A tour of Manhattan Associates

Manhattan Associates is a leading supply chain software provider to manage a company’s distribution operations. The company’s cloud platform is especially used in consumer goods, but it is also increasingly being adopted in other sectors such as in industrials, pharma and even energy. Its platform can scan and validate incoming shipments, optimize inventory throughout the supply chain, determine the best routing for transportation, manage orders and returns, track worker productivity and integrate with automated robotics systems. Gartner rates Manhattan as the number one in warehouse management systems:

And also Forrester sees Manhattan as the number one in order management:

Order and warehouse management have grown increasingly complex with the rise of digital. The warehouse system for example has to figure out whether a product can be picked up from a nearby store when a consumer is browsing the company’s website. Inventories have to be updated based on all sales via the different channels such as in-store collection, online delivery and in-store shopping. And keep track of any possible returns. Having a modern solution that provides the necessary information to both employees and customers of where and when products will be available is obviously a competitive advantage.

Speaking to several consultants, Manhattan is clearly the leading solution in the space. The company has invested substantially over the last decade to build out a modern solution in the cloud with wide capabilities. Competitors are playing catch up. Blue Yonder (Panasonic) for example is a number of years behind Manhattan and although Korber is still listed as a strong competitor by Gartner above, system integrators mention that they are far behind.

As a result, Manhattan is now shifting its customer base to the cloud. This is a highly attractive business model for investors. Cloud subscriptions bring in higher revenues than the classic ‘license + maintenance’ business model in software, while getting rid of lumpy license sales and moving these to annually recurring subscription revenues. This removes cyclicality for investors while giving high future visibility on the business. The below table illustrates the idea:

And subscriptions also allow for more regular price increases, which can be part of the contract. A nice feature of owning a business like this, is that ripping out and replacing a supply chain system takes the customer years and years. Often 3 to 4 years for even a mid-sized business, as the system has to be rolled out across all distribution centers and stores. And this across all countries.

So this is really a costly, risky and hugely time-consuming project for a customer. Something which a company will only try to do if the reason is really compelling, such as moving to a modern cloud-based solution from a legacy system. As a result, once Manhattan is built-in at the customer, its pricing power is strong.

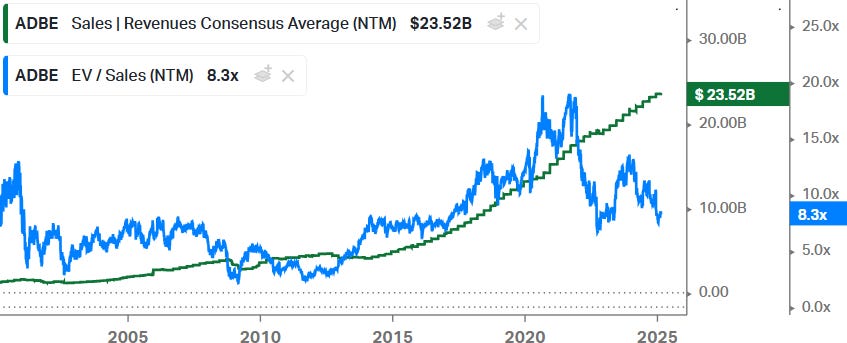

The classic case study in moving to a subscriptions-based business model is Adobe. The company started to move its customers to subscriptions as from 2013, which gave rise to high revenue growth once the initial negative impact of evaporating license sales started to wean off, and subscription revenues started accumulating:

And investors rewarded the company with a higher multiple as this story became clear. So this was a great opportunity last decade — the combination of high sales growth and expanding multiples resulted in a 10-plus-bagger for shareholders. Manhattan is now going through a similar business model transition.

This is Manhattan’s long time CEO, Eddie Chapel, detailing the company at the Baird conference last year:

“We went public in 1998. For the first 10 years, we were a one product and one country company. We provided warehouse management systems for large distribution centers. Then we grew into transportation management, order management, inventory management, retail point-of-sale and so on. Today, we're about a $1 billion revenue company. We started our cloud investments about 10 years ago. We have re-engineered everything, every piece of code from the ground up to have a truly versionless, cloud-native solution.

We focus now on Tier 1 and Tier 2 companies around the world, essentially companies that are $0.5 billion in revenues and up. We have some smaller customers than that, but that's sort of the sweet spot for us, and we have about 1,200 customers worldwide. Our biggest vertical is retail as that's where you have the most complexity in the supply chain. Also food service, grocery, third-party logistics, life sciences, automotive and high tech are verticals that we are dominant in.

About 80% of our revenue comes from the Americas and 20% from international. About half of our revenue comes from warehouse management systems, about 25% to 30% from order management, and 15% to 20% from transportation management and others. We have a 20% market share in warehouse management systems and a 2% market share in supply chain management overall, so there is plenty of runway in front of us. We have a 75% win rate against our top 6 competitors and in the 25% of deals that we don't win, 90% of the reason is that we lose on price. We are the premium solution in the market. Our aspirations are to grow at double-digit rates year-over-year with about 100 basis points a year of margin expansion.

