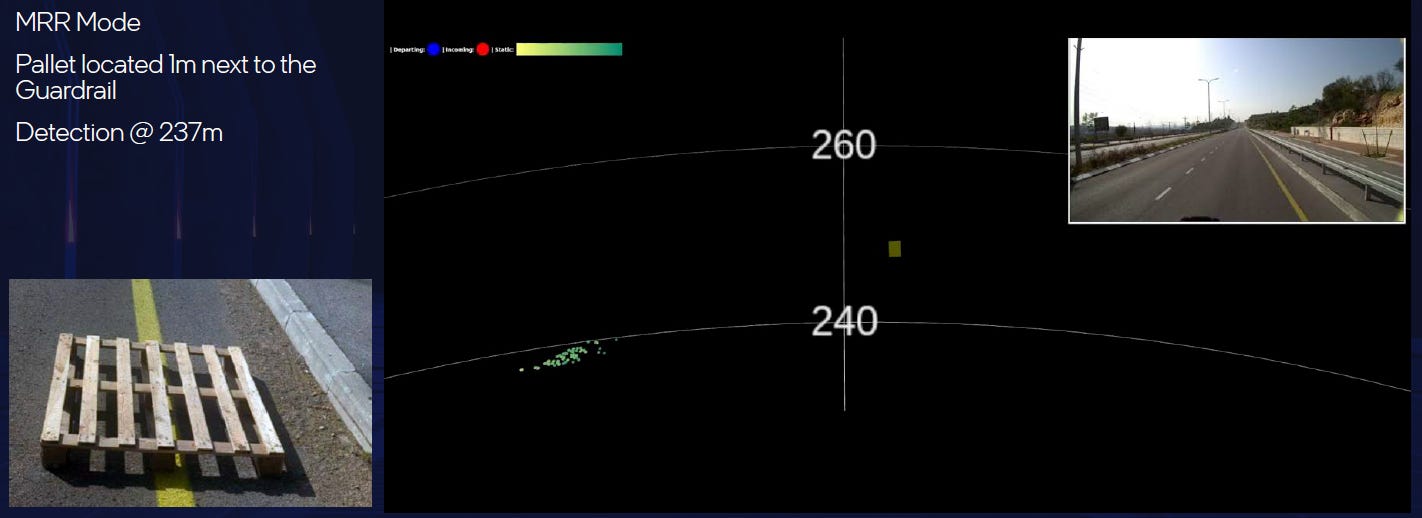

Another obvious use case of lidar is for long range detection, with in the below example a pallet being detected on the highway at 237 meters from the vehicle. So already the vehicle can start to prepare to switch lanes:

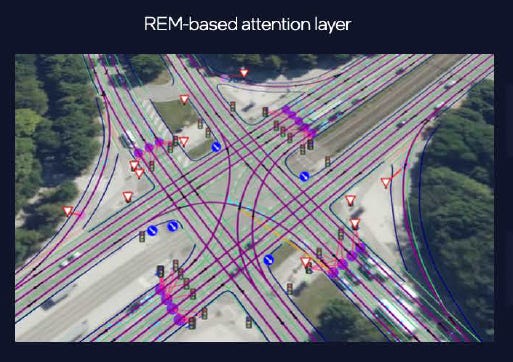

The final input that Mobileye’s AI relies on is its HD mapping. The benefit is that the vehicle already knows at any geolocation what the typical course of action is. For instance, when the vehicle arrives at a complex intersection, the AI already knows the path it’s going to follow. So it only needs to check if other objects might get in the way of this typical path, such as with temporary construction works, and it is only then that the system would have to come up with a creative solution, such as driving around the construction site. Another example is when the car arrives at a complex set of traffic lights. The map will provide context which light belongs to which lane and which light is for the pedestrians:

Overall, the attraction of the HD map is that the vehicle will have to figure out much less about its surroundings, as it already has access to large amounts of situational data. This reduces the risk of making a crucial mistake.

This is Mobileye’s CEO on the recent call detailing the performance of the new SuperVision system:

“When we look at the mean time between critical events, we did a test with one of our partner OEMs of our SuperVision vehicle in the U.S., where we have very good coverage of our REM maps, and the mean time between critical events is about 50 hours. This is about 5x better than the latest FSD version 12.5, according to the small amount of data that has been released so far. In China, it's much less than that because we haven't yet finished the localization, the REM coverage is not as good. And these are with the old EyeQ5 technology, imagine what we will do when we'll start launching EyeQ6. EyeQ5 does not yet have generative AI and with the EyeQ6, we have lots of generative AI components. All of our online and offline testing so far shows that we'll get a two orders of magnitude improvement.”

