Cloudflare’s sandbagging and AI network on the edge

As a brief recap, Cloudflare runs a network of edge servers located in smaller datacenters on which they’ve been building a wide array of software services, from cybersecurity to networking and application services. More recently, the platform has also become a mini public cloud version of Amazon AWS where developers can run workloads and store data. A key advantage of running services at the edge is proximity to the end consumer. Cloudflare can usually reach an end user within 50 milliseconds, giving an extremely smooth customer experience.

This has been a good story, and business is firing on all cylinders. This is the CEO discussing last quarter’s highlights:

“We achieved revenue of $379 million, up 30% year-over-year. We added 122 new large customers, those that pay us more than $100,000 per year, and now have 2,878 large customers, up 33% year-over-year. We are successfully moving upmarket and becoming a larger and more strategic vendor.”

He also gave a list of examples of big deals they signed, I’ll just flag two here for brevity:

“The National Cyber Security Centre, the U.K.'s technical authority for cyber threats, signed a 3-year contract with Cloudflare to deliver its protective domain name service. PDNS protects over 1,400 U.K. organizations in central government, local government, health care and emergency services from malware and cyber threats. This was a very competitive process with several vendors and a rigorous technical evaluation.

A large international energy company signed a 5-year, $4.5 million contract. This new customer is going all in with Cloudflare's SASE platform, with 6,000 Zero Trust seats along with CASB, DLP, Browser Isolation, Magic WAN and Magic Firewall. Competing against a first-generation Zero Trust vendor, our focus on scalability and efficiency as well as the ability to consolidate several vendors due to the significant value in our overall portfolio were key factors delivering this win.”

Additionally, the company has been busy restructuring its sales organization with the aim of accelerating growth. We got an update on their latest efforts:

“Just 90 days ago, we announced that Mark Anderson will be joining Cloudflare as our new President of Revenue to accelerate our next phase of growth at scale. The number of applicants for strategic account and enterprise sales positions increased 56% in March versus February following Mark's appointment. Across all positions, we had over 350,000 applicants in Q1, up 47% over the same quarter last year. We added several senior go-to-market leaders with proven track records in their areas of expertise, including a new Chief Partner Officer, a new Head of Global Sales and multiple regional strategic account sales leaders. If you're a sales professional who wants to win with great products and world-class leadership, the word is out, Cloudflare is the place to bet the next stage of your career. Beyond incredible hiring, our sales productivity from existing team members improved year-over-year. Sales cycles were similar to last quarter and new pipeline attainment exceeded our expectations. I feel extremely confident and clear in the long-term opportunity that Cloudflare has in front of us.”

Anderson was previously the CEO of Alteryx, President at Palo Alto Networks, and Head of Sales at F5 Networks.

As a final positive, the company has been installing GPUs in their end servers so that Cloudflare’s edge network can now be leveraged to run AI models close to the consumer. These are typically smaller models, not the huge language models such as GPT-4, but more in the class of Llama-2 and 3, as well as more traditional neural nets. We got an update on this interesting story:

“We're ahead of schedule rolling out GPUs across our network and now have them running in more than 150 cities globally, making us what we believe is the most widely distributed AI cloud by a huge margin. Our next generation of servers that begin to roll out in Q2 have GPUs built in by default and will support faster inference and even larger, more complicated models. Developers are building incredible new applications using Workers AI, and we're making it increasingly easy for them. We rolled out our partnership with Hugging Face, making it one-click simple to deploy most of their catalog of models to Cloudflare's network. And we added other bleeding edge models, including releasing Meta's Llama-3 simultaneously the day it was announced.