With our cloud-native solution, we've managed to extend our lead. The biggest reason that our customers move to the cloud with us, is getting access to innovation. In the old world, you implemented a big software upgrade every 5-6 years. Today in a version-less world, we deliver brand-new capabilities every 90 days. In the distribution world, things are moving much faster these days, there's the need for robotics and automation, and just an overall changing profile in distribution operations. So we feel in terms of our moat in WMS, we had a pretty big one to start with and with our new technology and capabilities over the last 3 or 4 years, we benefited from our competitors not making that move. They haven't started yet or they're starting just now.

And frankly, I know how how big of a lift that is and how much effort it takes in time, money, resources and strategy. So given that we started our cloud journey 10 years ago and we're not going to stop innovating, I feel pretty good about keeping that market-leading position. We're taking market share for sure and we've done a pretty nice job of diversifying beyond retail. For example, we started doing business with Nike about 15 years ago and this was originally 100% wholesale. Now we even handle distribution for Exxon.

SAP is sunsetting their legacy warehouse management product and also their ERP, and that's definitely creating some tailwinds for us. The ECC to S/4 HANA move that SAP is encouraging people to make, is not a reinvention of technology. They're essentially taking their on-premise software and moving it into the cloud. What that signals to a customer is that there's no innovation. And that's fine for the core SAP solutions such as financials, order to cash and procurement. But in the areas around those core capabilities such as supply chain, customers are looking for innovation and we're the beneficiary.

One of our more recent customers, Schneider Electric, which is a wall-to-wall SAP customer, they're moving to S/4 HANA but they've broken away warehouse and transportation management. They awarded us a global contract to roll out across all their distribution centers and transportation systems. And they're not the only one. L'Oreal, Nike, Asda in the UK and so forth, all are going through that same ECC to S/4 HANA migration and are breaking away supply chain pieces. We've been the beneficiary and so I expect that to continue. Many customers of SAP's legacy WM have pretty rudimentary needs and they're satisfied with SAP's capabilities. They don't need innovation and so forth. But even if there are 10% of those that are going to be applicable to us, it would be highly advantageous.

Historically, cross-selling is about 25% of our new software revenue every quarter. In the old world of selling licensed software, it would not be unusual to go to a client who wants to buy WMS and we'd say ‘how about buying TMS as well?’ And then they would say only if it's a great deal. In the license world, you could make it a great deal and then they'd buy WMS and TMS together. In the cloud world, obviously you'd be paying subscriptions so nobody will start paying for something if they're not going to be using it for a while. Most companies find it hard to execute on more than one of these initiatives at a time. So as a consequence of that, they buy when they're ready.

We have a unified set of solutions with common technology, so as we see more customers move over to the cloud with only one product initially, the likelihood to cross-sell is higher going forward. We have an account team that are focused on existing customers, understanding their roadmap and working with them to build that roadmap. That's code for selling them more software. So we are building new products because there are market needs.

For example, point of sale, I've been asked at conferences whether we will ever get into point of sale and the answer was no. But retail stores have changed. They were the same for hundreds of years. You walked into the store, you picked up a product and you paid for it. So the retail store was a single function facility with a little cash register to consummate the transaction. That's all it did. Today, the store is a multi-function facility. It's a billboard for the digital business, it's also a customer service center, maybe you buy online and return in-store, and it's now also a mini distribution center. So you buy online and pick it up in store or curbside. All these many functions cannot be supported by a cash register. So the time was right for a next generation point of sale platform and that's why we launched.

The same is true for supply chain planning. Planning has been around for decades and these systems were batch-based. Retail companies would send a shipment to their stores once a week and then the CEO would get the sales report overnight on what happened yesterday. But today, order management systems are better and distribution centers are faster. We believe that the time is right to take planning systems from being batch-based, to continuously optimize what to buy and where to disposition inventory. And this is also a cloud-native solution that we built.”

So there are a number of interesting growth angles here. SAP has about 6,000 customers that use their supply chain solutions, with around 3,000 to 5,000 using their warehouse management. As SAP’s customers are now being transitioned over to the cloud, if Manhattan could win 10% of those making use of warehouse management, this could result in 300 to 500 additional customers. Manhattan currently has only 1,200 customers, so this could provide a substantial tailwind.

Secondly, cross-selling modules should be much more lucrative in the cloud. As Eddie mentioned, historically additional modules were frequently sold as part of one large license deal. And modules that the customer didn’t need initially were heavily discounted. In the cloud, you can switch on subscriptions for modules as you start using them, so customers will start paying full prices. And there is clear evidence that this is playing out, more on this later.