EyeQ6 will start shipping in the first half of next year and pack 8 CPU cores, one GPU, and four more ASIC accelerators for AI processing:

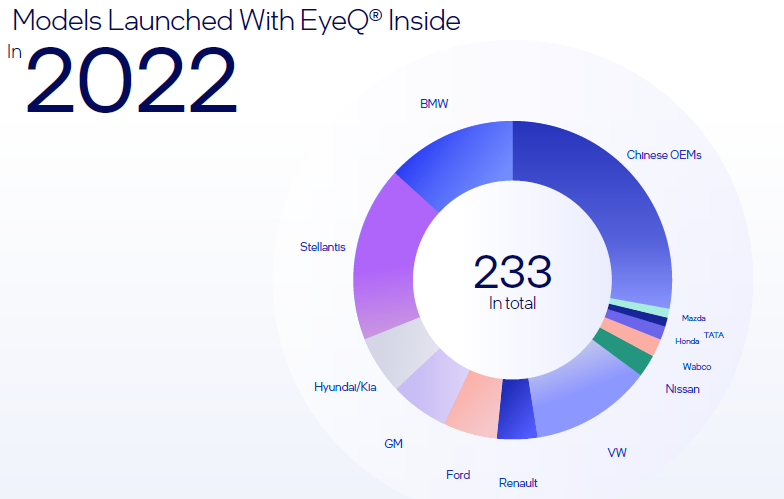

Mobileye has access to large amounts of mapping data as it launched this REM product in 2018, with EyeQ chips collecting data from their surroundings. In 2022 alone, these EyeQ chips were integrated in 233 model launches from a large variety of OEMs, as part of a base ADAS system:

Mobileye mentioned that they currently have 250 petabytes of labeled video data, which is even more than Tesla. As AI training is all about data quantity and quality, clearly both these companies should be amongst the best positioned to develop self driving systems.

Current EyeQ chips are largely being sold as part of the Mobileye’s base ADAS system, which is still making up most of its revenues. Next generation hands-off and then later on eyes-off systems will be sold at much higher ASPs. For example, a legacy ADAS is being sold for $50 per system while hands-off SuperVision is priced at around $1,500 per system and Chauffeur at $2,500. So going forward, Mobileye is well exposed to a strong revenue growth story with premium automotive vehicles upgrading to advanced self-driving systems such as SuperVision and Chauffeur. The company has also developed a mid-range autopilot, which will give an ASP lift of 4x compared to base ADAS. This latter system basically brings SuperVision capabilities to highways only.

We’re only at the beginning of this story really. So far, only a number of brands and models from Chinese OEMs are shipping with SuperVision. And then we have Volkswagen Group which will start shipping SuperVision, Chauffeur and Drive based products in the coming years. Mobileye’s CFO mentioned that these three advanced systems will start to scale significantly as from mid-2026.

An overview of the company’s design wins so far at the start of this year:

Mobileye mentioned on their latest call that they currently have advanced product wins or are in advanced discussions with 14 OEMs, representing approximately 52% of industry production. This is the company’s VP of Product Development detailing what these processes look like, and the outlook of getting deals done:

“The process of nominating this system is relatively complicated and involves many different activities starting from technically evaluating the system, building prototypes, doing global expeditions and performance evaluations, reviewing the architecture changes that are needed by the OEM et cetera. In addition, there is obviously the commercial part that needs to be negotiated to get to the right price point, and the investments needed in order to build this program, especially when we talk about incumbent OEMs, that have dozens or even hundreds of different vehicle models.

So the fact that it takes a few months or a year, in some cases more than years, it's natural given the magnitude of these decisions. At the same time, once these decisions have been made, it's very likely that the selected solutions will continue to be the backbone for the OEM for many years to come. We believe that we are now in the process of acquiring these OEM partners for our next-generation platforms. Once we do this in the next few months, we believe it will give us stability for years to come afterwards in terms of locking ourselves in as the technology provider for a very good portion of the top 10 OEMs in the world today.”

SuperVision has already been introduced in premium vehicles in China, and the company is getting good feedback. This is the IR on a recent survey they conducted with users:

“In a survey of about 600 Zeekr users, 85% said that they were either very satisfied or satisfied with the system, and 60% said they'd be willing to pay $3,000 to continue to have the functionality. Now, the reality is that no OEM is really charging for this in China because it's become part of the price war. So if you are trying to sell cars in China in the $45,000 and above pricing segment, it's very difficult to sell cars if you don't have a hands-free point-to-point pilot where you plug in the address and the car drives for you. There's 5 or 6 of these types of systems on the road in China.”

Overall, Mobileye should be a pretty straightforward investment case: the company has a strong market position for its existing products, there is a strong growth path ahead as ASPs of advanced autopilots will massively increase, while the market has been trading the shares based on short term volume expectations with the shares down 75%:

The key to unlocking strong growth in the coming 3 to 5 years ahead will be announcing further SuperVision and Chauffeur wins with large OEMs. Or Drive wins with ride hailing companies such as Uber, Grab or Didi. So far, the company has already won some Drive deals for shuttle bus operations.

While Mobileye paints a rosy picture for deals to come through, in this article we’ll go through findings from inside the industry to verify whether this is really the case. We’ll also discuss the current cycle, strengths and weaknesses of the various competitors such as Nvidia, Qualcomm and Tesla; the potential for the robotaxi Drive system, we’ll construct a detailed 2030 P&L with expected IRRs, and review Mobileye’s current financials and valuation, with concluding thoughts on whether the shares provide attractive risk-reward here.