One of the largest e-commerce platforms out there is starting to use Workers AI to do image classification and generate keywords for their shops. A start-up in the drone space is taking imagery and turning it into 3D models. A handful of the public platform companies are using Workers AI for video description, transcribing and translation. A multinational online food ordering company, every once in a while, a restaurant does submit a picture for one of the dishes. And so they're actually experimenting with Workers AI to generate pictures of the food that you're serving. Hopefully, they disclosed that it's not an actual picture. A handful of photo and video editing platforms are using Workers AI or evaluating it in order to do image enhancement and make that better. There's a startup that's generating songs in local languages. Large consulting companies, public companies, the big gaming companies, all of which are worried about shadow AI, and so they're actually using Workers AI in order to understand how their own teams are using AI. A start-up is using a series of enterprise summarization tools where they can look at a bunch of emails and very quickly summarize them into executive reports. There's a public company in the financial services space that's doing real-time fraud detection.”

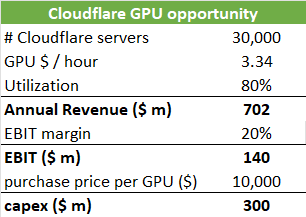

Having a GPU in 30,000 servers could bring in $702 million in annual revenues and $140 million in EBIT, which would nearly double Cloudflare’s estimated EBIT for this calendar year. So AI on the edge can become a meaningful business for Cloudflare over time and it’s certainly an interesting story to keep an eye on.

However, following the Q1 release, Cloudflare’s shares dipped 17%. These are the words from the CEO that spooked the market:

“In the short term however, my crystal ball is less clear. We see a lot of signals based on our privileged position running a good chunk of the Internet. Even without that visibility, if you've been watching the news at all, it's clear that the near-term outlook for the world is uncertain, increasing tensions in the Middle East, no end in sight on the Russia-Ukraine war and potential signs of instability in Asia. It's not at all certain on anything we see that things will get worse. But we do know from even recent history that macro factors can impact short-term sales trends.”

For comparison, these are the CFO’s remarks:

“Ongoing mixed macroeconomic data points and heightened geopolitical uncertainty remind us that we continue to operate in a business environment that remains challenging to predict. As a result, we remain prudent in our outlook for 2024. As you know, conservative is not a word that we use. When we talk about giving guidance, we tend to be thoughtful and prudent about it. And of course, it's a balance of the tailwinds we see, but also the uncertainty that is out there and in every major go-to-market transformation. In our case, it's actually more an evolution. There is risk, and it's reflected in our guidance, too.”

So what they’re talking about are mostly concerns about the economy as a whole, with a particular focus on a number of regional geopolitical conflicts which could indeed spill over into wider conflicts. If this is what concerns you, all cyclicals and high-growth stocks are indeed at risk, and you could rotate a portion of the portfolio into military suppliers and commodity names for example.

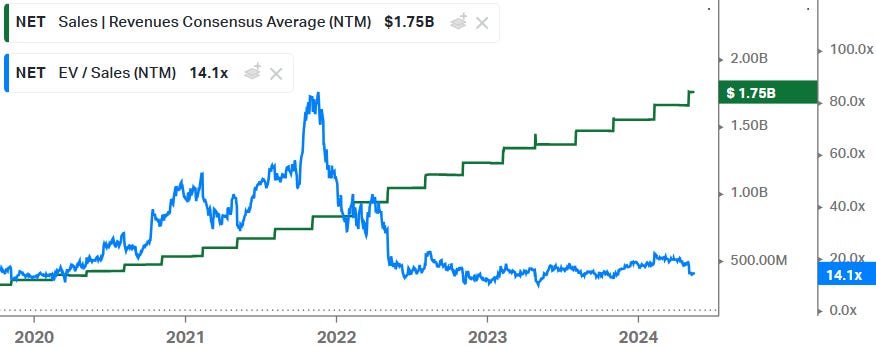

The market’s reaction can be explained by the fact that Cloudflare was trading on 18x revenues. With a multiple like that, you not only need an impeccable quarter, but also an impeccable guide. And given that there was some hesitation from management, the shares traded meaningfully lower. Personally, I think they’re sandbagging a bit and with the above mentioned drivers — i.e. cybersecurity, developer services, a better sales force, and AI on the edge — that we’re actually looking at a strong number of years in this name. Later on, the CEO seemed to be walking back already some of his comments, highlighting how increased global tensions are benefitting their cybersecurity business:

“We're fortunate that we're in the cybersecurity space, perhaps one of the few sectors that can actually benefit from increased global tensions. We're already seeing that, especially in our government business. The short term is uncertain, the long term is bright and so in the medium term, we're going to thoughtfully invest in our go-to-market efforts, in great engineering and in disruptive new products that deliver incredible value.”