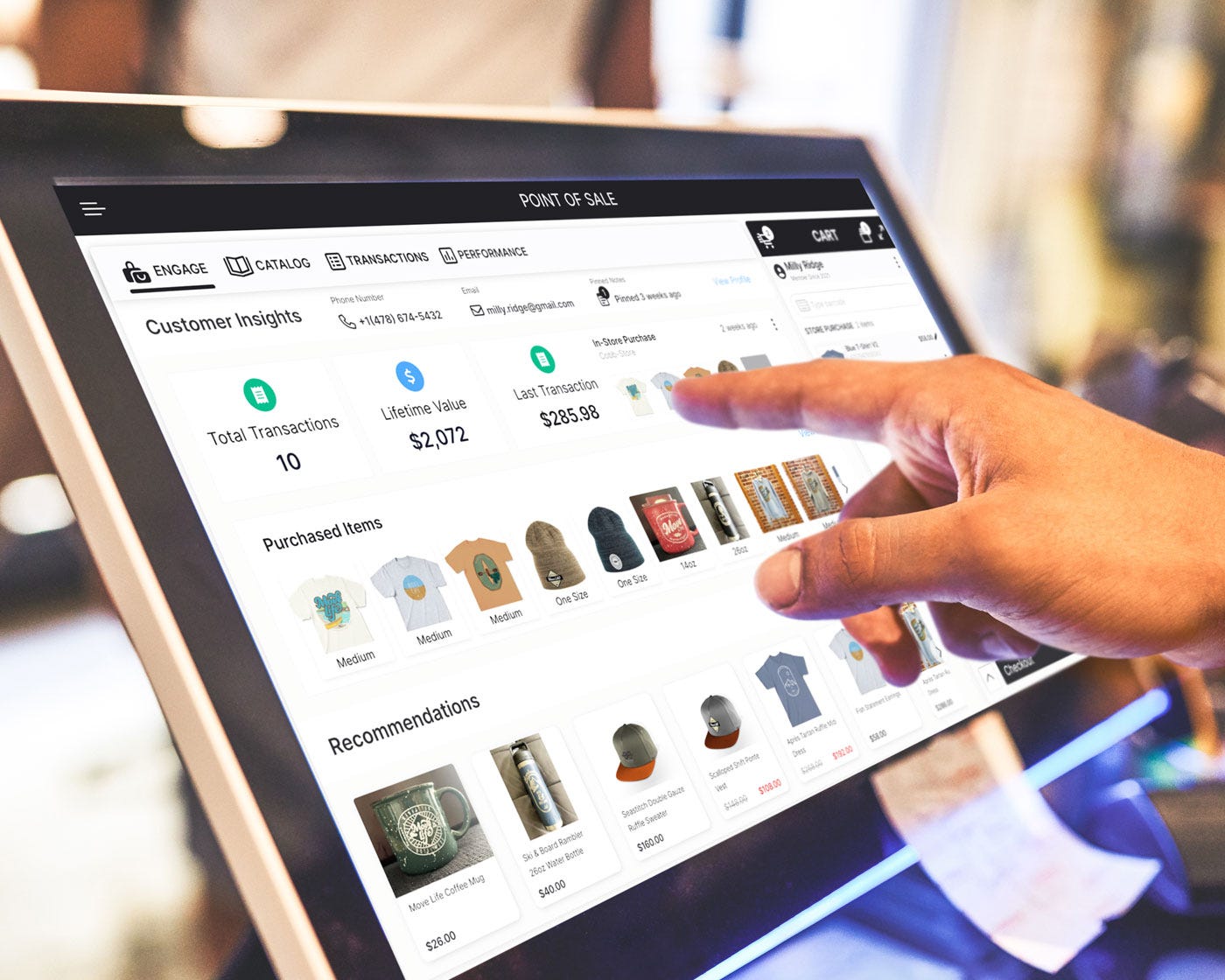

The third opportunity is the cross-selling of the company’s new products — point of sale and planning. Point of sale makes Manhattan’s cloud platform available to store employees so that they can check inventories, take payments and manage returns:

And you can access this solution on various end devices such as tablets, smartphones and even payment terminals:

Point of sale is a crowded space, but it’s a large TAM and could be attractive for Manhattan customers to make an advanced solution available to their store employees. Adyen is deploying a similar strategy with the goal of offering a unified system for customers to take both online and in-store payments.

We haven’t seen Manhattan’s new demand planning solution yet but the first customer will go live this year. There are a number of strong players in supply chain planning with cloud-based platforms such as o9, Kinaxis and Blue Yonder, but for some customers it could make sense to integrate forecasting inside of Manhattan’s platform.

Finally, Manhattan also closed a partnership with Shopify to integrate Manhattan’s order management system into Shopify’s platform. Given that Shopify is really a great business and which is now also increasingly being used by large enterprises, this could provide an interesting opening for Manhattan to gain new customers.

So Manhattan is obviously an interesting company — they are a leader in warehouse and order management software, and there is an obvious path for growth by gaining new customers, cross-selling additional software and by moving customers to higher value cloud subscriptions.

However, post the company’s recent results, shares sold off dramatically. With the shares now down 35%:

And with the company’s forward PE now back towards the bottom of its historical trading range:

For premium subscribers, we’ll give the insights from a consultant in the supply chain software space and from a large enterprise customer about what’s going on. We’ll dive into Manhattan’s problems and we’ll also flag one listed quality software name where these industry experts are currently seeing an acceleration in spending. Finally, we’ll analyze the financials and valuation of the key companies involved, and give our thoughts on which names should be good investments here.