ASML's Problems, and the Outlook for Litho

A deep dive on the leading edge semi space - ASML, Lam Research, ASM and TSMC

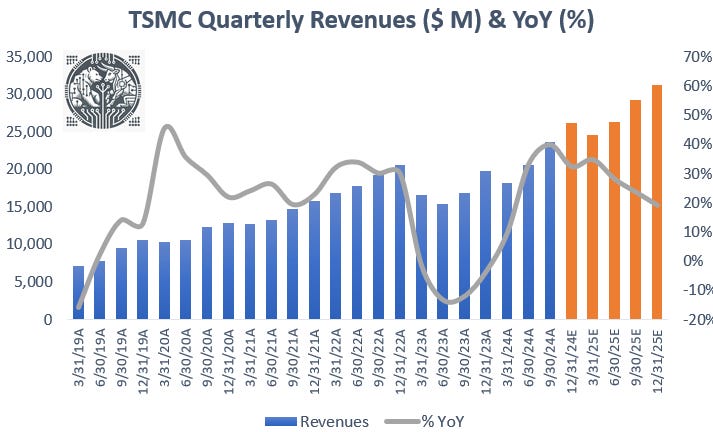

Introduction, TSMC is on fire

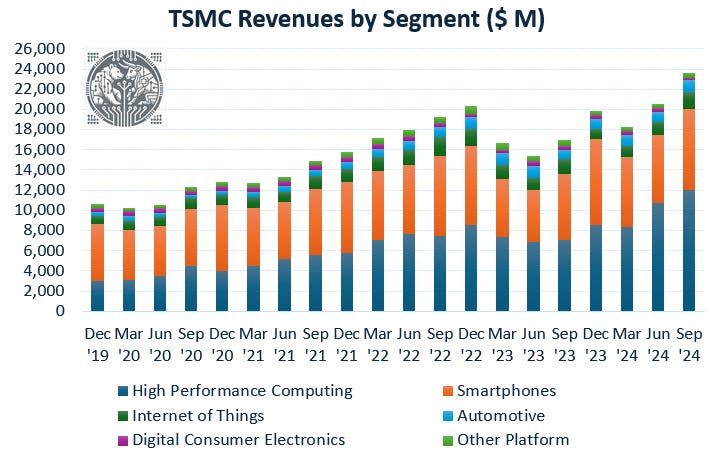

TSMC once again had a stellar quarter with 39% year-on-year and 13% sequential top line growth. The results were strong across the board with the two most important end-markets, smartphones and high-performance computing (HPC), growing 16% and 11% quarter-over-quarter:

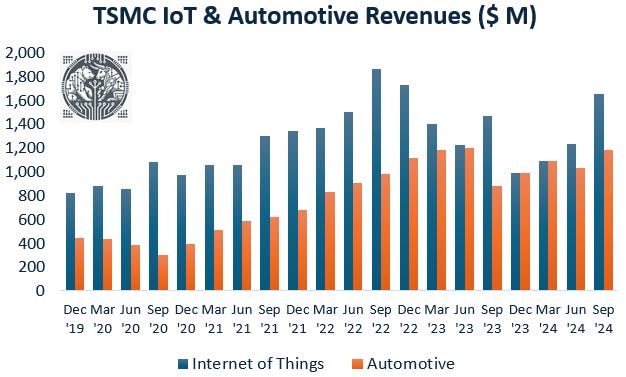

Also in mature semis, we saw a stellar recovery in IoT especially (+35% QoQ) with also automotive revenues continuing to pick up:

This the company’s CEO, CC Wei, discussing the overall business and the outlook in AI especially:

“We now forecast the revenue contribution from server AI processors to more than triple this year and account for a mid-teens percentage of our total revenues in 2024. This AI demand is real, we are talking to our customers all the time, including hyperscaler customers who are building their own chips. Almost every AI innovator is working with TSMC and so we get the deepest and widest look of anyone in this industry.

Why do I say it's real? Because we are using AI and machine learning in our fabs and R&D operations. With AI, we are able to drive productivity, efficiency, speed and chip quality and I believe it's just the beginning. My key customers said that the demand right now is insane. It's a new form of scientific engineering and it will continue for many years.