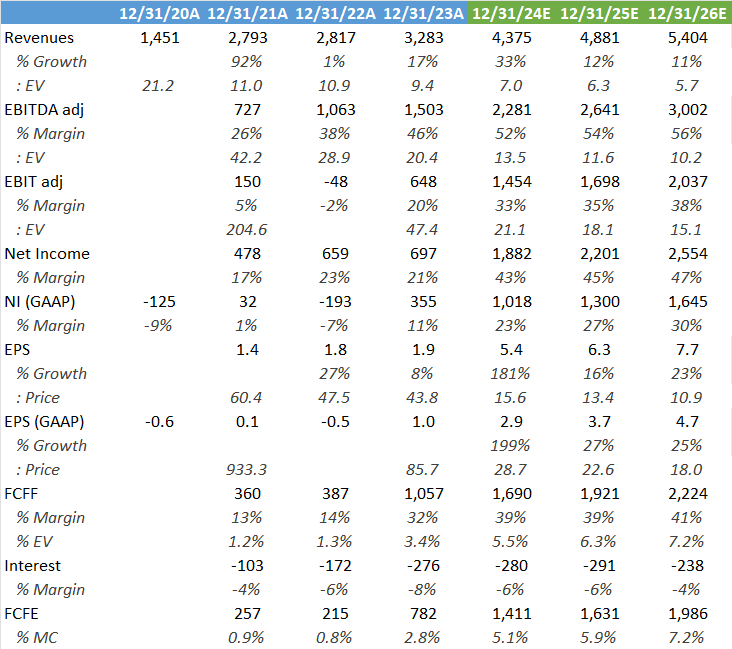

In my view, when these high-growth and good quality tech assets trade below 15x forward revenues, the risk-reward is starting to look attractive. Below is an example of how ServiceNow has traded on an EV-to-Sales basis and how the company has been growing its revenues. Even latecomers to the party in ‘16 who bought this stock at 8x sales still managed to catch a 10-bagger:

The market has gotten smarter since then and you can’t buy a name like this anymore on 8x forward Sales. In fact, the cheapest Cloudflare has ever traded is just below 11x:

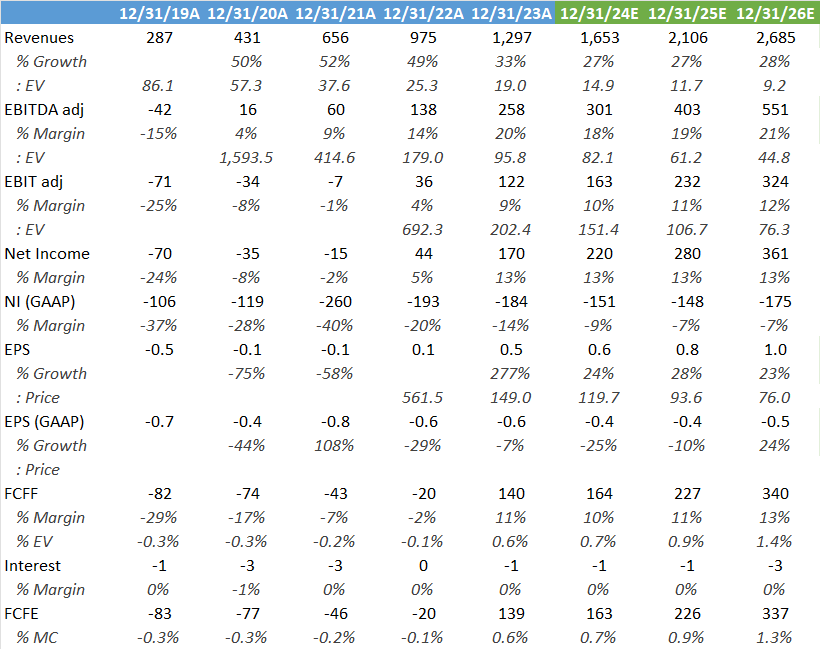

Looking at consensus modelling, the forecasted margins in the coming years look very conservative. As a result, we’re looking at a very high consensus PE. However, with the above mentioned drivers and the conservative modelling, it looks like there is plenty of opportunity to do better:

