AI Economics & Outlook

After a weak start for tech stocks this year driven by a panic in software and subsequently the Iran war, markets went into one of the most spectacular rallies on record as hostilities in the Middle East came to a halt and one of the key frontier AI labs, Anthropic, disclosed stratospheric revenue growth.

There have been a variety of AI bear theses over the past few years. Initially, lower quality accounts argued that “Nvidia is just cooking the numbers”. Media reports speculated that “Nvidia’s revenues are simply driven by circular financing”. The most credible bear argument was probably that there wasn’t a killer app in AI, or no substantial revenue.

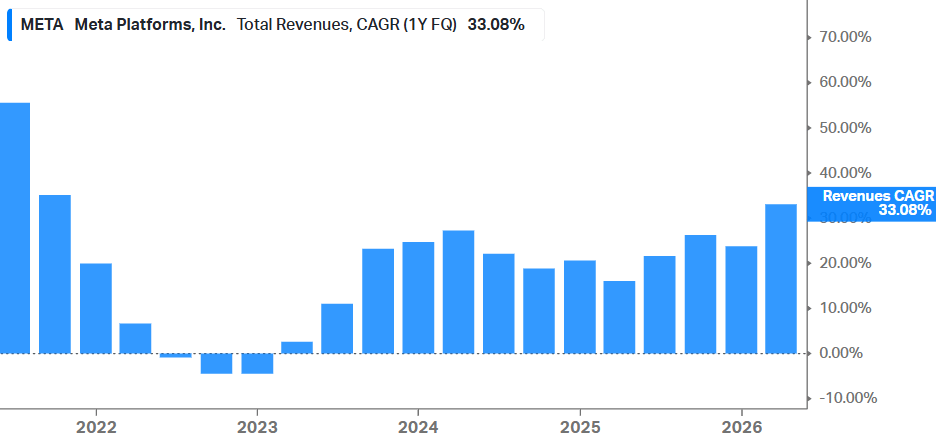

However, the first killer app was already there as AI was driving revenue acceleration at the largest companies in the world, i.e. the internet giants, by creating better user feeds combined with better ad targeting:

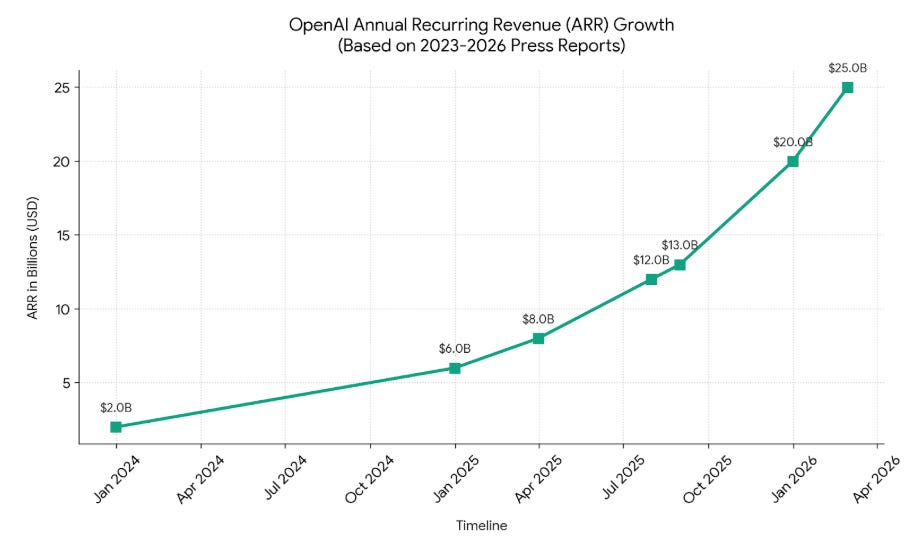

In the meantime, also LLM pioneer OpenAI managed to build up sizeable revenues driven by accelerating growth rates:

