The Battle for the TCB Market – Hanmi Semi vs ASMPT

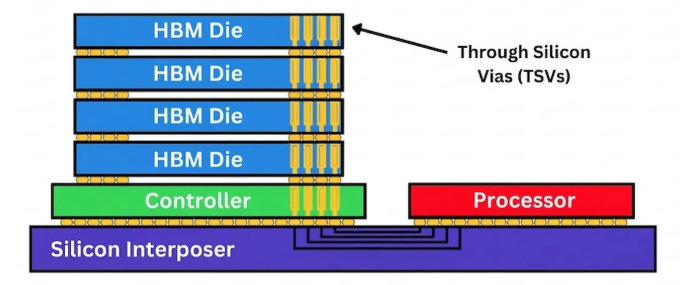

HBM (high-bandwidth memory) is a workhorse in the current AI boom. In HBM, DRAM dies are stacked on top of each other and connected through TSVs. This design allows for loads of fast working memory to be located close to the GPU. Bonding these DRAM dies together is a key step in back-end manufacturing (advanced packaging) as it determines the interconnect density, and thus speed and bandwidth.

This bonding process was dominated by Hanmi Semi over the last few years as the key supplier to SK Hynix (and Micron). However, the SK Hynix relationship soured when the latter started evaluating equipment from other suppliers. Currently, HBM die bonding is dominated by a technique called thermo compression bonding (TCB), and Hanmi Semi’s erratic behavior towards their key customer has now allowed ASMPT to get a strong foothold in the TCB market. ASMPT’s growth has exploded in the TCB market, and is now guiding for a 35-40% market share in this high-growth TAM. This is the CEO on the recent call:

“TCB momentum strengthened further in 2025 with significant new orders across logic and memory, solidifying our TCB technology leadership. We established deep engagement with both logic and memory customers and saw encouraging traction in areas such as HBM and C2W (Chip-to-Wafer) ultrafine pitch applications. This continues to reinforce our position as a leading provider of advanced packaging solutions as customers move to more complex chiplet-based and high-density architectures.

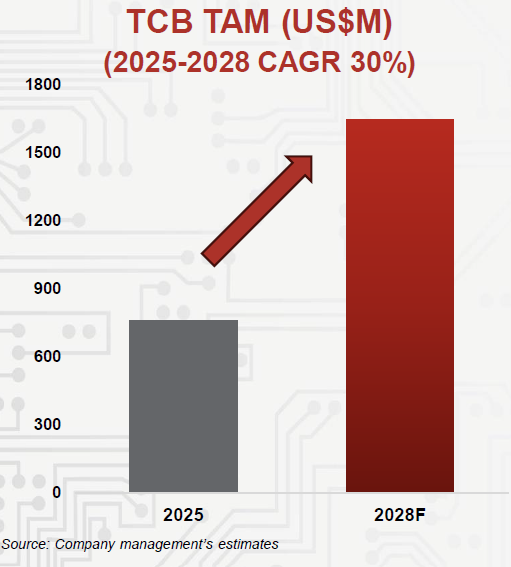

This time last year, we expected the TCB TAM to reach around USD 1 billion by 2027. Since then, the landscape has evolved meaningfully. The acceleration of AI-driven investment—especially in advanced logic and high-bandwidth memory—has expanded the market significantly more than our earlier assumptions. Based on our latest projections, we now estimate the TCB TAM to grow from roughly USD 759 million in 2025 to USD 1.6 billion by 2028, representing a CAGR of 30%. This reflects sustained adoption of 2.5D architectures, higher HBM stacks, and the industry’s move towards final pitch interconnect. These are all areas where TCB is increasingly the preferred solution.

Our target market share remains at 35% to 40%. With our breakthrough into the competitive HBM market, we grew TCB market share significantly, achieving record TCB revenue growth of 146% year-on-year. In 2025, our advanced packaging (AP) revenue growth of 30% year-on-year was driven by TCB.

Now, let’s look at TCB more closely. In logic, our C2S (Chip-to-Substrate) solution maintains its dominant position as a process of record with a steady flow of orders from key OSAT customers in 2025. Extending into early 2026, we are pleased to share that we have secured additional orders for 9 more TCB tools from the same customer. We are well positioned for further order wins as the market shift towards larger compound lines. At the same time, our C2W ultra-fine pitch platform secured orders for 2 tools in February 2026 from a leading customer. Since the announcement, we have secured 2 more such TCB tools from the same customer. As the industry transitions from mass reflow technology to TCB, ASMPT stands to benefit significantly as the preferred C2W solution provider offering plasma enabled capabilities.