Unity vs Applovin

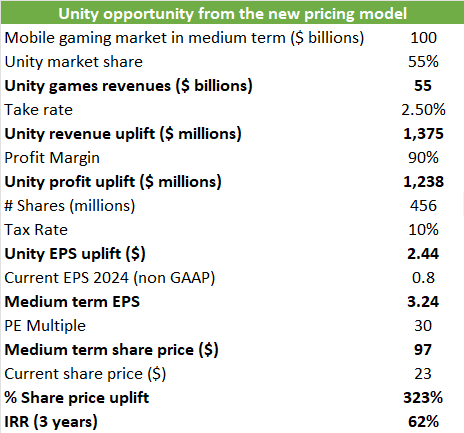

Unity is the dominant engine for mobile games development. Historically, despite its strong positioning, this business has been poorly monetized. We previously discussed how the company under new leadership is now moving to a new pricing model, which should unlock value for shareholders in the coming years. Typically, computer aided design (CAD) tools such as Unity are high margin business and trade at premium multiples, as investors like the sticky, recurring revenues with substantial pricing power. So over time there is strong potential for Unity to transition from being somewhat of an ugly duckling currently to a quality-growth asset.

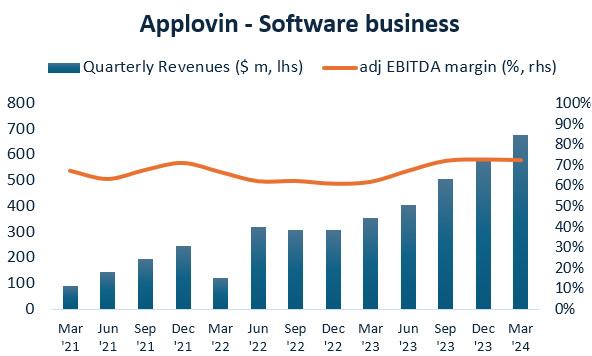

The other part of the business is managing ads for game publishers, where they compete with dominant player Applovin. We also discussed the latter a number of months ago as it offered attractive value for the high growth they’re generating. Unity is nowhere close to Applovin in this space, or at least for the moment. Whereas Applovin’s ad business has been growing at rates of close to 100%, Unity’s has been flatlining.

There should be scope for Unity to become a much stronger player here over time, but it’s good to keep in mind that a large part of this business is lower quality in nature and won’t attract software-type multiples.

Let’s start with the better quality part of ads. This is basically a take rate business where a game publisher sells ads within their games and Applovin’s or Unity’s platform will make sure that these are sold to the highest bidders. So far so good. This business is also called mediation. The second part of the business is what is called discovery. A game studio can pay Applovin or Unity to attract say 1,000 new users for a fixed fee. What these discovery platforms subsequently have to do is find these users at a lower cost, so that the business can make a profit margin. The way they do this is by leveraging the data they have and then buy ads in other games to target gamers which are likely to be interested in this new game. So it is really sort of an algorithmic trading business, where you buy ads cheaply and make a margin on this trade. It reminds me a lot of Criteo.

To be clear, the latter is not a business I would invest in for the long term. However, in the case of Unity, they do have a lot of data and are now integrating acquired IronSource, so it could be an interesting improvement story over the coming years. This is Unity’s CEO updating us how they’re planning to compete more effectively with Applovin:

“We're operating with, frankly, two different data science departments. So we weren't fully integrated in what we were doing. This year, as part of completing the IronSource merger, we've brought those organizations together. There was frankly a lot of data we just weren't fully using. We are now training our models using substantially more data. We actually now have some initial results that look super positive. And so we will be rolling those out more at scale through the rest of this quarter and it will bleed into July as well, which is why we see the back half of the year, as we've projected, kind of sequential improvement in the back half of the year.

