Introduction, software eats the world

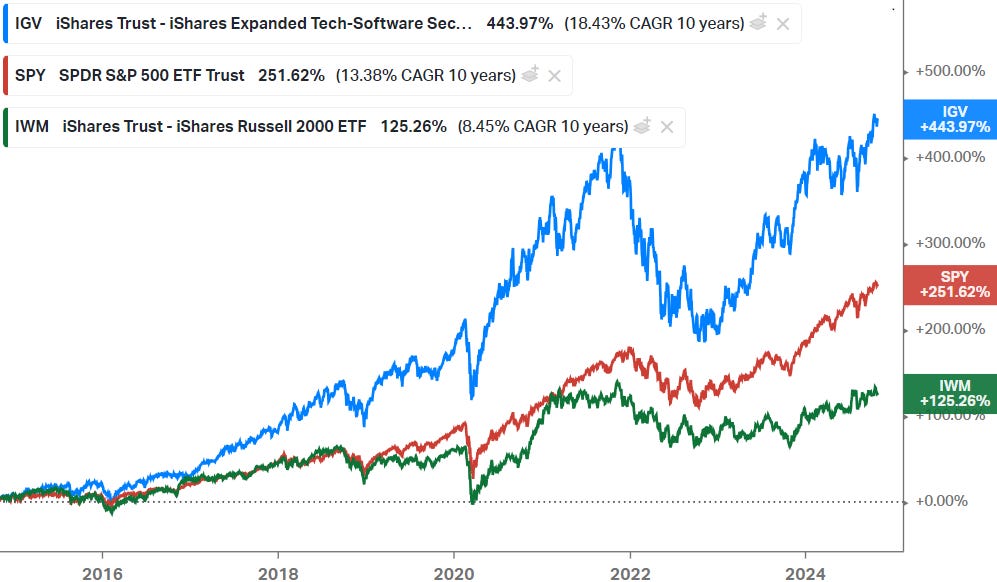

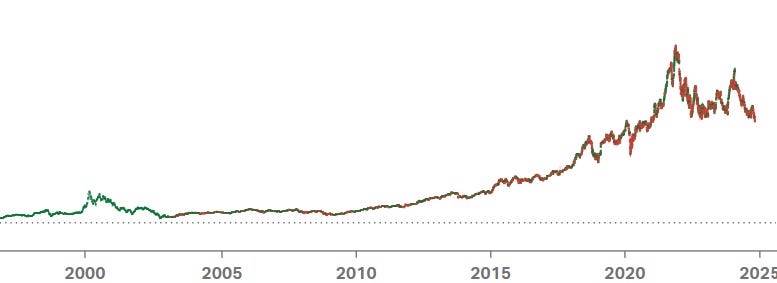

Software has been an excellent space for investing over the last decade, with the space strongly outperforming both the S&P 500 and Russell 2000 indices:

This isn’t a surprise. The software industry frequently exhibits high switching costs for users in combination with network effects, resulting in strong pricing power for the typically few number of providers that dominate a niche. As customers are running their operations on a particular software, the software firm can implement a ‘land and expand’ strategy at the customer by creating more modules on the software platform. Customers can then purchase these to get access to the additional software functionality and then run ever more workloads and operations over the platform. This is an obvious flywheel for revenue growth for software companies.

And even when a particular software architecture gets disrupted over time, such as the mainframe or client-server models, these companies continue to print cash as share losses are only gradual while these also can be offset with price increases to a certain extent, depending on the particular situation. On top of that, many of the software leaders of the client-server era have successfully transitioned to the cloud by also offering SaaS versions of their platform.

A negative is that these attractive characteristics of the industry have increasingly gained the appreciating of investors. Ten years ago, you could frequently pick up quality software businesses for around 15 to 30 times forward earnings or so, but now these valuation ranges have moved up for most of them. Good quality software is now usually trading well above 30x.