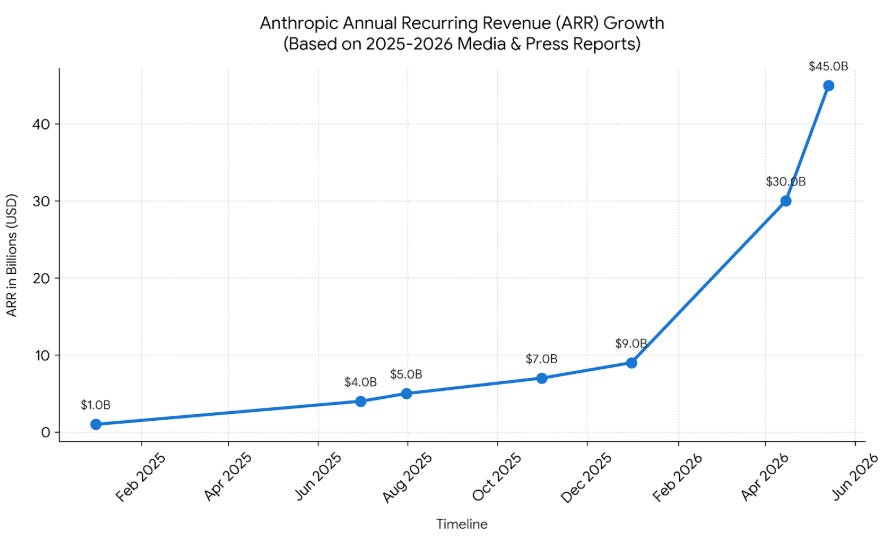

Then, in the first months of this year, it became clear that Anthropic’s revenues were fully exploding on the back of its Opus model’s coding capabilities.

Our personal experience is that our coding productivity has gone up 10x, easily, and so this allows a single developer now to do the work of what previously would have required a small engineering team of even 10 people.

Naturally, this will create massive cost efficiencies at all companies that write code. As such, Meta announced this month that it will be cutting 10% of its workforce alongside cancelling another 6,000 open roles. Similarly, Block—led by Jack Dorsey—reduced its workforce by 40%. Dorsey is also looking to cut out middle management layers and have engineering teams report to him directly via an intermediary AI layer.

Therefore, we think that the setup for certain names in software is looking attractive—we’re at historically low valuations in the space, many investors are now spending zero time anymore researching the space, while software companies that can successfully automate workloads for their customers are likely looking at their biggest revenue opportunity ever. Finally, there is a huge potential for software companies to optimize their workforce and cost base (such as share based compensation) to drive steep EPS growth. While low quality software will get disrupted, key systems that form the backbone of enterprises are well positioned here in our view to capture this opportunity.

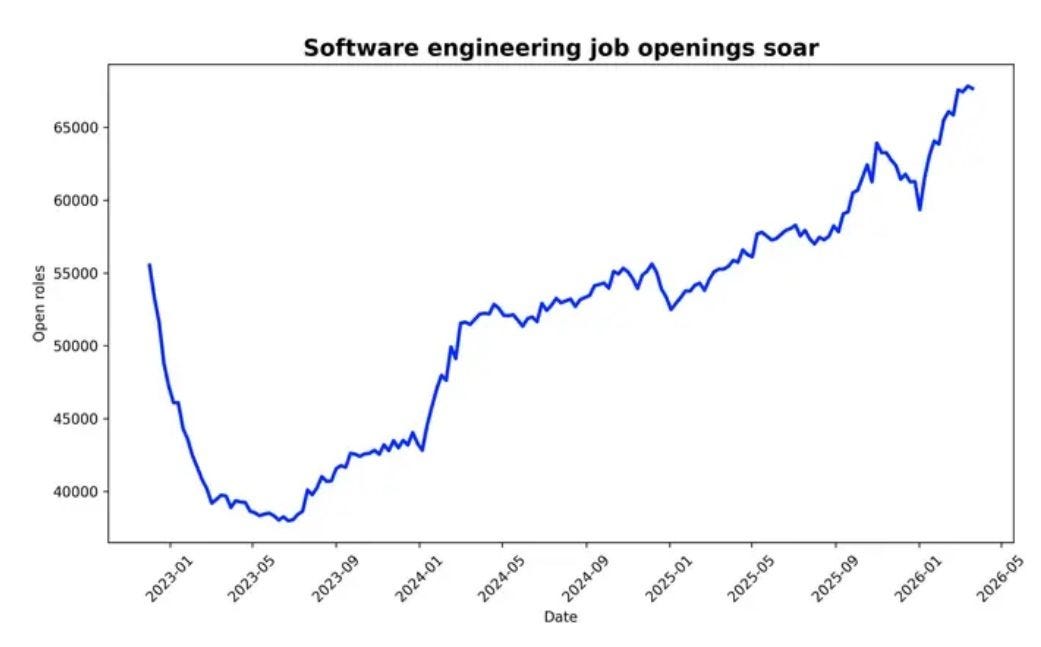

As the cost of writing production grade code has dropped massively, the demand for code is skyrocketing. Open roles for software engineers keep surging (chart below). Anything that couldn’t be automated before—either because the skills weren’t available or because the costs of writing the code didn’t justify it—now can quickly be written out by AI.