Some of these tests, as we then talk to partners, they have been extremely positive, and we've actually had some people moving some more to LevelPlay with the results. And these are large Max customers (Applovin’s mediation platform) and so that leads us to believe that the interventions actually close much of the gap versus AppLovin.

Are we equal to them or not in ROAS (return on ad spend)? It's hard to exactly say, but the customer feedback has been actually extremely positive, and we are seeing share shift. And we think when we roll these out, we will continue to see that. No one wants to have one partner and so people want competition there. And so we've had a number of customers just say, we're being patient. We're expecting you to catch up.”

Applovin currently not only has the momentum, but the company keeps improving their engine as well. This is the company’s CEO on the recent call:

“Two themes are important to understand as our business goes forward. First, a key driver of our growth will be the ongoing improvements to AXON. Our models are still in an early stage and will continue to improve themselves. But more importantly, our teams are still finding ways to materially improve these algorithms. While these gains may not be predictable, they may sometimes lead to quarters like Q1 where we far exceed expectations. Second, there is nothing that limits our models to just gaming. By expanding into web-based marketing and e-commerce, we expect our AI models to improve with added demand diversity.”

On gaming, Unity introduced a new runtime fee that should work out to be around 2.5% of game revenues above $1 million. Previous CEO Riccitiello really botched the introduction of this new pricing model as he wanted to introduce it retroactively i.e. including for games already published. Needless to say this caused a lot of resentment in the gaming community which led to Riccitiello’s exit last year. After this episode current interim CEO Whitehurst took over.

This is Whitehurst updating us on the runtime fee situation and the launch of their new gaming development platform, Unity 6:

“We are seeing customers who were a bit ruffled at the end of last year feeling much more confident with us. We've gone from the what and why of a runtime fee to a recognition that the industry wants to make sure that we invest in the runtime. So we're having super productive conversations with our large customers. On Unity 6, that doesn't release until later this year. But if we look at the leading metrics, both the downloads and usage, it's the highest quality release at this stage that we've ever had and the time lines have pulled in.”

Unity has now hired a new CEO, Matthew Bromberg, who previously held the positions of COO at mobile games developer Zynga and VP of Strategy at Electronic Arts. Whitehurst, who did a great job at Red Hat, will stay on as executive Chairman. This is Whitehurst on the transition and outlook for the business:

“I'm remaining as Executive Chairman and what I'm really excited about is working on the Industry side of the business. I'm probably biased, but I still think that's a bigger opportunity in the long run than the Gaming business. It is still a relatively nascent opportunity for us, but the more I'm out talking to customers, the more opportunity I see there. In the long run, I continue to be super optimistic about the business as we are essential to gaming.”

Industry is essentially using the Unity engine to create digital twins of workplace environments and then also use this to train the workforce. The engine can also be used to illustrate to customers what a final product will look like.

Unity also closed a partnership with CapGemini which is one of the largest system integrators in the world. In software, it is important to keep an eye on these types of deals as these IT services companies enjoy a large corporate customer base, to which they can now also sell Unity’s software.