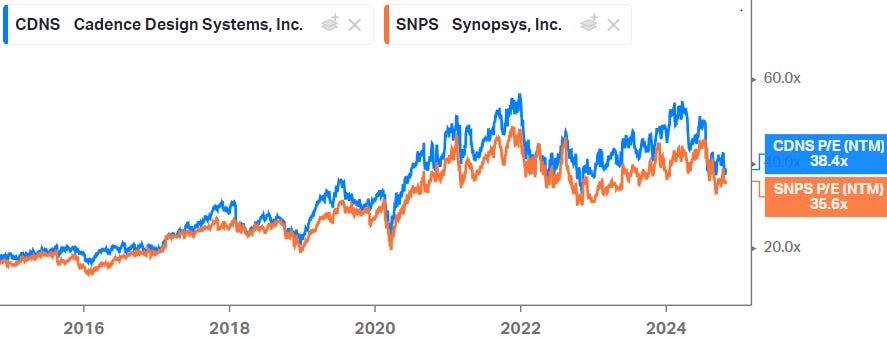

A few good examples here are Cadence and Synopsys, two software businesses that dominate the market for semiconductor design. While an acceleration in top line growth gives scope for further multiple appreciation, there is also a risk that if growth slows down we’ll see multiple compression over time.

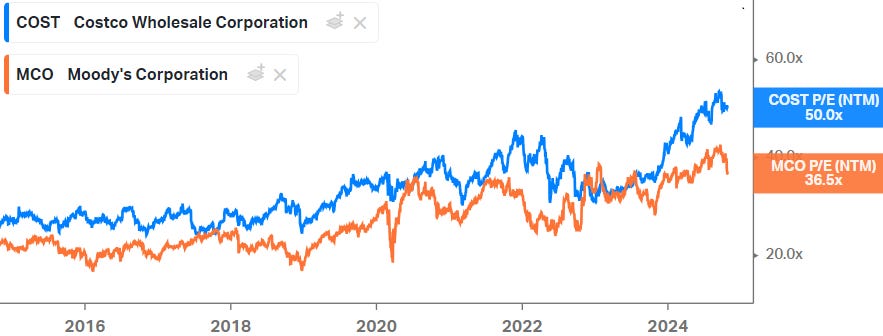

This is actually not a phenomenon unique to software. As the commodity supercycle collapsed around ten years ago, driven by the shale revolution in the energy markets and the slowdown of the Chinese economy more generally, investors woke up again that commodity markets are highly cyclical. Additionally, as the Sino-American geopolitical rivalry took off, and combined with the generally low interest rate environment, Western investors started looking for US-based quality assets that can bring in a safe and predictable growth rate. Two examples here are Costco and Moody’s:

Today we’ll be looking at a software name that is dominant in its space, where currently cyclical headwinds have been slowing down growth, but that has a number of interesting opportunities ahead of itself..

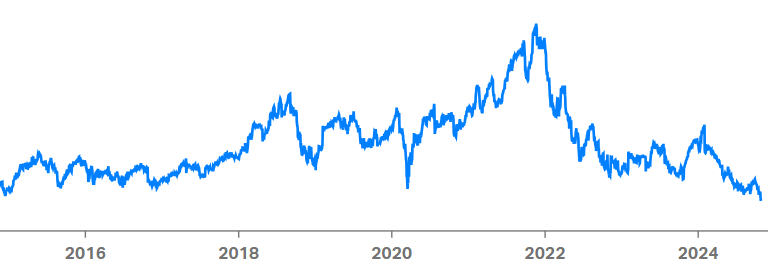

.. while its forward PE valuation is again near the bottom of its trading range:

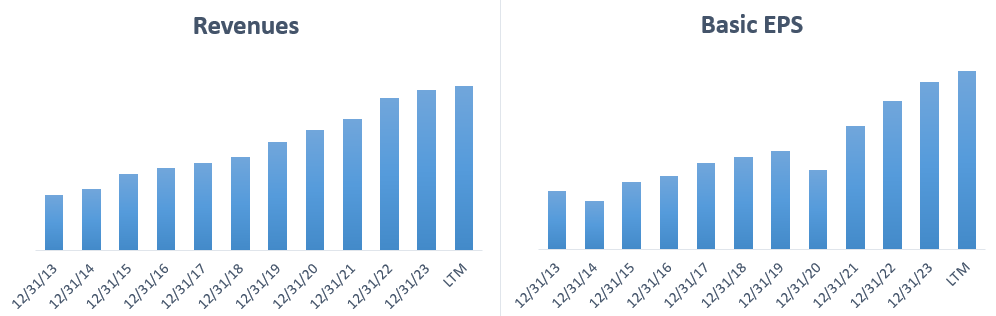

Which makes the cyclical slowdown in growth well reflected in the share price:

So the investment case is fairly simple — as the cycle picks up again, we should see an acceleration in top line and EPS growth, and combined with multiple re-rating. Additionally, as the company has been expanding successfully into new fields, there are substantial revenue opportunities from new verticals.