Overall, the current annual value that AI is creating is already in the hundreds of billions. We can see this by simply looking at Anthropic’s and OpenAI’s revenues, the revenue acceleration at the internet giants, the cost reductions in the required workforce, and then GPU revenues from running inference for open source models.

We’re in the very early phases of the AI revolution, similar to the nineties when it comes to the internet revolution. After the launch of the Netscape browser in 1994, we saw multiple waves of innovation in subsequent decades with massive new TAMs being created—search, social media, SaaS, the public cloud, streaming, etc. Killer apps such as TikTok even emerged only recently. It’s likely that with AI, in the coming decades we will see multiple waves of innovation that will continue to drive up demand. Writing code, creating better social media feeds and ad targeting, helping with research, tracking your calories, etc. are only the first applications of AI. There’s huge potential for large parts of white collar jobs to be automated or augmented with AI, as well as the emergence of physical AI in the form of robotaxis, humanoid robotics, and industrial automation.

When it comes to AI capacity currently being built, we see the risk of current capacity expansions being wasted as low as the environment will remain tight at least into 2027.

This is neocloud Nebius commenting on GPU demand on the recent call:

“Our pipeline generation in the first quarter grew 3.5x over the fourth quarter, and this is a record for us. And the demand is broadening across industries. […] The vast majority of capacity coming online over the next several quarters to 12 months is already under contract. We are typically seeing 4 or more customers competing for every GPU we bring online. We have significant expansion planned for 2027, including Vera Rubin’s, and we’ll start selling that capacity as we move into the second half of this year.”

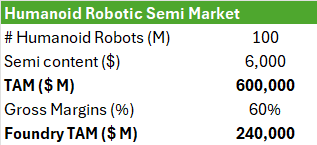

Physical AI is still too far out to really make an impact in the coming years, although this can become a large semis market in the 2030s. Say, ten years from now, 100 million humanoid robots are sold per annum (vs a smartphone market which is currently at 1.25 billion units), this would translate into another semi TAM of $600 billion. For comparison, Nvidia will be doing $372 billion in revenues this year.

Assuming the semi designers will make 60% gross margins, this means that foundries can capture a $240 billion market in physical AI. For comparison, TSMC will ‘only’ be doing $136 billion in revenues this year. And then there’s further potential in physical AI with robotaxis, industrial robotics, etc. We remain long term semi bulls and continue to hold the best quality names in the space.

Small Cap Semis Fever

However, we’re also seeing parts of the market that are starting to look frothy, especially in small cap semis that we would categorize as speculative stocks.

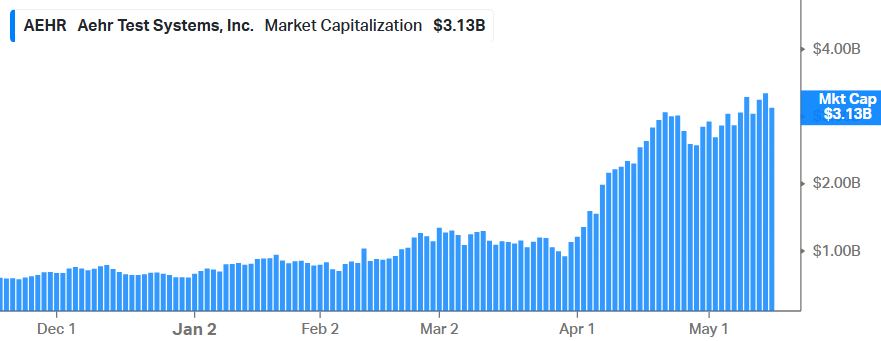

Take Aehr for example, a credible company with a strong growth outlook. However, with a market cap of $3 billion, the company is now trading on 60x its current backlog of $50 million. For comparison, ASML—which is probably more attractive in our view—is trading on 10 times its backlog.