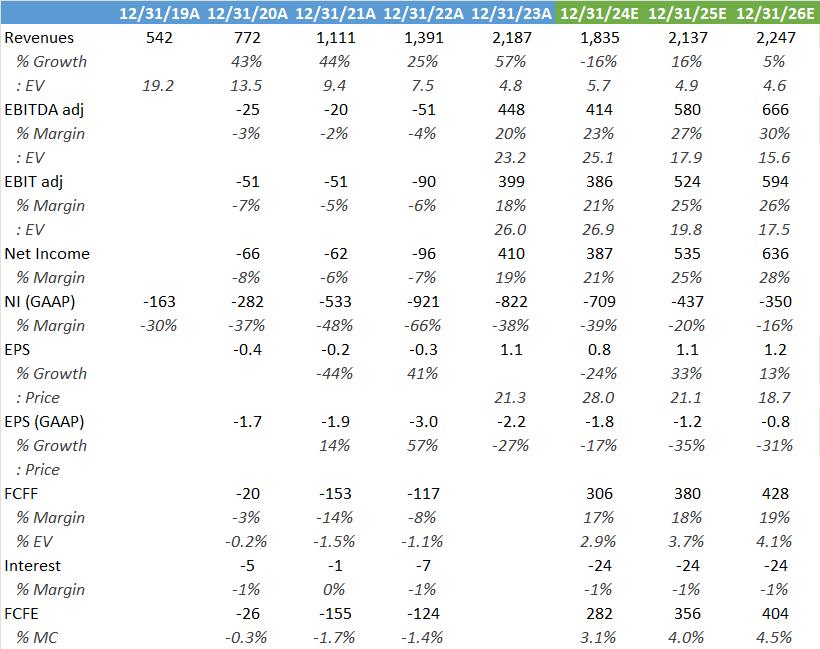

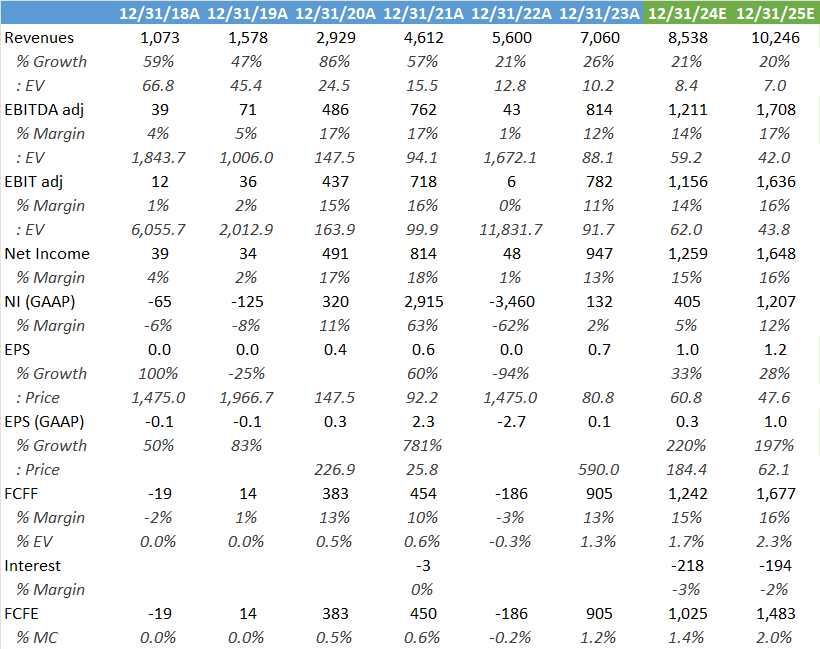

Under Whitehurst, the company divested some non-core businesses which weren’t making any money, after the acquisitive legacy of Riccitiello. So this year we get a reset in revenues although the impact on profitability will be limited. And as from 2025, top line growth should return. These are the sell side’s numbers:

Note that SBC is high in this business at $750 million, which at the current market cap of $8.7 billion is very dilutive.

On the positive, if a new pricing plan is successfully introduced, there is a lot of upside to consensus EPS:

And then we also have the prospect of Unity’s gaming engine being further utilized in the so-called industries business, which is already contributing 30% of the engine’s revenues. Furthermore, Unity has a strong share in development for VR environments and the company is also integrating AI tools into their engine, which can speed up development for studios and which is something they can start monetizing as well. Lastly, there is potential for the company’s ad business to become a more effective competitor to Applovin. So there are really a lot of levers here. Overall, I still like this story although the high SBC is obviously the main negative.

Applovin’s valuation remains undemanding at 15x next-twelve-months’ EPS. The company also has an attractive FCF yield of above 5% while consensus is projecting double digit annual top line growth with attractive operating leverage. SBC is much better under control, with only 1.3% of the market cap being paid out to employees over the last twelve months.