We have many customers interested in the 2-nanometer node. Today, we actually see more demand than we ever dreamed about compared to N3, so we are preparing more capacity in N2 than in N3 and this will be followed by A16. A16 is very attractive for AI server chips and so we are working very hard to prepare both 2-nanometer and A16 capacity.

The unit growth of PC and smartphones is still in the low single digit, but more importantly is the content. Now that we put more AI into the chip, the silicon area increases faster than the unit growth. So again, we expect the PC and smartphone business to be healthy in the next few years.

We are putting a lot of effort to increase the capacity of CoWoS. Today's situation is that our customers’ demand far exceeds our ability to supply. So we we increased the capacity by about more than twice this year compared to last year, and we will probably double it again next year but it still won’t be enough. Anyways, we are working very hard to meet the customers’ requirements.”

So the most interesting bit here for Nvidia investors is that CC Wei is thinking that doubling CoWoS capacity next year won’t be enough. Nvidia is going to do around $110 billion in datacenter revenues this year, so doubling again next year would mean we could be looking at $220 billion in datacenter revenues. However, as we discussed a few weeks ago, hyperscalers are looking to shift more AI workloads to their own silicon, with for example Amazon placing the strongest growth in AI silicon orders for next year with its own Trainium chips:

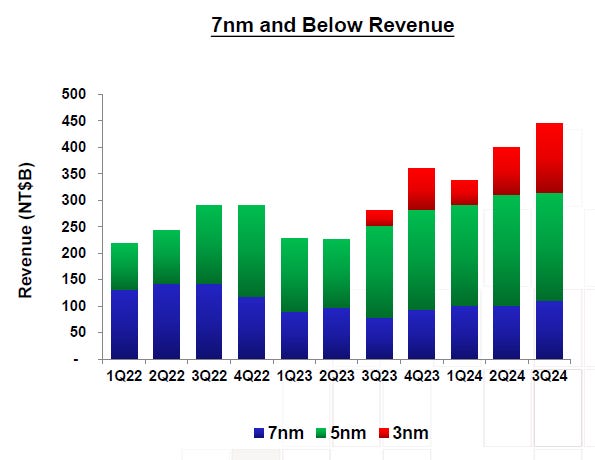

In the meanwhile, TSMC’ new N3 node continued ramping successfully..

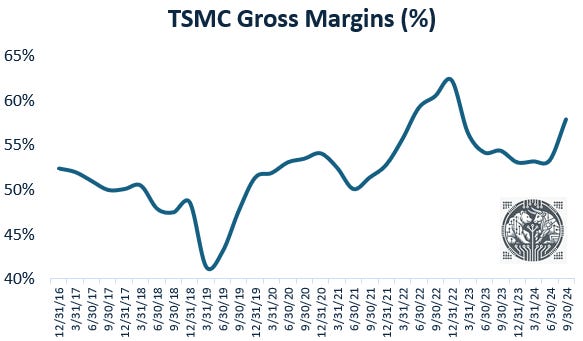

.. giving a strong boost to the company’s gross margin, together with cost optimization efforts and higher fab utilizations overall:

However, for the coming years, TSMC is guiding for 2 to 3 points of gross margin dilution. This is the company’s CFO on the various factors at play here:

“Next year will be a healthy growth year so utilization will also be positive. On the other hand, there'll be a 2 to 3 percentage point dilution from the overseas fabs when we begin to ramp them. In Arizona and in Kumamoto, we are ramping more than one phase, so when phase one begins to improve its profitability, the second phase comes in, and then the third phase.

At the same time, we are also converting some of our N5 capacity to N3 to meet the strong demand for N3. And don't forget, we're ramping N2 in 2026 so there will be some preparation costs. As we migrate to more and more advanced nodes in the future, these preparation costs will become bigger and bigger.

Now you also know that the electricity cost has risen, we had a 15% increase in 2022, a 17% increase in 2023, and a 25% increase in 2024. Next year, we think that the electricity price for us in Taiwan will be the highest of all the regions that we operate in. This is expected to impact our gross margin by at least 1%.

Advanced packaging in the next 5 years will be growing faster than the corporate average. In terms of margins, it is improving and it's approaching the corporate margin, but we’re not there yet.”

This is CC Wei discussing TSMC’s execution on the overseas fabs:

“In Arizona, we received a strong commitment from our US customers and the various governments, our plan is to build three fabs to create greater economies of scale. Each of our fabs in Arizona will have a clean room area that is approximately double the size of a typical logical fab. Our first fab entered initial wafer production in April with 4-nanometer process technology, and the result is highly satisfactory with a very good yield.

