ASML – The EUV Bottleneck

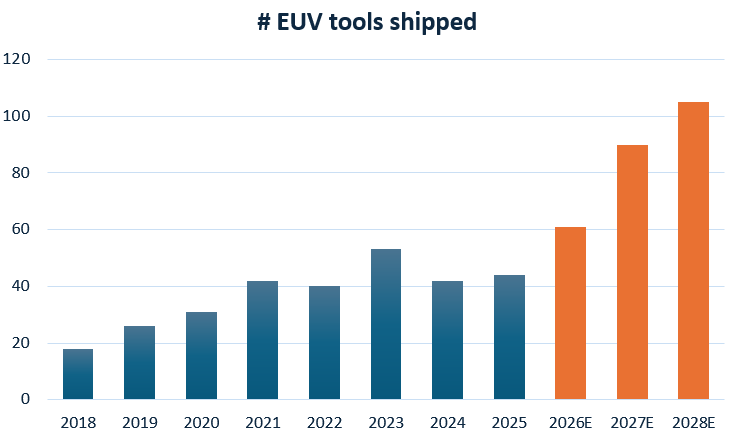

ASML’s tone has shifted from estimates where demand will be in the coming years to how much capacity they can provide (source: JP Morgan conference). Due to manufacturing optimizations, the company can probably ship 110 EUV tools in the coming years without building new clean rooms.

We can see that EUV shipments showed lackluster growth as from 2021. This was driven by two key factors—the industry digested the capacity which had been added during the covid semi boom while TSMC also moved to the 2nm node, which didn’t see an increase in litho intensity. Because TSMC didn’t dramatically increase the number of EUV exposures per wafer at 2nm compared to 3nm—as it moved from the FinFET architecture to gate-all-around (GAA)—the litho intensity on this new node flattened. Bears assumed that if new nodes won’t require steep increases in EUV anymore, ASML’s high growth era would be over.

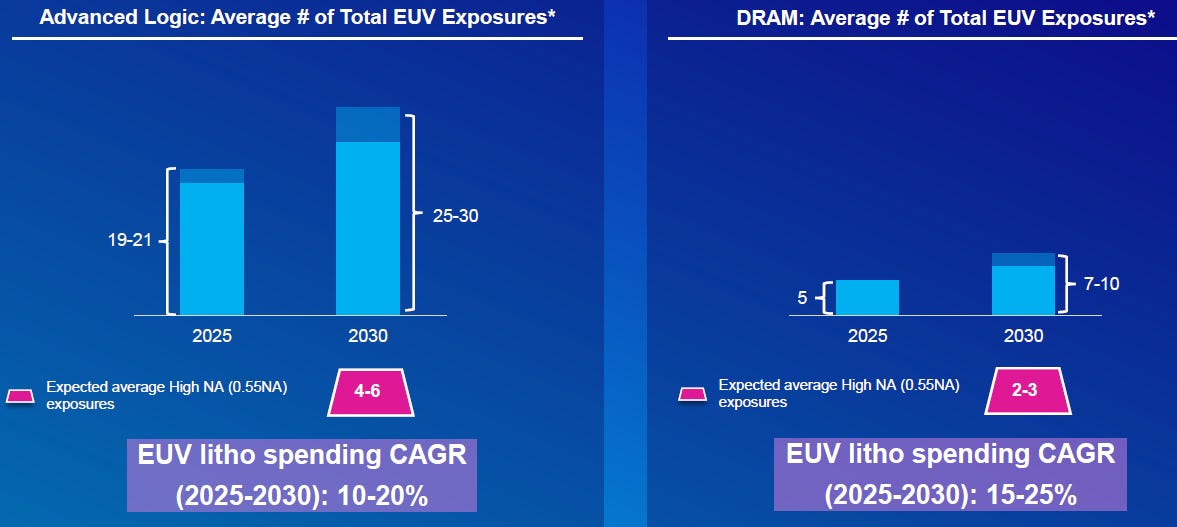

However, as transistor scaling resumes post 2nm as we move into the Angstrom era with the A14 and A10 nodes, EUV usage node-on-node will again see substantial increases. The same is true for new DRAM nodes, and ASML actually expects the steepest growth in litho exposures node-on-node in DRAM:

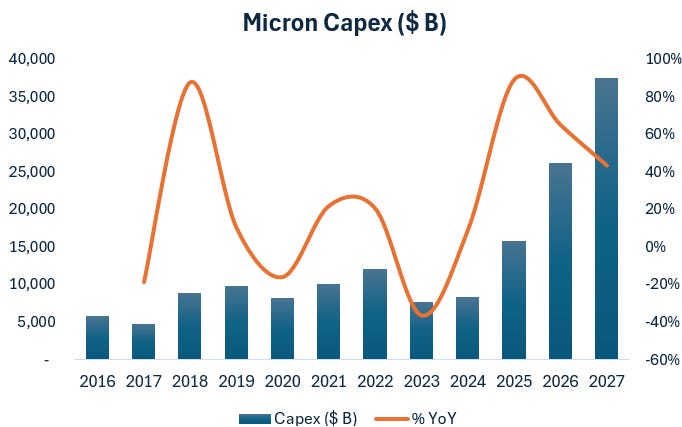

At the same time, AI is massively DRAM intensive (especially in HBM), which is driving an unprecedented wave of capex growth in the industry:

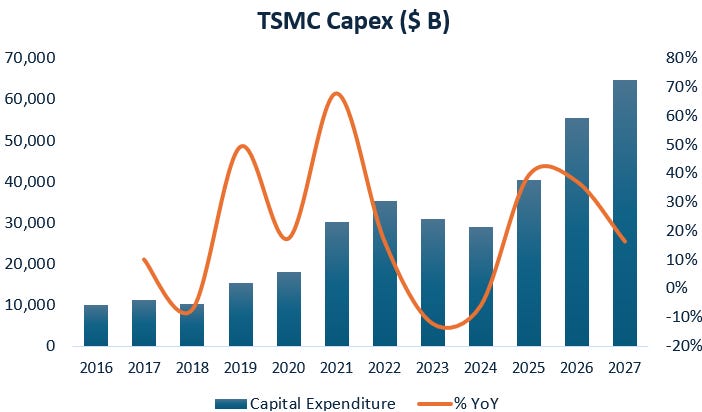

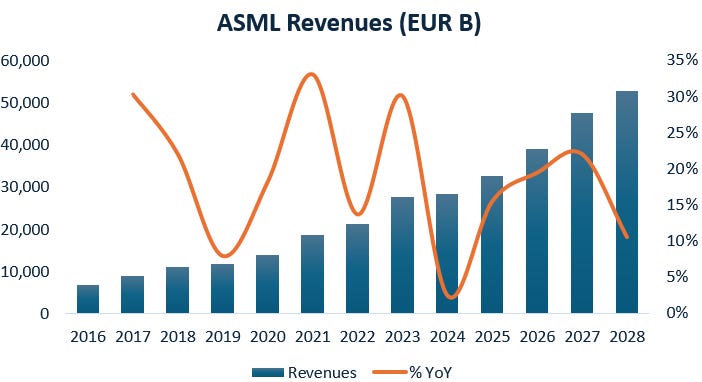

While also TSMC will grow capex by 37% this year. We continue to think that the sell side is underestimating TSMC capex growth in the coming years. First, TSMC capex growth rates are still below growth rates during previous upcycles like 2019 and 2021:

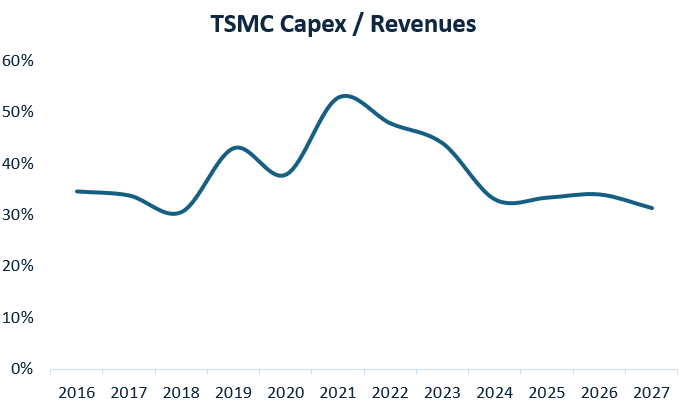

Secondly, also TSMC’s capex-to-revenues ratio remains at cyclical lows:

We think that TSMC has a lot of gas left in the tank and that the risk-reward is strongly to the upside here for semicap names such as ASML.

Overall, we see a scenario with steep capex growth at both the DRAM players and TSMC playing out, while we also know that litho intensity at their coming nodes will continue to go up. Meanwhile, analysts continue to model fairly tepid revenue growth for ASML in the coming years, with much lower growth rates than during previous semi upcycles:

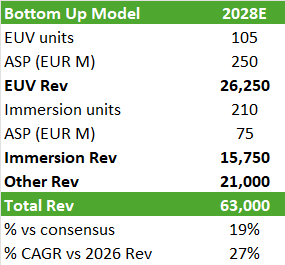

If we model in unit shipments from the JP Morgan conference, we already get to EUR 63 billion in revenues, 19% above consensus, giving a 27% revenue CAGR as from 2026:

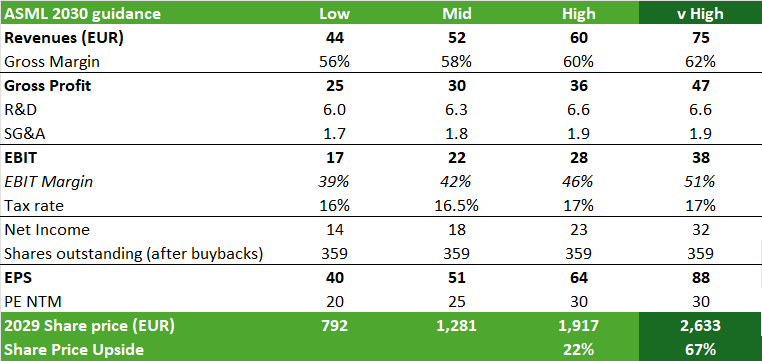

Below is the model we originally built based on ASML’s capital markets guidance, although we added a very high scenario due to the current demand boom in AI. As a result, ASML will likely move towards EUR 64 of EPS much sooner than 2030, possibly already in 2028:

Bottleneck investing has become popular and ASML is an obvious bottleneck in the AI value chain—it is the monopolist provider of both EUV and immersion lithography equipment. We continue to be ASML bulls and hold this name.

Next, we’ll go through further findings in leading edge semis from this week, a number of stocks we’re purchasing at these levels, including new names, and our current top conviction list in semis.