I actually invested in both names in January and while Unity has been a dud, or at least so far, Applovin nicely more than doubled. So net-net this space has still been a good place. Unity is a name I can see myself staying in for the long term, but with Applovin the plan is to purely ride this wave of momentum the company is currently enjoying.

Shopify’s sell-off

We reviewed Shopify last December following the company’s investor day, and while the SaaS platform for e-commerce stores remains a compelling growth story, valuation was looking a bit steep at the time with a forward PE of 75x. While the company remained performing solidly with gross profit growth rates currently at 33% year-over-year, the company gave a tepid outlook for Q2, causing a sharp decline in the share price of around 25%. This stock basically had the same problem as Cloudflare, with such a highly demanding valuation, results and outlook need to be impeccable.

Shopify has two revenue streams, software subscriptions where customers can run their e-commerce operations from and merchant solutions which is mostly payments processing:

This is Shopify’s President discussing the business and outlook, note that the company recently divested their logistics business which is impacting results:

“Revenue for the first quarter was $1.9 billion, up 23% year-over-year, which equates to 29% year-over-year growth when excluding the logistics businesses. This represents the fourth consecutive quarter that our revenue growth has been greater than 25% on an organic basis. The key drivers of this growth were: the GMV strength just discussed; growth in Subscription Solutions revenue from both new margin growth and the pricing increases on standard plans; and lastly, increased payments penetration, which hit 60% for Q1.

Our expectations for the second quarter of 2024 are as follows. We expect Q2 year-over-year revenue growth to be in the high teens on a GAAP basis, which equates to a year-over-year growth rate in the low to mid-20s when excluding the 300 to 400 basis-point impact from the sale of our logistics business. An important dynamic to highlight is the impact of the standard and plus pricing changes and how they affect our growth rate for Q2 versus Q1. The impact of the pricing changes in standard and plus will have a smaller combined benefit in Q2 versus Q1.”

The company also has been introducing its Shop Pay button which has a very smooth user experience, or at least whenever I’ve used it, in the form of low latencies to complete a payment. This compares to Paypal’s current button which gives a rather sluggish impression, probably that codebase was written 20 years ago or so and has only been expanding ever since. Sometimes it’s best to just rewrite the entire thing from scratch and speed things up.

This is Shopify’s President on Shop Pay:

“Shop Pay is the highest converting checkout on the Internet. It converts up to 36% better than competition and 15% more on average. There's now 150 million buyers that have opted into Shop Pay. And for Q1 alone, we facilitated $14 billion of GMV, that's a 56% increase year-on-year. Customers want to use Shop Pay because the mere presence on the checkout results in a 5% higher conversion. It's becoming a really bad idea for any brand or any retailer on the planet to not use it.”

This is a company with limited competition and Shopify is also successfully moving up-market. Traditionally Shopify was a SaaS platform for mom-and-pop ecommerce stores, but more and more larger brands are starting to run their operations from the platform. Both for direct-to-consumer and wholesale activities. Shopify’s President highlighted an independent study that concluded the Shopify platform to have a lower cost of ownership of up to 36% in the enterprise space.

With the still attractive growth rates and low penetration rates in e-commerce, there is a lot to like in this company. Near term growth will be a bit weaker as the tailwind of past price increases rolls off, however, investors have the prospect of new price increases in the coming years. Typically I like adding to good quality, high-growth assets when they sell off sharply for short term reasons and historically, this has been a strategy which has been working extremely well. So I’ve taken again a position in Shopify and will probably stay in it for the long term.

If you enjoy research like this, hit the like and restack buttons, and subscribe if you haven’t done so yet. Also, please share a link to this post on social media or with others who might be interested, it will help the newsletter to grow which is a good incentive to publish more.

I’m also regularly discussing tech stocks on my Twitter.

Disclaimer - This article is not a recommendation to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it can not be guaranteed that all information used is of this nature. Before making any investment, it is recommended to do your own due diligence.

I agree with you. I think Cloudflare has a lot going for them and they continue to uplevel the team! Great post.

Great Unity write up... I sometimes struggle to see the long-term picture on this stock amidst all the negative noise.