We now expect volume production of our first fab to start at the beginning of 2025. We are confident to deliver the same level of manufacturing quality and reliability in our fab in Arizona as from our fabs in Taiwan. Our second and third fabs will utilize more advanced technologies based on our customers' needs. The second fab is scheduled to begin volume production in 2028 and our third fab will begin production by the end of the decade.

In Japan, our progress is also very successful. Our first specialty fab has completed all process qualifications. Volume production started this quarter and we are confident to deliver the same level of manufacturing quality and reliability in our fab in Kumamoto. The land preparation for our second specialty fab has already begun and construction will begin in the fourth quarter next year. This second fab will support consumer, automotive, industrial and HPC-related applications, and volume production is targeted by the end of 2027.

In Europe, together with our JV partners, we had a groundbreaking ceremony in August for our specialty technology fab in Dresden, Germany. This fab will focus on automotive and industrial applications utilizing 12/16 FinFET and 28nm process technologies. Volume production is scheduled to begin by the end of 2027.

Under today's fragmenting globalized environment, overseas fab costs are higher for everyone in the industry. We are leveraging our fundamental competitive advantage of manufacturing and technology leadership. Thus, TSMC will be the most efficient and cost-effective manufacturer in the regions that we operate in, while continuing to provide our customers with the most advanced technology.”

So it’s looking like Arizona will become a massive fab hub. And a former director at TSMC was also very positive on the company’s fab hub in Kumamoto, Japan, citing a similar low cost structure and workforce culture as the company is enjoying in Taiwan:

So TSMC’s recovery is in full swing, and the market is looking for 25 to 35 percent year-over-year top line growth in the coming four quarters:

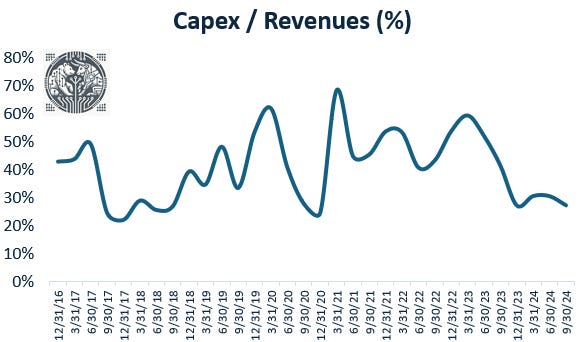

Additionally, TSMC is doing this in a relatively asset-light manner, with the capex-to-revenue ratio close to historical lows, giving a strong outlook for future margins:

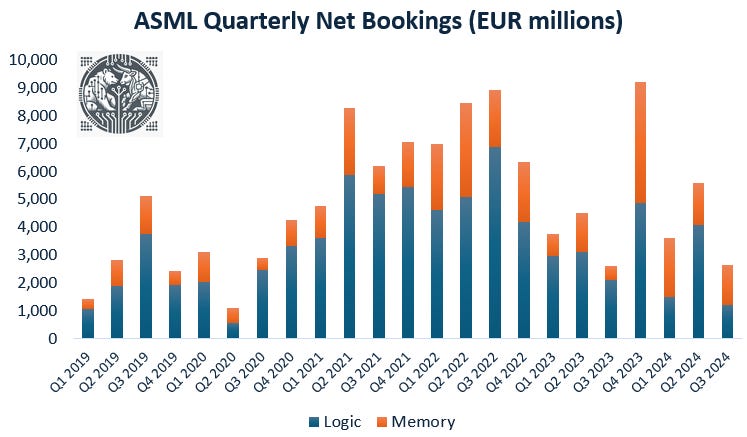

So one might think that ASML’s lacklustre order numbers — and outlook for ‘25 — are due to TSMC’s current capital efficiency..