In memory, we deepened our engagement with several customers and continue to expand our share with shipments in Q4 2025. Our tools have demonstrated superior performance with industry-leading production yields and interconnect quality. We were also the first to secure HBM4 12-high orders from multiple players, and we are now leading HBM4 16-high development with our flux-based TCB tool deployed for sampling, and our fluxless AOR-TCB process under qualification. These are important milestones for our technology leadership as HBM architectures scale further.”

During the Q&A we got more details on ASMPT’s positioning for the coming years:

“Currently, the HBM portion in the TCB TAM is definitely much larger than logic. But as we go a few years out, this dynamic will actually shift where logic, especially CoW, should take a larger share. But we cannot share the specific split for confidentiality reasons or competitive reasons. ASMPT is very strong in CoS and we are also making wins on CoW. Recently, we won two tools for C2W application and then we won two more. So I think it is a signal that we are also being recognized as a solid solution provider for the C2W space.

Now on the memory side, I think the competition landscape is different. We have a strong incumbent in the memory space, but a year ago, we broke into the HBM market and so we have gained market share there as well. In 2024, we had practically zero share in HBM. In 2025, we have a strong foothold in the memory market. For 2026, orders will come as our customer rolls out 16-high HBM in volume. As the industry moves from 12-high to 16-high, I think all equipment suppliers, including myself for TCB, are waiting anxiously for that particular customer to allocate TCB demand. So at this moment, we feel that 2026 will be a year whereby there will be new true demand for TCB for 16-high, but exact timing, I cannot give you any visibility at this point in time, but it cannot be too long before we know in our opinion.”

For years, Hanmi Semi (a South Korean equipment maker) was the dominant supplier of mass reflow bonders to SK Hynix, the leading player in HBM. However, diversifying the supplier base is fairly common practice for all leading fabs. For example, Intel for a long time kept sourcing a smaller share of its less crucial lithography tools from Nikon, even though those had far inferior performance compared to ASML. The reason is that they wanted to keep Nikon alive in the lithography race and not become fully reliant on ASML. So, it’s fairly common to give 70-80% share to the best equipment maker, and then 20-30% to a secondary player so that the fab can keep multiple options open. This also provides funds to the second player to stay alive in the innovation race.

So, in our view, it’s fairly normal that SK hynix started placing small orders with Hanwha Semi and ASMPT to test out their TC bonders. However, according to media reports, Hanmi subsequently recalled 60 engineers from SK Hynix’s fabs which were servicing the bonding equipment. Additionally, Hanmi notified SK Hynix of a 25% price increase. This led SK Hynix to accelerate its shift towards another strong supplier.

Because ASMPT’s equipment had apparently been successful in testing, this allowed the company to capture substantial TCB order flow in 2025. The Elec mentions that ASMPT has captured half of HBM4 TC bonders so far:

“SK Hynix is expected to place a large order of a hundred set of TC bonders for the production of HBM4 in March. This is when it plans to expand 1b DRAM production at its M15X fab at Cheongju. It remains to be seen how the chipmaker places orders for these bonders to ASMPT, Hanmi Semi and Hanwha Semi. SK Hynix uses around fifty sets of TC bonders for the production of HBM4 at the current stage, and half of these have been supplied by ASMPT. Hanwha Semitech’s bonders were not in use, sources said.”

According to Electrical Engineering World, ASMPT’s bonders are outperforming those of Hanmi Semi:

“A person familiar with SK Hynix said, ‘During the process simulation of HBM3E 16-layer, we found that the performance of ASMPT equipment exceeded that of Hanmi equipment as the number of stacked layers increased.”

So, it’s not really surprising that Hanmi Semi has been reporting disappointing revenues. This is JP Morgan on the company’s recent results:

“Hanmi’s 4Q earnings were a miss, with the OP coming in 40-60% below JPMe/ Bloomberg consensus with TCB sales recording the lowest since 4Q23. After two quarters of earnings misses from HBM4 qualification delays, we expect TCB earnings to recover in 1H26 from memory makers resuming TCB orders. Despite memory capex entering an upcycle, however, we see unfavorable risk/reward with Hanmi trading at a 30%-35% premium to peers with Samsung TCB optimism priced in. We remain UW with a PT of W150K based on 29x FY27E P/E and recommend investors trim at strength.