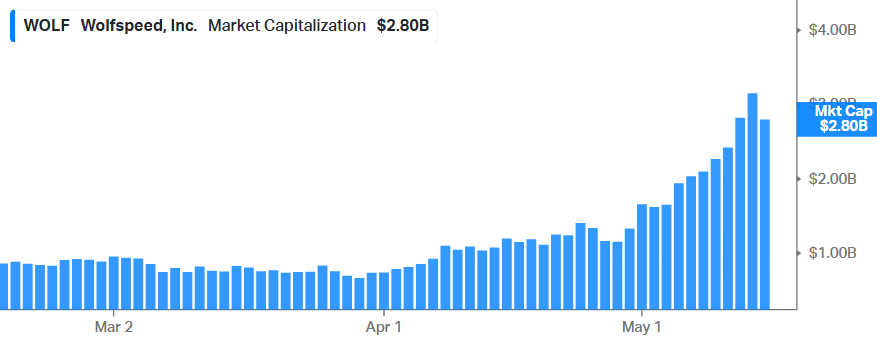

We see a similar story in Wolfspeed—an interesting company with a state-of-the-art SiC fab in New York. However, the market cap has gone up 4x since the start of April while we didn’t get any news of meaningful orders on the last call. Remember, due to low utilization rates, their SiC fab is still generating negative gross margins and is burning around $100 million in cash per quarter, while the company remains in a net debt position. Wolfspeed really needs orders to come in, in a SiC market that remains oversupplied.

We’ve seen a number of bullish reports connecting Wolfspeed to the solid state transformer (SST) market where SiC power semis will be heavily used. However, we’re unsure whether this market will be large enough to really turn this fab FCF positive. Infineon estimated the SST power semi market to be over $1 billion in 2030. If we bullishly assume Wolfspeed can capture 25% of this market, it would mean $250 million in revenues in 2030. Wolfspeed needs a lot more orders than that, and faster. In the meantime, power semi king Infineon is already shipping silicon for SSTs and continues to pile up orders, with SolarEdge announcing they will be sourcing their SST SiC from Infineon.

While it’s good news that Wolfspeed has developed a 300mm SiC wafer, likely at the request of TSMC for use in AI applications, SiC wafer manufacturing is a pretty commoditized market with tons of competition. If TSMC needs 300mm SiC wafers, they’ve likely asked a number of players to develop these. While it can give Wolfspeed a new revenue source, SiC wafer manufacturing is too much of a commoditized and low margin business for us to really get enthused here as well.

In our view, Wolfspeed’s share price is starting to get disconnected from the fundamentals as well and we see the risk-reward now as much more balanced compared to when we first initiated our position in December. Therefore, we’re locking in profits here and will allocate proceeds to stocks with better risk-reward.

Memory As The New Hottest Industry

In the meantime, we’re also starting to see classic signs of a bubble emerging in other areas of semis. Bloomberg notes that South-Koreans are now massively opening new trading accounts and borrowing money to invest in the local stock market, with the KOSPI index being heavily dominated by the two memory giants, Samsung Electronics and SK Hynix:

“In South Korea’s $4.6 trillion stock market, signs of euphoria are popping up everywhere. Enthralled by a 200% surge over the past year that has far outpaced every other market on earth, locals are borrowing record sums to amplify their bets on stocks. Trading volumes have soared to all-time highs, while daily price swings of 5% or more have become more common — making the benchmark Kospi index the most volatile major stock gauge worldwide.

The sense of FOMO spreading through offices, lunchrooms and family gatherings across South Korea has gotten so intense that investors are increasingly buying stocks for their kids, too: Data compiled by Toss Securities show a near 10-fold surge in new account openings for under-18s in the first quarter versus a year earlier.

“The mood in the retail community is very hot, nearly maniacal,” said Jang Eunjung, 37, a Seoul-based video producer whose YouTube show on stock investing grew from a tiny audience to more than 1.3 million subscribers as the market soared. “Will we ever see such a vertical rally again?””

Another classic sign of a bubble is the launch of new investment funds purely focused on the particular thematic, and yes, we’re also seeing that now when it comes to memory. From CNBC:

“‘Biggest bottleneck in the AI buildup’ fuels DRAM ETF to record. The Roundhill Memory ETF (DRAM) just hit $9.8 billion in assets under management in 43 days— the fastest pace ever for an exchange-traded fund.”

The DRAM ETF is purely focused on all memory stocks, i.e. the three DRAM/HBM players and the NAND players.

As readers will know, we’ve been holding the DRAM/HBM names over the past years as this is a fairly attractive three player market while AI is extremely HBM and DRAM intensive, giving a clear growth angle.

NAND on the other hand remains much less attractive as the industry is much more commoditized, and it’s also the least crucial type of memory for AI. Basically, this is where you store the KV cache when your DRAM can’t hold it anymore. HBM is what really powers AI workloads, and then DRAM is where you store data that you need fast access to. NAND on the other hand is much slower.

We’ll go in detail through our updated outlook for the DRAM/HBM space, with our thoughts on whether to continue holding these names or whether we’re locking in profits here.