.. however, other leading edge semicap providers such as ASM International are seeing healthy order growth, even when compared to the covid semi boom:

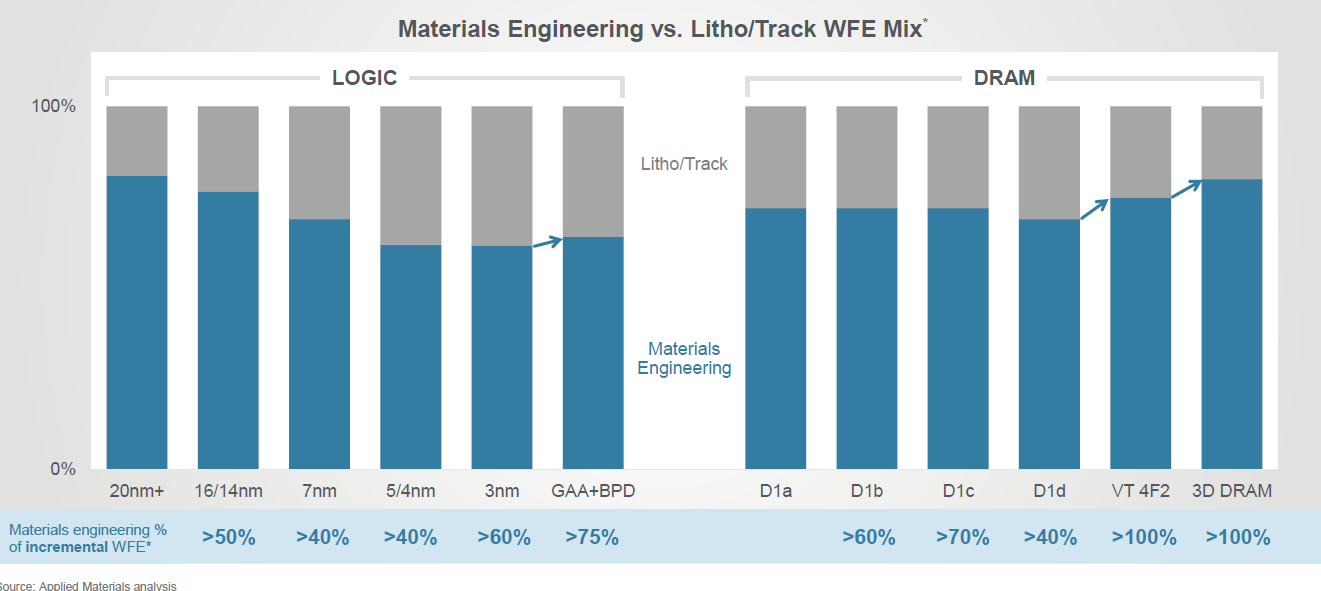

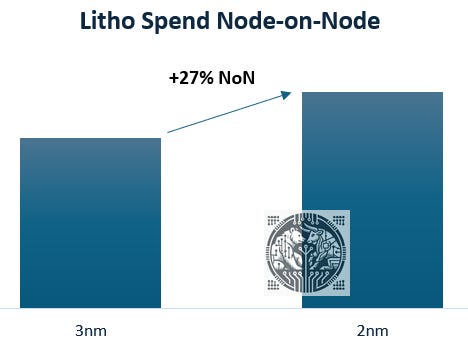

Another reason being mentioned for ASML’s weak orders is that the litho intensity drops at TSMC’s next 2nm node, chart taken from Applied Materials:

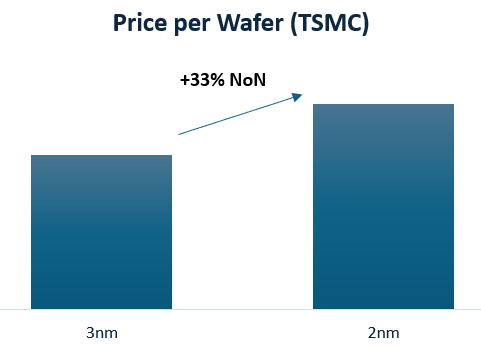

However, taking into account the roughly 33% rising cost to manufacture TSMC’s N2 vs N3 process technology..

.. even with the reduced litho intensity, the litho cost node-on-node will continue to rise at a rate of around 27%:

In this article, we’ll dive deep into the semicap space and explain the variety of problems that are currently hampering ASML. We’ll give insights from a number of industry insiders, such as a former technical manager at TSMC as well as from a former board member at ASML. We’ll also discuss the long term outlook for litho and the outlook for the semicap space in general, with a focus on Lam Research and ASM International, two players who are currently seeing larger tailwinds. Finally, we’ll do an analysis of the financials and valuation for all names in the semicap space.