Hanmi shares have outperformed peers YTD which we attribute to: 1) memory capex entering an upcycle; 2) Samsung TCB optimism; and 3) the market’s perception of Hanmi being a higher beta to memory stocks. We agree that memory capex is entering an upcycle, but we emphasize that the upside risk is on the front-end capacity and conventional DRAM more than HBM where we do not sense any upward revision to HBM capacity in the next 12M. Samsung is testing both HCB and TCB for 16-Hi HBM4E, and while we expect Samsung to converge to TCB, we see limited reasons for Samsung to diversify TCB vendors.”

Samsung is heavily relying on its internal equipment maker, SEMES, to supply its TCB tools. This means that it is unlikely Samsung will adopt Hanmi’s equipment, unless Hanmi’s equipment strongly outperforms SEMES tools. To make matters worse for Hanmi, Macquarie points out that Hanmi could also lose share at its other key customer, Micron, which has been testing out ASMPT as well as Besi:

“Hanmi continues to face Hanwha Semi and ASMPT in SK Hynix’s value chain. At Micron, Hanmi remains dominant, but Micron has tested ASMPT and Besi, increasing competitive risk. While Hanmi entering Samsung Electronics’ HBM bonding is a catalyst that the market awaits, we see Samsung prioritising its subsidiary SEMES and considering alternatives rather than adopting Hanmi tools.”

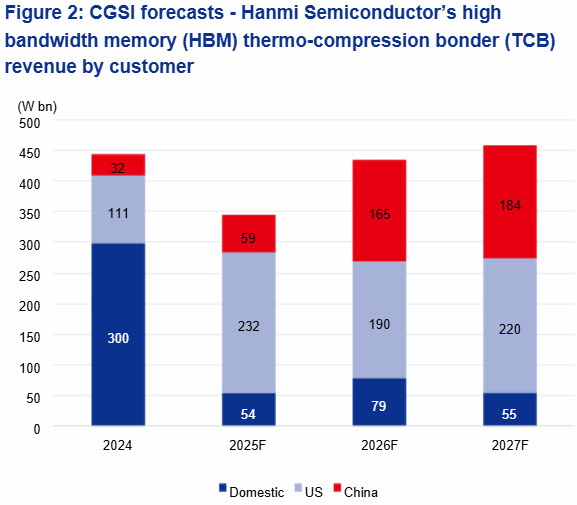

Asian broker CGSI models in revenue growth for Hanmi with as demand source Chinese packaging fabs:

However, this is a somewhat unreliable source of demand as increasing sanctions pose a looming risk, especially as Huawei is the end customer which has been a constant target of sanctions. From CGSI:

“As China pushes for advanced chip localization, centered on Huawei, we expect Chinese outsourced semiconductor assembly and test players (OSAT) to place large-volume orders for critical packaging process tools to Hanmi and key Japanese players, driven by Huawei’s production ramp-up for artificial intelligence (AI) chips amid the depletion of pre-secured HBMs. We expect Chinese HBM players to start mass volume shipment in 2H26F and project their monthly HBM through silicon via (TSV) capacity at 60k by end-2026F and 127k by end-2027F. Assuming 50% thermo-compression bonder (TCB) market share of Hanmi in China, we expect its China-bound bonder exports to jump to W164.6bn in FY26F and W183.9bn in FY27F from W58.9bn in FY25F, contributing 38% and 40% in total TCB sales in FY26F and FY27F, respectively, up from 17% in FY25F.”

Overall, the TCB semicap market is an interesting space for long term investors. Not only does it play a crucial role in the HBM market, but it’s also seeing increasing adoption in the logic market for 2.5D chiplet integration which is crucial to pack more compute into a single system. As Moore’s Law has slowed, the obvious way to pack more transistors into a single computing system is to simply cobble more dies together. AMD has been at the forefront of this trend:

ASMPT is forecasting a 30% CAGR in the TCB TAM, while ASMPT is the player with the momentum in this market. Obviously, the company is well-positioned to capture a strong market share of this future TAM.

Is it time to invest in ASMPT? Or are other names even better positioned to capture the value from the attractive outlook in advanced die bonding for logic and HBM end-markets? We’ll dive further into this space next.